Generosity Wealth Management is excited to share that our founder, Michael (Mike) Brady, recently joined a distinguished panel at The Lenz Foundation’s live event, Overcoming Election Anxiety. This free virtual event focused on how to navigate anxiety surrounding the upcoming election season with greater peace, resilience, and mindfulness.

About the Event

Hosted by The Lenz Foundation, Overcoming Election Anxiety provided accessible strategies and insights from experts across various fields. Recognizing that elections can bring heightened stress, the panel emphasized practices for maintaining mental wellness in times of uncertainty. Topics included practical mindfulness techniques, the benefits of staying grounded, and the importance of compassionate engagement with current events.

Mike Brady’s Insight

With a background in wealth management and mindful financial planning, Mike Brady brought his unique perspective to the discussion, exploring the link between financial security and emotional well-being during turbulent times. In his segment, Mike emphasized how long-term financial planning can bring peace of mind, especially during stressful situations like election cycles. By focusing on enduring strategies and values, Mike underscored the role financial stability plays in personal resilience.

Empowering Clients Through Turbulent Times

At Generosity Wealth Management, we believe in the power of a well-prepared financial strategy to support emotional and mental wellness. Mike’s insights are a testament to our commitment to holistic wealth management—helping our clients not only build and sustain wealth but also navigate life’s unpredictable challenges with clarity and confidence.

Learn More

For more information on Overcoming Election Anxiety and other mindfulness events from The Lenz Foundation, visit their New and Recent Events page. We encourage our clients and community to explore resources that foster mindfulness as part of a balanced approach to financial well-being.

“Alcohol: the cause of, and the solution to, all of life’s problems.” – Homer Simpson

One thing we hear, especially during challenging times like these is, “I just don’t want to lose it all. I’m fearful of losing all of my portfolio.” In a diversified portfolio you are invested in hundreds to thousands of various things whether it be stocks or bonds. Whether you have a conservative portfolio or an aggressive, it should be diversified. So let’s unpack the fear of “losing it all.” What exactly does that mean and is it something that could actually happen? How does one then walk out of that fear and what action is needed to overcome?

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive, full service financial services firm headquartered right here in Boulder, Colorado.

You can see from the backdrop that I’m still self-isolated at Generosity Wealth North Boulder Headquarters which is also known as my home office. Hopefully all of you are doing well. I have some random thoughts today and the first one is something that I periodically hear from prospective clients over my last 30 years which is I want to be invested but I just don’t want to lose it all. I’m fearful of losing all of my portfolio. Let’s deconstruct that and talk about that as a fear or as a concern.

In a diversified portfolio, and you should have a diversified portfolio, you’re invested in hundreds if not thousands of various issues. Whether or not that’s stocks or bonds or whatever that particular portfolio is whether it’s conservative, moderate, aggressive. It’s invested in hundreds like I said, or thousands. In order for that portfolio, that pool of investments, to go down to zero all of them would have to go down to zero. All of the manufacturing companies, all the technology, all of the oil, all of the service. They’d have to go down to absolutely zero.

Can individual sectors go down at certain points? Absolutely. Can individual stocks go from something to bankruptcy? The answer is absolutely. That’s why you shouldn’t have a portfolio comprised of only an individual stock or just a few stocks or just some specific sectors. It just doesn’t make sense to be that undiversified. Having a diversified portfolio does not guarantee against having market ups and downs, and right now we’re seeing some of those market downs. It does not protect you fully from that, but in order for it to go down to zero all of the underlying investments that comprise that portfolio which would be hundreds and thousands and the most common names and common stocks and companies out there would all have to go bankrupt and down to zero. Hopefully you can see this is not very probable. If that was to happen we truly would have an Armageddon here in the United States.

The economy and the market are not necessarily the same thing. In March of 2009, March 9 to be exact, was the absolute low for the stock market. At that point if I was to say to you over the next eight years we’re going to have two presidential terms, two four-year terms, for the very first time where an economy that’s going to have a sluggish recovery and never be greater in any of those eight years a GDP growth of over three percent. It never happened before. Two-four year terms for a presidency where the GDP didn’t grow more than three percent. And it’s not Obama’s fault. This is not about Obama. I’m just using that as a benchmark that the economy is going to be sluggish and it’s never going to be over three percent and oh, by the way, the best thing that you can do is invest in the stock market. You’d say that’s crazy. The economy is – really, you’re telling me the economy was sluggish and the stock market is going to be great? The answer is that’s exactly what happened. It was almost a tripling from March 2009, almost a 300 percent increase during the next eight years. The stock market, the buy market, those unmanaged stock market indexes, the S&P, the Dow Jones, et cetera, they’re what we call forward thinking. What investors believe is going to happen in the future. And sometimes they get it right and sometimes they get it wrong.

In 2008-2009 I would say that it was oversold because you can see that what they thought was going to happen, that the economy was going to be even worse. And then they realized wow, we overshot this thing. We overshot and then it was a buying opportunity.

If I was to ask the person on the street, if I was to ask you who the best investor of all time is most people would say Warren Buffett. I mean Warren Buffett of course. If you have some longevity in the markets you might remember Peter Lynch who retired about 25 years ago. You might say Peter Lynch. He worked at a big mutual fund company. Both of them believe that, and this is a direct quite from Warren Buffett, “Be greedy when others are fearful, fearful when others are greedy.” So, I wonder what did they know? What do I know that they don’t know if I do the opposite of what they say.

They’re very smart investors. They believe, and I do as well, that you make decisions with your head and not with your stomach because the stomach when you do that in the midst of difficult decisions you make bad decisions. That’s why you have a multiyear plan that you stick with that I’ve talked about in some of my previous videos.

It’s just very important that the economy is not necessarily completely indicative of what the stock market’s going to do and that we make decisions with our head and not with our stomach because that leads us down the wrong path.

If we knew, if we had perfect foresight we would know what to do, but none of us have perfect foresight. I have had it in my mind I’ve thought about that there’s two different types of people in the world and this applies to so many different areas. When I talk with people about unintended consequences and potential consequences there’s one type of person who says hey, I’m not going to actually do anything until I know it’s going to have a positive outcome. I want to know not 100 percent but I want to have a pretty high probability that the action I’m going to take is going to have the positive outcome that I want.

There’s a second type of person who says I’ve got to do something. If it has an unintended consequence and it might even be negative, well at least I’m moving forward. At least I’m taking action. And not taking action, particularly when we don’t know the consequences of that action is sometimes the most difficult thing to do is to not do something just so that we can feel that we’re doing something.

If there is an action that someone wants to take it’s a systematic rebalancing. The problem with that meaning that maybe your stocks or equities have gone down, it’s increasing the equity exposure. Doing the exact opposite of what your emotions might actually be telling you at this particular time.

So, if there’s some action to do it’s actually to reevaluate. Maybe my stock and equity portion has gone down. Maybe it’s time to rebalance to buy more of that. That is a question that should be asked that you can think of.

I’ve said for many years as part of my random thoughts here I’m just going to go that some of the most difficult times to talk with an investor to make investment decisions is when you’ve made lots of money and you’ve lost lots of money. It has everything to do with your mindset and the behavior that you’re bringing to the decision. If you’ve made lots of money you might have just been lucky, but you have overconfidence in yourself, in your decisions. If you’ve lost lots of money it’s the opposite. There’s a fear that’s always the way it works and it just doesn’t work that way.

Most years have a 10 percent decline. I’ve thrown up on the screen not now but in previous videos that you’ll see that’s the normal. There is a correction of 10 percent I most years. There is a 20 percent bear market about one out of every four years. There is a large correction of 30 percent and 40 percent, let’s just kind of look back. In 1973-74, in 2000-2001-2002, in 2008-2009, that time and then right now. When we look at all that we’re talking about once a decade. The 70s, the early 2000s, the late 2000s and now. About once every decade and in every single time it has recovered. Maybe not exactly when we wanted it to. Of course we want it to go away next week, next quarter, next year. And it might. I doubt it’s going to happen tomorrow, but it has always come back and it’s about once every 10-15 years.

You’ll notice that I didn’t say 1987 because 1987 was actually a positive year for the unmanaged stock market indexes. Everyone thinks that it was this, it’s because it happened very quickly. It just wiped away a years’ worth of gain, but actually ended the year positive. And then the years after that the next couple of years were positive as well.

So, it’s good to keep everything in perspective. That’s why I’m always talking about a long term vision. I said something in my last video about Point A to Point B an the reason why I bring that up is Point B is not retirement. It’s not outliving your money. or not outliving your money, you and your significant other’s money. You might just happen to have a retirement event inside there. If you’re 60 years old, I’m just arbitrarily picking 60 years old, your point is not 65 years old. It’s for the rest of your life because you don’t want to outlive your money. But during that timeframe you just might have some life events that happen – your retirement, perhaps the loss of your spouse or significant other. There’s lots of major things that happen during your life expectancy or when you add in your spouse or significant other, both of your lives.

It really does boil down to having longer time horizons even when we’re close or already in retirement. That’s why it’s good to say we had multiyear strategies, it’s good to keep that in mind. That’s why you do all the work before something like what we’ve seen in this past month which has been very bad, not good at all. You do it before that happens. Steel yourself for those decisions and five and ten years from now you’ll say it absolutely was horrible while I lived through it. I sure am glad it’s over. It was a painful lesson. I hate that. You know what? The best thing that I did was I did nothing at that point.

Call me at any time, 303-747-6455. You have a wonderful day. Bye bye.

“Bear Markets are periods when stocks are transferred from weak to strong hands, as does wealth when recoveries occur.” – Buckingham Strategic Partners

I promised in my last video (March 12th) to have a longer discussion about the current economic and financial situation. You’ve got it right here! And with graphs!

Hi clients and friends. Mike Brady here with Generosity Wealth Management, a comprehensive full service financial services firm headquartered right here in Boulder, Colorado. As you can see from the backdrop I am back in my office here in Boulder. The last two videos I did from Orlando. I’m going to make today’s video a little bit longer. When I’m traveling it doesn’t matter with today’s technology except when you want to do a newsletter with big video files and transfer, et cetera, and that gets a little irritating I assure you.

Lots going on in the world and in the markets and I want to talk about some of the implications. Let’s first put up on the screen a graph. On the left hand side that is the unmanaged stock market index, the Dow Jones Industrial average. The left access is percentage rate of return. And what you’ll see is for the first one-and-a-half months of this year it was positive, and then it took a huge sharp downward over the last three weeks or so. It is rebounded slightly because of the nice Friday that we had. However, it is definitely near the bear territory. It dipped into it which means a negative 20 percent decline. So it dipped below and then it’s kind of popped back up, but it is right there at that cusp of what we technically call the bear. Not good at all.

One thing that is important, we always talk about from a military engagement point of view that everyone’s always fighting the last war. Every general is fighting the last war or it seems since the Vietnam War everything is always compared to Vietnam. Well, we now seem to compare everything to the 1987 decline and the 2008 decline. I’m going to talk here in a few minutes about why it’s not 2008.

Before we move on though I want to talk a little bit about bonds. Bonds have done well. I’m going to put another chart up on the screen. What you will see is they have done what they’re supposed to do which is go up when stocks go down. The correlation meaning it’s very highly correlated if they do the same thing as the stock market. It is negatively correlated if it does the opposite. And what you’ll see is a portfolio of stocks and bonds. The stocks have gone down but the bonds have gone up. And whether or not a particular portfolio has gone up or down is how much of the mix you have. I’ve said in previous videos that over the long term it’s my belief that you’ll be happier over ten years the more aggressive that you are, but that doesn’t mean on a short-term basis whether that’s months. In this case it’s been weeks, even days frankly, but on a year-by-year basis you’ll be unhappy because the volatility increases.

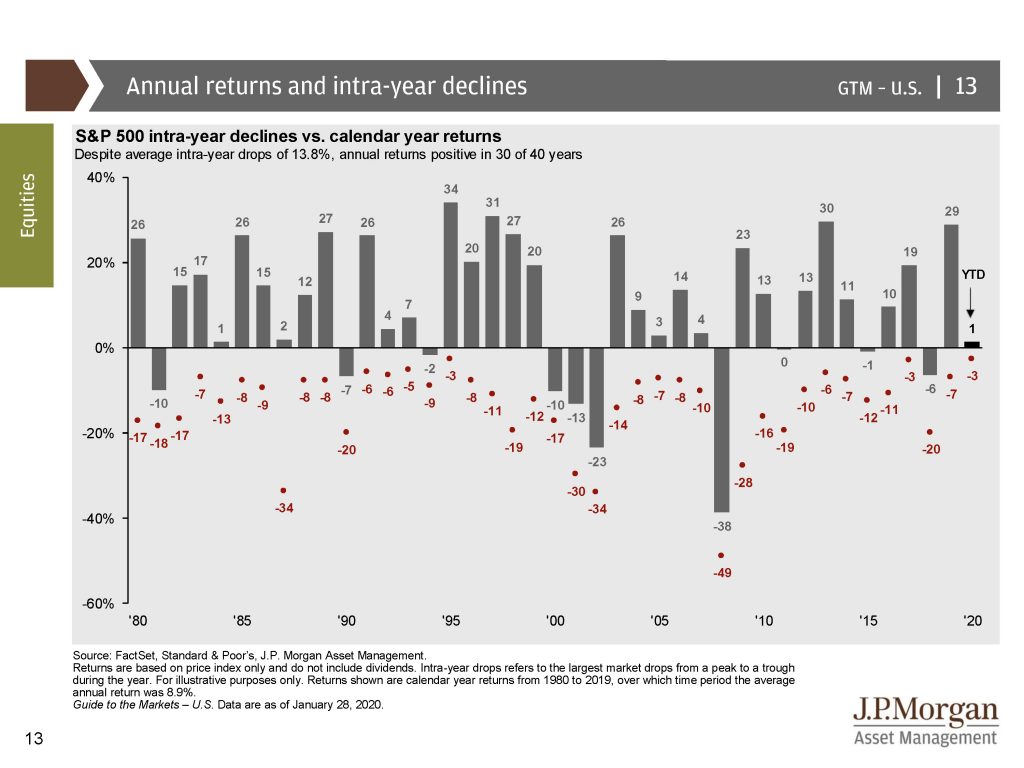

I’m going to put one more chart up there. The third chart is over the last 20-30 years.It is since 1980 and what you’ll see is the bottom numbers or the red numbers, those are the intra-year declines, the declines that happen within the year. And then you’ll see that the gray number,I’m not sure how it’s going to show up on the screen, is what it is the year and the data. And, of course we’re just starting off the year not even three months in. One thing that’s important to note is 1987 which people talk about all the time that actually was a positive year. Most people think that it was some huge negative year for the stock market when it actually had made lots of money through the first two-and-a-half quarters and then it gave it all up in a spectacular fashion over a day or two. But it actually ended the year positive.

So far this year we’ve had a very dramatic three weeks. That does not, of course, mean that the entire year is for naught. This is a little bit different than 2008 for the simple fact that we started the year in a very high economic and positive nature. Unemployment – I’m going to put a graph up on the screen and what you will see is that unemployment was at an all time low and we had incredible labor force participation with wages rising in the last year or so. Just absolutely wonderful.

This is not a financial crisis. This is a healthcare crisis. Healthcare crises we’ve had before. This is a particularly bad one. We have survived the SARS. We’ve survived some of the other, the Ebola scare and other things in the last 10 to 20 years. But we haven’t seen anything like this and particularly the concern and the scare. I’m not an expert on how this crisis will play out as it relates from a healthcare point of view. There’s enough experts on Facebook that you can watch who are all your friends who used to be experts in something else. Now they’re experts in this. I admit that I don’t know and I know that there are many scientists who admit that they don’t know as well. They have models which are projections which might have some degree of probability, but this is a healthcare crisis, not a financial crisis.

Our banks were not in a strong position back in 2007 and 2008. Now they are in a very good position on strong holding. I’m going to put a chart up on the screen.What you’re going to see is interest rates. The Fed and interest rates are very high. Sorry, are very low. And the projected, that one higher number was what they projected that they would raise interest rates. Now it has been adjusted so that we will have some interest rate declines which is a good thing. That pumps money into the economy. This is a good thing. It will help governments, consumers and corporations refinance debt with lower debt burdens with those sectors of the economy.

I’m going to put up on the screen another chart which is oil prices. You’re going to see a collapsing of oil prices which is effectively a big tax cut for consumers and companies that are heavy energy users like airlines and things of that nature. This is bad for oil producers. There’s going to be winners and losers in pretty much anything that happens in the economy, but this is a “huge tax cut” if you want to say. I’m doing air quotes if you’re watching the video for the consumer. And so this is a good thing unlike what the price was back in 2008 which was significantly higher than what it is today.

The U.S. has the highest – I’m going to throw another chart up on the screen. We are less dependent than many other countries on our imports and exports. I’m going to put up on the screen a list of all the companies, their imports and their exports as a percentage of their GPD. So that means that as a percentage of what they produce when you add up all the goods and services within a country what percentage of imports and exports as a percentage of what they produce both like I said goods and services. You’re going to see that when we flip through that first screen and a second screen you’re going to see I’ve just highlighted what the world average is. The U.S. is near the very bottom. That is because we are actually a pretty well contained goods and services producer and user. There are many countries that are in a world of hurt if the global imports and exports and trade dramatically change. We’re at the very, very bottom and in comparison to the rest of the world that is a good thing. It is not however, good for us because we are, I mean completely good for us. Everything is relative. When the global economy slows down we slow down as well.

And I am just as worried about our local businesses. We’ve talked about the health of our citizens, our fellow man, our fellow woman, our fellow person and we should be concerned about that. Don’t get me wrong. But just as concerning to me are those people who are from an economic point of view more vulnerable than others. Not all of us can work at home. I mean I’m very fortunate that I get to. I’m in a white collar job. There’s an awful lot of blue collar people out there. Your servers, people who are in the service industry or in manufacturing that you can’t work from home. We should be worried about them as well. And so from a good point of view today versus where we were back in 2008, the consumer debt is much, much lower.

I’ve got the screen here and I’m going to put it up on the screen. The consumer debt is significantly lower. I’m going to put it up there on the screen and what you’re going to see is consumer debt is significantly lower than where it was. Household debt service is at 9.7 and not at 13.2 where it was back in 2007 and 2008. This is a good thing that we have much less debt from a consumer point of view than where we were back in 2008.

I was having a conversation with someone at my particular gym, my dojo, and they were talking about hey, wait a second. I’m in my 60s, I’m in my 70s. Will I have enough time, we talk about the longevity in the markets and the answer is I would hope so. I’m going to put up on the screen and particularly on the left side is the probability of reaching ages 80 and 90. If you are 65 years old you still have, particularly if you’re a couple, you have a 90 percent probability that one of you will reach age 80. You have a 50 percent probability that you will reach age 90. Yes, five and ten year time horizons even if you’re 75 and 80, particularly if you’re a couple. Now let’s say that you’re single. I would hope that you’re not going to die next year or the year after. Longevity is still something that you have to keep in mind. And so just throwing it into a mattress, throwing it into a money market or a savings account will almost guarantee you that you won’t reach some of your goals if you need income from it. And so we need to watch out for the longevity. We don’t know. Every person is individual in their particular portfolio and that’s why when I throw a word guarantee it’s if you have a certain rate of return that you have to achieve then there’s a balance between having the safety that you desire by not participating in something and then, of course, along that spectrum of where can I stay with my particular plan and reach those percentage rates of return that I’m hoping from the long term. And we’ve got to be in this for the long term.

There’s a quote that I read in an article and I want to make sure that I get it right. “Bear markets are periods when stocks are transferred from weak to strong hands as does wealth when recoveries occur. We’ve recovered from every past crisis which we tend to experience with great frequency about every two or three years there’s something that causes some dis-ease and right now there is some and a lot, but we too will recover from this.”

Mike Brady. Generosity Wealth Management, 303-747-6455. Give me a call at any time. Thank you. Bye bye.

“Stop a minute, right where you are. Relax your shoulders, shake your head and spine like a dog shaking off cold water. Tell that imperious voice in your head to be still.” – Barbara Kingsolver

Turbulence in a plane is normal, and so it is in the markets. This is the biggest turbulence we’ve seen thus far, and in 11 or 12 years. Painful! But that doesn’t mean you change a long-term decision on short-term emotions. In my opinion, the ones fives years from now who are the winners are the ones who are in control today. That was true in the past, and I believe in the future. I’ll continue with videos and newsletters as every day seems to be important. Due to regulatory requirements it takes a while from recording it to out to you, but I’ll do my best! Watch our video to hear more!

Hi clients and friends. Mike Brady with Generosity Wealth Management; a comprehensive full service financial services firm headquartered in Boulder Colorado. As you can see from the backdrop I am still at my hotel room leaving in about 45 minutes for the airport. I spoke at a financial conference actually a couple of days ago and with today’s technology it doesn’t really matter. I have the office here as if I was right there in my Boulder office with today’s, like I said, technology and Internet and everything else.

So, so much is going on. Every day is exciting. I’m assuming that you are paying attention to the news and watching everything and anyone who tells you how it’s going to play out in any aspect of the world at any time, not just today but in any time of the world is just lying and I’m not sure why they think that forecasting the future is helpful or even possible.

Reaching your financial goals and the best way to reach those goals is clearly defining your goals and having a plan for how to get from point A to point B. I think of it as riding in an airplane, from point A to point B there might be some turbulence, nobody likes it. The better the airplanes that we get the less turbulent things become, they’re able to buffer them so that you don’t see and feel what’s happening. But sometimes there is turbulence in the airplane, which is, of course, where I’m going with turbulence in the market. But in the plane it happens, it’s absolutely horrible but you know that periodically it does happen. Hopefully it doesn’t preclude you from taking that next plane ride because your life is much richer when you’re able to travel from point A to point B.

The market is no different, investments no different. Sometimes there’s turbulence. This happens to be a particularly difficult air pocket. I cannot believe the oversold indicators that I’m seeing. It’s quite remarkable. There are certain times in our lives where we’ll look back on it and say remember that time? And in most recent it was, of course, 2008. Another really bad selloff that was very precipitous was when the S&P downgraded the U.S. government in 2011. Maybe you remember that. Both of these incidents were recovered. They were painful both of them. We might remember them.

If you’ve been watching my videos I’ve been talking about the unnatural nature, the unusual nature of our calmness over the last two/three/four years that we’ve become lulled into expecting that that’s always the way it is there’s no volatility, very little volatility in the markets so I highly recommend you do that. I did a great one last summer August or September talking about the number of positive plus or minus one percent days in the year was remarkably low but most people perceived it as being particularly high but that actually wasn’t true. And it’s one of the ways that I would argue news media can really provide a picture that’s not statistically true or maybe completely accurate without emotion. These things do happen, like that turbulence on the plane the turbulence in the markets do happen, they are absolutely uncomfortable when they happen but that’s why it’s good to take a step back and say okay let’s be calm and remember that this is part of the plan, that I knew it was going to happen and then it did happen. I mean it’s just completely unpleasant but a part of that journey from point A to point B.

I mentioned something earlier about being oversold, yeah I watch a lot of technical indicators. At the end of the day my training almost 30 years ago was in technical trading. That’s when you’re doing various charts and things of that nature and the oversold nature of this is mind boggling to me. I’m very much looking forward to when it would turn around and that can be later today, tomorrow, next month, next year, I don’t know. But that’s the reason why oversold from my point of view leads to a very good market and that’s why we then have long-term investments along the way so that we can benefit from that when it happens at some point in the future when I don’t know when it is. I mean that’s why you have to kind of deal with things now and the best thing you can do is have control of your emotions.

Anyway, I’m going to continue to have these videos periodically when I’m back in my office I have a little bit more charts and things of that nature so I might get a little bit more technical for those of you who might want more technical. Anyway, 303–747–6455. Mike Brady. Thanks. Bye bye.

“By staying calm, you increase your resistance against any kind of storms.” – Mehmet Murat Ildan

Every single year there is some kind of market volatility. It is normal for there to be ups and downs. Therefore, preparing ourselves for it early on is the key. We know it’s going to happen, so we will have a multiple year strategy in mind at all times. And if there are any concerns, of course, you’ll call your favorite financial advisor Mike Brady!

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered right here in Boulder, Colorado.

Last month I did the year end review and it was a little bit longer so this time I thought I would talk shortly about a topic that I know is going to happen in 2020 which is volatility. I’m big into setting up expectations. I’m big into controlling our emotions and having a plan. The reason why I bring that up is in 2020 like every single year there is some kind of volatility. It is normal for there to be drops in the market. There are ups, there are downs.

I’m going to put a chart up on the screen which shows the market going back decades, and you’ll see on the bottom below the axis there are red numbers. Those are the intra-year declines and it is normal for there to be intra-year, within the year, declines in the stock market, the unmanaged stock market indexes, of double digits or more, 10 percent or more.

I’m recording this at the very end of January and, of course, you’ll get it the first part of February and nothing has happened so far this year. However, we have 11 more months. We have an election. We have many different things. We have a global economy that’s very complex. But one thing that I can almost guarantee is that the market will go up and down at various times. And our reaction to it is going to be much more impactful to reaching our financial goals than that actual event of the ups and the downs. That’s my opinion at least.

Therefore, setting ourselves up now and saying okay, great. I know it’s going to happen. I’m going to be cool. I’m going to have my multiple year strategy in my mind at all times. And if I ever have any concerns, of course, I’ll call my favorite financial advisor Mike Brady.

That’s what I want to talk about this year so when it happens don’t be surprised. With the market as high as it is right now, hundreds of points on the unmanaged stock market index, the Dow Jones Industrial Average doesn’t mean as much as it used to frankly, 5, 10 and 20, 30 years ago. We look at the percentages, we know it’s going to happen but we keep the long term vision in mind. What I believe is one of the key ingredients to long term success is keeping our emotions in check, keeping the big picture in mind and really looking at how are we going to reach our financial goals not only with our investments but with all the financial decisions that are going on in our lives.

Mike Brady, Generosity Wealth Management, 303-747-6455. Thanks. Bye bye. Have a wonderful week, a wonderful month. We’ll talk to you in a month. Bye bye.