The halfway point of the year is a natural time to reflect—not just on investment performance, but on whether your financial plan is helping you build the life you truly want.

In this month’s video, Michael Brady shares why successful financial planning extends far beyond market returns. While the first half of 2026 has reminded investors that markets rarely move in a straight line, the bigger lesson is one that doesn’t change with economic headlines: your investments are simply the tools. Your purpose, your family, your legacy, and your goals are what truly matter.

Watch this month’s Mid-Year Update as Michael discusses staying focused through market volatility, the value of diversification, and why aligning your wealth with your purpose remains the foundation of every financial plan.

Transcript

Hi there, Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered here in Boulder, Colorado.

Today is our halftime report. Half the year is gone, and we have half to go.

I want to talk a little technically about the markets, but I’m going to be very philosophical today as well.

Before I go on, you’re probably wondering what’s up with my backdrop. I’m in a hotel room because my very favorite uncle is not doing well. He had a heart transplant about eight years ago, and now, in his 70s, he’s facing some health challenges.

I’m very fortunate that I can continue working with clients and serving in my chosen profession anywhere I have my iPad, internet access, and video capability. So this hotel room is where I’m recording today, and honestly, it’s the best backdrop I could find. I still wanted to get this newsletter out to you.

It kind of reminds me—and this is where I get philosophical—that during the first 20 years of my 35-year career, I wore a suit and went to an office every day. At one point, I made a proactive choice. I wanted to make an impact in the world. I wanted to live my life. I wanted the flexibility to support my family when they’re sick or when they need me. That’s very important to me.

You may feel the same way. You want to support your children, your grandchildren, and your loved ones. Maybe your purpose is to travel. Maybe it’s making sure your needs are met in retirement so you don’t outlive your money. Maybe it’s maintaining the dignity and freedom to make your own decisions or passing your wealth on to the next generation or to charities.

Whatever it is, you have your own goals.

Very few people wake up in the morning and say, “I want to think about my investments today,” or, “I can’t wait to review my financial plan.”

Those things are simply the means to an end.

They’re the processes that help us accomplish what really matters.

Here at Generosity Wealth Management, we say that we align wealth with purpose and possibility. It’s important to understand what your purpose is and what possibilities you’re striving toward—even those you may not have thought about yet.

Think about a watch. Most of us care about the hour hand, the minute hand, and the second hand. Do you really care about all the gears underneath that make it work? Or, in today’s world, all the electronics inside a digital watch?

No.

You simply care that it tells the right time and gets you where you want to go.

That’s exactly what we do here.

We’re trying to align the pieces of your financial life with the realities of the world so you can get where you want to go. It doesn’t matter if someone else gets there first or later. What matters is your goals, your purpose, and your journey.

Generosity Wealth Management exists to help you get there.

Generosity Estate Planning focuses on maintaining dignity while you’re living and ensuring your wishes are carried out after you’re gone. That practice is led by Cassidy Murphy, a seasoned attorney with more than 25 years of legal experience.

We also serve business owners through Generosity Business Exit Planning, a division we don’t talk about as often. There, we help business owners prepare their companies for transition—whether that’s passing the business to the next generation, selling it, or simply making sure both the business and the owner are transition-ready.

The goal is that the success you’ve built in your business becomes significance that continues long after you’ve stepped away.

One thing I’ve observed over the years is that I work with clients who have lots of commas and zeros after their net worth, and I work with clients who have fewer.

The formula for success is remarkably similar.

In my opinion, it comes down to emotional control, understanding your time horizon, maintaining discipline, having adequate liquidity, and clearly defining your goals.

In fact, I believe 80% of reaching your goals is simply knowing what those goals actually are.

Are you trying to retire at a certain age? Support your family? Travel? Leave a legacy?

Once we understand that, we can build the investment strategy around those objectives. Then we can identify the things most likely to derail your plan and proactively address them.

The investments themselves aren’t the destination—they’re simply the vehicle.

That’s an important distinction.

Now, let’s talk briefly about the markets.

The first quarter wasn’t very good.

The second quarter largely made up for it.

Most of the unmanaged stock market indexes are positive for the year, although performance varies depending on where you’re invested.

Large-growth stocks, which were among the strongest performers last year, have lagged so far this year. They’re still positive, just not leading the pack.

Meanwhile, small-value stocks, which struggled last year, have been among the best-performing sectors this year.

Markets rotate.

That’s why diversification is so important.

Bond indexes are also modestly positive this year and continue to provide the stabilizing influence they often bring to a diversified portfolio.

The lesson here is simple.

One quarter does not determine an entire year.

At the end of the first quarter, some people felt convinced it would be a terrible year.

That wasn’t true.

Likewise, just because the first half of the year has been positive doesn’t guarantee the second half will be.

This is exactly why we focus on time horizon and discipline.

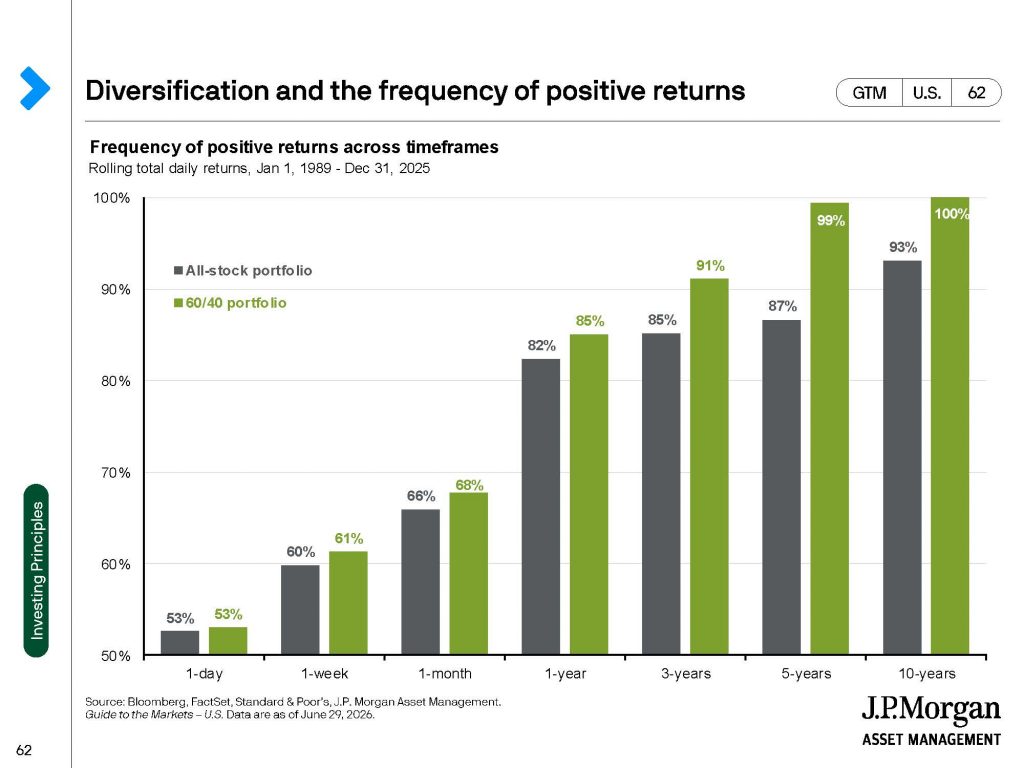

There’s a chart I’m going to put on the screen that’s become one of my favorites.

It looks at a diversified portfolio made up of 60% stocks and 40% bonds using unmanaged indexes going back to 1989.

The farther out your investment time horizon extends—from one day, to one week, one month, one year, three years, five years, and ten years—the greater your historical probability of experiencing positive returns.

Over very short periods, markets can move in either direction.

But historically, the longer investors remained disciplined and stayed invested in a diversified portfolio, the better their odds became.

Our goal isn’t simply to break even.

You could do that by putting your money in the bank.

Our goal is to thoughtfully manage downside risk while helping position you to achieve your long-term objectives.

As we move into the second half of the year, I’ve already planned several upcoming videos where we’ll cover more technical topics, including Trump Accounts and other financial issues you may be hearing about in the news.

One reason I don’t spend much time discussing daily headlines is because you’re already surrounded by them.

Turn on the television.

Open a newspaper.

Browse the internet.

Technical information is everywhere.

But understanding the individual tools—a hammer, a nail gun, or a wrench—doesn’t teach you how to build a house.

The wisdom comes from knowing how all of those tools fit together to create something meaningful.

Our goal isn’t to obsess over the tools.

Our goal is to help you build the life you want to live.

To live with purpose.

To create a meaningful legacy.

To have the freedom to support your family at a moment’s notice if they need you.

That’s what financial planning is really about.

Whether the markets are up or down in any given month or quarter, we’ll continue helping you navigate those details while keeping your long-term goals at the center of every decision.

I hope you understand that, and I hope you’ll always feel comfortable reaching out so we can have honest conversations about where you’re headed and how we can help guide you there.

I’m Mike Brady with Generosity Wealth Management.

If you ever have questions, give us a call at 303-747-6455.

I’m here. Felicia is here. Autumn, Evan, Cassidy, and Sara are all here to support you wherever life takes you.

Have a wonderful celebration of our great country’s anniversary, and we’ll talk to you again next month.

A recession. Inflation. Interest rates. Elections. Geopolitical conflict. The next prediction about what could go wrong.

And yet, despite decades of headlines, uncertainty, and volatility, one principle has remained remarkably consistent: Successful long-term investors rarely win because they can predict the future. They succeed because they remain focused on what matters most.

In his latest video update, Generosity Wealth Management Founder Michael Brady reflects on market volatility, the importance of emotional discipline, and the continued evolution of the Generosity Group family of companies.

The Market Has Always Tested Our Patience

When Michael entered the financial services industry in 1991, the Dow Jones Industrial Average was approximately 3,500. Today, it stands many times higher despite decades of market corrections, economic disruptions, political uncertainty, and global events.

The lesson isn’t that markets move in a straight line.

They don’t.

The lesson is that short-term uncertainty has always been part of the journey.

Investors who remain patient, stay invested, and maintain emotional control often find themselves in a much stronger position than those who allow fear to dictate their decisions.

As Michael often reminds clients:

We don’t want to make long-term decisions based on short-term information.

What We Can Control

The future will always contain uncertainty.

The next market decline is not a matter of if, but when.

That reality isn’t something to fear—it is something to prepare for.

At Generosity Wealth Management, our focus is not on reacting to every headline. It is on building thoughtful strategies that allow clients to navigate uncertainty with confidence.

While we cannot control markets, we can control:

Our planning

Our spending decisions

Our investment discipline

Our risk management

Our long-term perspective

When markets become noisy, these are the things that matter most.

A Bigger Vision for Serving Clients

Over the past several years, Michael has been quietly building something larger than a traditional wealth management firm.

Today, Generosity Group brings together multiple disciplines designed to help clients navigate life’s most important financial decisions.

Generosity Wealth Management

Aligning wealth with purpose and possibility through comprehensive financial planning and investment management.

Generosity Estate Planning

Led by attorney Cassidy Brady, helping families create thoughtful plans that protect what matters most.

Generosity Business Exit Planning

Helping business owners increase value, prepare for transition, and create more options for the future.

Recent additions to the team—including Autumn Davidson and Evan Faber—reflect the firm’s continued commitment to providing deeper expertise and broader support for clients navigating increasingly complex decisions.

Why We Continue to Grow

Growth has never been about becoming bigger for the sake of being bigger.

It has always been about creating greater value for the people we serve.

Whether clients are preparing for retirement, planning their estate, transitioning a business, or coordinating multiple aspects of their financial lives, our goal remains the same:

To provide thoughtful guidance, trusted relationships, and a comprehensive approach that helps clients make confident decisions.

Because wealth is about far more than investment performance.

It’s about creating the freedom to live your values, pursue opportunities, care for the people you love, and build the legacy you want to leave behind.

Full Video Transcript

Mike Brady with Generosity Wealth Management, a comprehensive full-service financial services firm headquartered here in Boulder, Colorado. I am recording this on a perfect Monday morning, even though you’re probably receiving this video a couple weeks after I’ve done it. I’ve got to edit it and get it through compliance, get the newsletter all put together. But this is a beautiful Memorial Day—sunny, not a cloud in the sky, people out there running the Bolder Boulder. I wanted to get this video done. I’ll be heading up to Dubois, Wyoming, where I have a cabin for the summer. I run the whole business right out of there all summer long and have no interruptions as it relates to Zoom, email, phone, et cetera, even though in-person meetings are a little difficult to do. I have a great team here in Boulder, which I’ll talk about in just a second.

At the end of March, I did a video, and at that time I talked about how it had been a tough quarter. The unmanaged stock market indexes like the Dow and the S&P, etc., they were all negative. I said at that time, “You know what, guys, this is normal.” It is normal for there to be declines. We might take two or three steps forward, maybe one step back, and it’s been this way my entire career. As a matter of fact, when I entered the financial services career realm back in August of 1991, the Dow Jones, which is an unmanaged stock market index, was about 3,500. Today it’s over 50,000. How many doublings is that? I don’t want to get technical, but it’s a lot. The same thing with all the other unmanaged stock market indexes—it has been a wonderful 35-year ride with lots of ups and downs along the way. Those people who were patient and had emotional control are the ones sitting pretty, who’ve had a fine ride along the way and are feeling good now.

The same advice that I have given that entire 35 years is still valid today, which is, “Hey, if you don’t have 35 years, that’s okay.” I mean, I’m 57 years old. I may not have 35 years myself, but we are going to have many, hopefully, five- and ten-year time horizons. We’re still keeping our emotions in check, staying invested, keeping our eye on the long term, not allowing short-term trends or information or people whispering in our ear—whether that’s a newspaper reporter or some pundit on TV—to detract us from our long-term vision and our long-term plan. We don’t want to make long-term decisions based on short-term information. That’s what is unhelpful. Emotional control, keeping our eyes on the big prize—this has served me well over the last 35 years, and I believe that it will continue to serve you.

Once again, I told you two months ago, “Guys, this is fine.” Nobody likes it when it’s down, and it’s nice that it has reversed in the last couple of months. We’re sitting pretty so far year to date as of the end of May. Also, let me tell you, there are still going to be some ups and downs for the rest of the year and for the next year and two and three years from now. That is normal—there will always be that.

I want to pivot for just a second and talk a little bit about my company, Generosity Group. It’s something I created a couple of years ago that really is an expansion of what I’ve done for years. Generosity-Group.com—if you ever want to go there, you can see what I’m talking about. It’s really three companies put together.

The first one is Generosity Wealth Management, which I’m kind of wearing that hat right now as I’m talking with you. We align wealth with purpose and possibility—that is what we’ve had for many years, since 2008. So that’s a good 18 years I’ve had Generosity Wealth Management.

The second part of Generosity Group is Generosity Estate Planning. I’m very proud that my wife, who’s been an attorney since 1999, runs that division. She has an estate planning firm called Generosity Estate Planning. I’ll talk more about that as the year unfolds and as 2027 is right around the corner, feels like.

The third one, which I’ll talk even more about in the coming months, is Generosity Business Exit Planning. It’s run by our Chief Business Officer, Evan Faber. If you read the newsletter, which I hope that you do, you’ll read a little bit about Evan. He is a wonderful addition to the whole Generosity Group.

In the last couple of months, we’ve welcomed Autumn Davidson. She’ll be working in the Generosity Wealth Management part of the business. And then there’s Evan, who is currently getting licensed with his Certified Exit Planning Advisor. He’ll soon be—assuming that the test at the end of June works out the way we’d like—a Certified Value Growth Advisor. Both are designations I happen to have as well.

Generosity Business Exit Planning is working with business owners who want to get their business transition-ready for moving to the next generation or selling to someone else, so they can unlock the 80 to 90% of the wealth they have—most business owners have—in their business. This is something I’ve been working on for the last three years or so. I saw an opportunity: I met with many business owners who really weren’t sure what to do with their business. They wanted to get it best in class so they could choose at their discretion, have many options if they’d like, for when they wanted to transition away from that business. Sometimes it’s not our own choosing. Sometimes there’s death, there’s divorce, there’s disagreement with partners, there’s disability.

There are many different reasons why you need to have that in place before any of those things really hit, or before distress to your business—like you’re not thinking ahead, and all of a sudden the business has got a cash crunch or something else. So Evan has come onto the team to help business owners out. We’ll talk a little bit more about Generosity Business Exit Planning in the future.

We’ve got three divisions, and I’ve thought about adding on a fourth one: Generosity Wealth Management, Generosity Estate Planning, Generosity Business Exit Planning, and then at some point—since I’m currently getting my Enrolled Agent license—we might have Generosity Tax Planning as well. Whether that’s with a CPA or how that works, I’m not entirely sure. But we want to have all the needs that a client might have so that we can be the greatest value to our clients. That’s really what’s in the back of our mind at all times: how we can continue to add value to the relationship with the client, so that we are the choice to choose, or for you to recommend us to your friends, your family, your neighbors, your business associates. “Hey, these are the people who can handle what you need, and they’ve probably seen it because they’ve seen it all.”

Anyway, Mike Brady, Generosity Wealth Management, 303-747-6455. Thank you very much for being our clients, and for all your confidence in me, Felicia, Cassidy, Autumn, Evan, and Sarah. Thank you very much for being with us and allowing us to serve you.

Have a great rest of June, and I will see you in July once the second quarter is over.

Market headlines can feel overwhelming—especially during periods of volatility. But not all market movement is cause for concern.

In this latest quarterly update, Michael Brady shares a grounded perspective on what’s happening in today’s market, what a “correction” actually means, and why long-term investors are better served by focusing on what they can control rather than reacting to short-term noise.

If you’ve been feeling uncertain about recent market activity, this is a helpful reminder of what truly matters—and what doesn’t.

Transcript

Hi there. Mike Brady with Generosity Wealth Management, where we align wealth with purpose and possibility. I’m here with my first quarter review, the rest of the year preview video, and newsletter.

I’m asked every once in a while why I don’t get more technical. I touch upon technical topics in my videos, but I don’t go very deep, to be honest. One reason is that when I started 35 years ago, having a technical advantage was the big thing. Now there’s so much information on the internet, on TV, on the radio, discerning what’s important and what isn’t is more difficult.

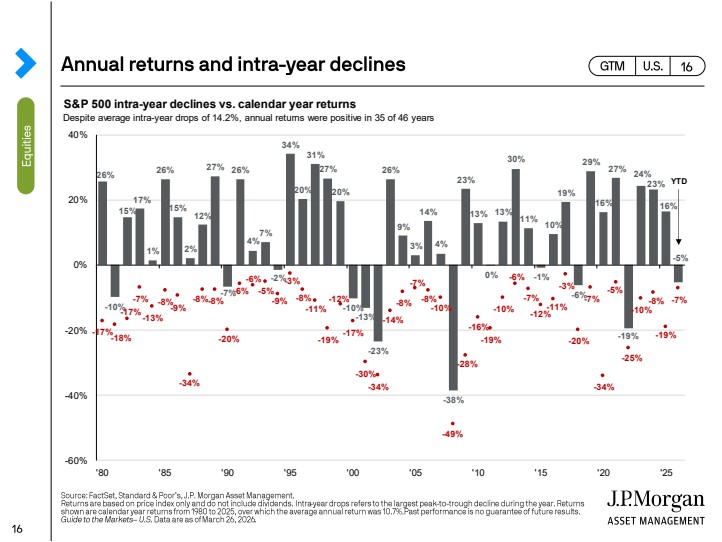

As I view the world now, we are close to a correction at the time I am recording this video. A correction is a 10% drop from the most recent high. It doesn’t mean a 10% loss for the year. It doesn’t mean 10% like you’re never going to get it back. It’s a 10% drop in an unmanaged stock market index. As of this moment, the S&P 500 and the Dow are flirting around with it: 8%, 9%, 10% depending on the day. Most corrections, when you look back over a long period of time, last between three and eight months before they recover. It’s not three to eight years. It’s three to eight months. They’re usually relatively short in duration.

On the screen, you’ve seen me show this before. It is normal for most years, as seen in the red numbers below the x-axis, for there to be corrections of double digits or more during the year. The numbers on the top of the x-axis are what the year ended at, and it does not mean that it ends the year negative. I like to get back to the basics, which is our attitude, whether we’re paying attention to the right thing, and what our particular biases are.

I like to think of the difference between complicated and complex. Complicated is a rocket to go to the moon: A plus B plus C. It has a million different parts, and if you follow the directions, you can duplicate these rockets and build ten of them one after another. Complex is raising a child. You think you do A, and they come back with B because that’s what they did the last ten times. But sometimes they come back with C or D or something else. They come back with an answer you weren’t expecting, and then you respond in a different way, and so on. That’s complex. Human relationships are complex. If I do a certain thing all the time, someone else may respond in a certain way, but then my reaction to their reaction is different, and it continues. That’s complex. It’s not necessarily complicated.

I bring this up because I get tired of the news saying the market went up because of A, or down because of B, as if that’s the whole reason. It’s not that simple. We need to look at it not as static but as dynamic. If I do something, someone else changes their behavior. If I’m selling hamburgers for $10 and I want to increase my profit, I don’t just double the price, because people will buy fewer hamburgers. So when I impose something on the consumer, they react accordingly. The markets are quite complex, and I believe a diversified portfolio is incredibly important. I don’t believe in individual-issue risk, such as focusing on a single stock or bond. I don’t believe that’s the best way for an investor or client to reach their financial goals over the long term.

I also believe that matching the diversified portfolio with the duration or time frame of your goals is crucial. The money you need in three months is different from the money you need in 30 years. If you’re 60 years old, I hope you know that you have a 30-year time horizon. We have to think about that. If you’re in your 50s, 60s, or 70s, you still have many five- and ten-year time horizons, while you might also have short-term needs, like your monthly income.

For today’s review, it’s been volatile in the first quarter, and that’s unpleasant. Nobody likes it when it goes down. We have risk aversion, meaning we feel more pain with a 5% loss than happiness with a 5% gain. That’s human nature. We have to acknowledge that risk aversion. We have to stay calm, rational, and in control of our emotions. Looking at the rest of the year, I don’t know what will happen. My crystal ball isn’t perfect. But if we have a good diversified portfolio, I think it’s the best way to live in an uncertain world, because the future isn’t always known. It’s always uncertain, even if we don’t always notice it.

Let’s keep the buckets in mind: things we can control, things we have some control over, and things we have no control over. Let’s not spend all our time on the things we can’t control. Let’s spend the majority of our time on the things we can control, like how much we save, when we retire, how much we retire on, and some elements of our portfolio and financial goals. That’s my first quarter newsletter and video. I’m always here if you need anything, even if I’m traveling or in Boulder or heading up to Wyoming for the summer. I can run the business from up there, near Yellowstone in Dubois, Wyoming. My number is 303-747-6455.

Mike Brady. I’m always happy you’re my client. If you’re not my client, consider becoming one. Thank you.

Recent headlines about global conflict and market volatility can make investing feel uncertain. When emotions rise and news cycles move quickly, it’s easy to feel pressure to react.

In this video, Michael Brady of Generosity Wealth Management shares a timeless perspective on navigating moments like these. Drawing on decades of experience, Mike explains why emotional control and discipline are two of the most important ingredients for long-term financial success.

Markets will always experience ups and downs. Geopolitical events will always occur. The key is not predicting every headline, but building a thoughtful plan and maintaining the perspective to stay on course.

Mike also shares a helpful reminder: intra-year market declines are normal, even in years that ultimately end positive. Long-term investing is about progress over time — not reacting to every moment of uncertainty.

At Generosity Wealth Management, the goal is to align wealth with purpose and possibility, helping clients live well today while preparing confidently for the future.

Transcript

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive full-service financial services firm headquartered in Boulder, Colorado. Although I am in Michigan right now, if you’re ever wondering what my childhood backyard looks like, that is it. My mother’s in assisted living. She moved there over the summer, and I’m doing the last little bit in my childhood home. My parents have had this house for 50 years, and I’m helping do the last little bits in order to put it on the market and close that chapter.

I did a video about a week ago that was going to go in this newsletter. But it did not get sent out because I’m replacing it with this video. While we were editing the newsletter, the Iran–Middle East conflict came up, and I thought I’d be a little more timely and remind you of certain lessons that are tried and true.

One of them is that we have emotional control at all times. If you want to be successful in the financial world and reach your financial goals, it is my opinion that one of the first things you do is have emotional control. Remember that the media—whether it’s print, scrolling, or TV—often tries to elicit emotion from you, not necessarily inform you. If you’re getting excited or upset, check yourself.

One thing we can do is ask, “How am I feeling right now? What’s causing that? If it’s not helping me, stop doing it.” It’s just that simple.

The other is discipline. Have the discipline to know what our plan is and move towards it. Periodically I hear people say, “Well, we’re obviously at a high.” First off, when the word “obviously” is in anything in our industry, you know it’s not obvious. But the question is, are we at a high in the unmanaged stock market indexes? The answer is, we might be at a high from where it was 5, 10, and 20 years ago. I certainly hope it’s at a low in comparison to where it will be 5, 10, and 20 years from today. That’s all that really matters, because we can’t live in the past, but we certainly can live, and we will hopefully live, the future. Why else would we have investments if we didn’t believe that they would be higher 5, 10, and 20 years from now?

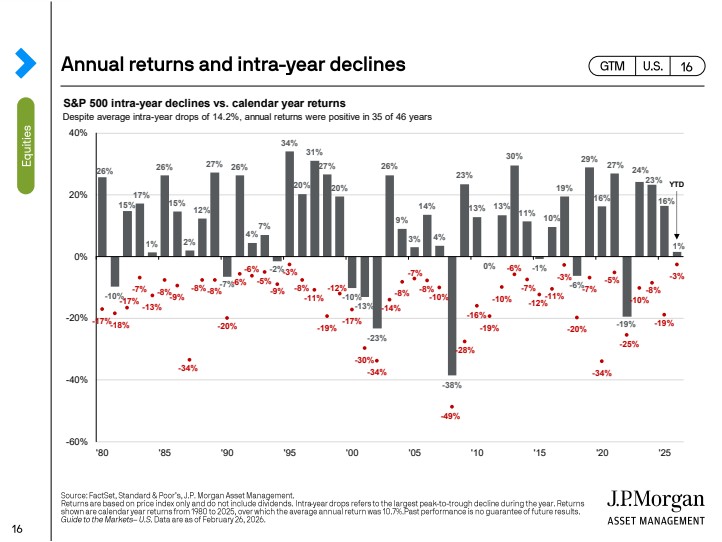

Up on the screen is something that I like to remind people of: the numbers below the X axis are the intra-year decline, and it is normal for there to be declines throughout the year. It doesn’t mean that the end of the year ends negative. It is normal for there to be declines.

Someone asked me the other day, “Mike, your videos are not very technical.” And my answer is yes, that’s by design. If you want technical, you can go to any business news channel and get that technical analysis. You can open up print media or a business magazine or newspaper and have all kinds of technical analysis. Twenty or thirty years ago, I could wow you with that information and charts. Today it’s all free and available. But what is more important than all of that technical data is what it actually means. What are the ingredients for success that they might not be talking about in the media or that you might not see others talking about in your neighborhood or community? That’s what I’m here to present: what I believe, and my beliefs have come from decades of experience in discipline and emotional control.

Know your liquidity, have your duration in mind, and then execute properly. Money that you need in two weeks is certainly different from money that you need in five, ten, or twenty years. Even if you’re in your 60s or 70s, we hope that you will have many five- and ten-year timeframes going forward.

I want to bring us back to the fact that geopolitical events will always happen. The market will always go up and down historically. The way I believe is that if you’re so averse to risk or so afraid of any kind of decline, you’re not going to get the ups. It’s three steps forward, maybe two steps back. Three steps forward, two steps back, but you’re progressing along a path. It’s no different than if you’re so afraid of a relationship—friendship or romantic—of being hurt that you’ll never find true love. It’s the same when trying to reach your financial goals. We need to mitigate risk; we can’t eliminate it.

We have to ask, “What’s our duration?” Are the investments we’re in consistent with what we want to do? Can I keep my emotional control, and am I disciplined when things happen that I know are going to happen, like the market going up and down or geopolitical issues or things in the news or in our own country? These things have always happened, and they will continue to happen. How am I going to react?

Is the purpose of my money to make me happy? I would say yes, to live your life so you’re not a burden on others. Your purpose and possibility is really what we talk about—Generosity Wealth Management aligns wealth with purpose and possibility. If that’s the case, then let’s get immune to those external things and stay with our plan. Be peaceful and calm in sometimes non-peaceful situations in the world, but we can be our own oasis.

So, Michael Brady, 303-747-6455. Give me a call or send me an email if you ever feel like you want to talk about something. Let me know, and we can have that communication. Have a great rest of the day, great week. Bye.

2025 reminded us of something easy to forget in noisy markets: certainty is an illusion. With 24/7 news, constant opinions, and confident predictions everywhere, it’s tempting to believe someone knows exactly what comes next.

They don’t.

At Generosity Wealth Management, we believe the real value isn’t prediction — it’s perspective.

Transcript

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered right here in Boulder, Colorado. It is the end of 2025. So this is my 2025 review, and I would say it’s more lessons learned, because you can have all the technical information about 2025. You can read it, you can watch it on TV. I mean, when I started in this industry 34 years ago, you know, it was hard to find that information. People genuinely didn’t know. Now we have 24/7 news and the Internet, and I’m just telling you, you can read more analytical stuff than I can provide you in this particular video and this newsletter. So I want to do it at a high level, but I also want to do the 2026 preview, which is very light because I don’t believe in that. I believe that the future is inherently unknown. And so we’d better have some conviction, some foundation, some base that is, you know, key that we need to remind ourselves about. And that’s more important to spend that money than trying to guess what 2026 is. Because frankly, I could flip a coin, you could flip a coin, and one of us is going to be right. I mean, it’s that simple.

The problem with many pundits is that they are trying to be very exact about something impossible to be exact about. The way I like to think of it is the economy and the stock market. It’s not math, it’s not physics. It’s more like biology. Math is A plus B equals C. Physics is, hey, these are the rules of physics. Biology, that’s the economy, and that’s the investments. You know, even the smartest doctor is not quite sure what’s going to happen because it’s so complex. There’s so many variables. Well, wow, the other people I gave this poison to, they died, but you’re doing okay. Or the other way around. An antidote that might work for you doesn’t work with somebody else. And side effects and counteracting. That’s why anesthesiologists get paid so much money, is they have to keep all these different—you know, this thing helps and this thing hurts—and you know, on balance, this is the way, you know, hit these dials to help a client out.

So, you know, the economy, the investments, they’re like biology. It’s like a body. It’s a very complex system. And so, I’m hoping that one thing that we will take away from 2025 is some humility up on the screen.

I have shown the intra-year, and I’ve just circled it: all those red numbers, that’s how much a decline was within that year. And you’ll see that it is normal for there to be a decline of over 10%. Double-digit declines. That’s normal. And this year was no different. The S&P 500, which is an unmanaged stock market index, was down 19% at one point this year, but the year did not end with a negative 19%. You can see throughout the graph that, on average, three out of four years are positive, and one is negative. Okay, sometimes they’re strung together, you know, negative, negative, and then positive, positive. There’s a whole number of different ways that it can play out. But on average, when you hold it for a long time, three out of four are positive, and one out of four are negative. But almost every year has a negative decline throughout the year, so we shouldn’t be surprised when it happens. What’s very frustrating about this year is that the sky-is-falling crowd comes out, as it did in March and in April, but with so much confidence. Not the, well, I think this is going to happen, I think this is going to be the impact—it’s definitive statements of it will, and that’s just not true. I hope that we take away from this year that that which you hold with such conviction is sometimes wrong.

I have humility in what I do with clients all the time. Now, I might hide it. Okay, I mean, those of you who know me well saying, wow, he talks with a lot of confidence. Well, I talk with some confidence because I’ve seen it, 15,000 trading days since I started. When I started back in 1991, in August of 1991, the Dow was at 3,000. And then I heard people say, wow, it could never get above 5,000, never get above 10,000, 20,000, 30,000, 40,000. I mean, every single time it’s obviously at a high; well, it obviously can’t get any higher. Well, you know what, I’ve heard that my entire career as it went from 3,000 to 5 to 10 to 15 to 20, all the way up to where we are today. The Dow Jones, which is an unmanaged stock market index. This year, almost every one of those unmanaged stock market indexes were positive across the board—S&P 500, bond indexes, international, you name it. It was a very good year, despite what all those people on TV and all—if you’re doom scrolling on your Internet news feed—say how everything is going to be absolutely horrible. Many of those same people might be saying the same thing in 2026. They’re just trying to be right. Oh my gosh, I can’t say that I was wrong, it just hasn’t happened yet. Well, whatever.

I believe that if you don’t think that five years from now the market is going to be higher than it is today, why would you have any investments? If you don’t believe that, move it in cash, for goodness sakes. Okay? So I don’t know if this next year, 2026, will be negative. I don’t know if 2027 will be negative. But I feel with high confidence—but no guarantee—and I feel with high confidence through my experience and the experience of others over a hundred years that it’s a good bet that I will win on that if I have investments properly matched to me and my emotional level, my goals, okay, my risk level, that five years from now it’ll be higher. Whatever mix that I do, why else would I have investments? Let’s keep our eye on the ball. What happens in a month and a quarter doesn’t really matter. We keep our eye on that ball.

So one of the things that I recommend and I repeat over and over again is emotional control. If you don’t have emotional control, I don’t know what to tell you. People are going to whisper in this ear, and they’re going to whisper in that ear, and you’re going to move this and this and this, and you’re going to be so flexible that you’re really bendable, and you’re not going to be happy. The way I like to describe it is, you know, one person worried every day throughout the year, another person didn’t. The returns are exactly the same. One person just had a very poor journey, the other one believed in the system, had their thing, and executed it. So knowing what your purpose is—I mean, Generosity Wealth Management, I want to be very clear on this: we align wealth with purpose and possibility. What that means is we use wealth to help you. What is your purpose? What do you need today? What do you want to have happen so that you can be generous with yourself? What’s your purpose with your family? What’s your purpose in your community? What’s your purpose maybe in the future, but what’s also possible that you haven’t even imagined yet? Okay, so let’s have that conversation. That’s what the value is of Generosity Wealth Management. We help explore that and bring alignment of wealth with purpose and possibility, and we do that in a number of different ways.

I want to talk about one of some of the things I’m very proud of in 2025 is we really upped our game as it relates to retirement analysis. You need to know what your number is. You need to know how these balls in the air come down into an equation that leads to the outcome you want. And hopefully it’s positive; let’s try to avoid the negative. But what can happen proactively so that’s not just chance? What are the things that we can control? What are the things that we can’t control? And the wisdom to know the difference. We really upped our game as it relates to tax planning so that we can provide you with our thoughts, some talking points that you could have with your tax professional. I’m not a CPA. But I work and brainstorm at a very high level with you and with your CPA, because I believe that this is something—it’s most people’s single biggest expense: taxes. So you’ve got to be an expert in it. Retirement accounts outside of your house—it’s most people’s single biggest asset. I have to be an expert in it. I joined the Ed Slott Elite Advisors, and I’m very proud of that. My knowledge has dramatically increased. And of course, you’re the benefactor of it. And I want you to ask me tough questions. I want you to talk about me with your friends and work colleagues so that they know that they’ve got an expert that they can come to. I work with business owners, I work with people who are retired and not retired. I want to work with good people who I like, like you, if you’re my client already. Because I got to tell you, this is the truth: there’s not a single client that I have that I don’t like, that I don’t kind of look—and there’s no client that is like, oh God, I got to pick up the phone, or I got to give them a call. No. Okay, they weed themselves out. I spend a lot of time at the beginning of a relationship to find the people that maybe were not a right fit, and that’s okay. I want to attract the right people. I don’t chase people, I attract the right people, and then we kind of date. We decide we’re going to be right for each other, but if for some reason we screwed up, I kind of help you find that, or you find out on your own that maybe we’re not right for each other. So I want to work with people that I have lots of chemistry with, they have problems that I can help, that I can provide value to you first, so that of course, you can see the value in what I’m bringing as well.

2026 I want to summarize. I don’t know if it’s going to be up or down for the unmanaged stock market indexes, but I do know the value of diversification. Knowing what your purpose is and what the duration of your money is, is important. I know that discipline, okay, whatever that discipline, and emotional control, I know that these things—every year, I could say 2026 or I could say 2023 or the year 2000—they’re the same throughout the years of my career. These things I keep coming back to, and also, of course, humility. Hey, we don’t know everything, so let’s do the best job that we can and keep control of our emotions as we move forward.

I do want to have more clients. So if you—my client, who I love, all right, who I am willing to jump on a phone call and a Zoom with and give you the best advice that I can, and the experience of what has worked and not worked with other people—if you know friends, family, work colleagues that are just like you, I want to replicate you. Then have them contact me, and we’ll determine independently if it works out. I am going to expand my business. We’ll talk about it—not today—but I have new and fun and cool things that are in the pipeline that you will hopefully see, and I’ll roll out to you in 2026 and even into 2027, and that is all in service of the client, because when the client sees the value, if I make you a raving fan, then you will talk to other people, and that’s how my business grows. And of course, as I bring in other junior advisors and replicate some of the knowledge that’s in my head with them, to serve you continually, that’s how we can be of benefit to the community. And you’re part of the Generosity Wealth Management community. Felicia and I, Sarah Cassidy, we thank you for being our clients, and we just really want to have a wonderful 2026, and we’re glad that we’re doing that together. So, Mike Brady, 303-747-6455.

As 2025 nears its end, Generosity Wealth Management founder Michael Brady takes a moment to pause — not just to reflect on a strong year for markets, but to share insights on what truly drives long-term financial success.

In his latest video update, recorded just before Thanksgiving, Michael discusses why patience, emotional control, and thoughtful planning often matter more than the latest market move. He also highlights his recent speaking engagements in Las Vegas and Austin, where he explored how technology like AI can deepen advisor-client relationships and how tax-smart retirement strategies can build wealth that lasts.

Because at Generosity Wealth Management, it’s not just about managing investments — it’s about aligning your money with your goals, your time horizon, and the life you want to live.

Transcript

Hello clients and friends. Mike Brady here with Generosity Wealth Management, a comprehensive full-service financial services firm headquartered here in Boulder, Colorado. Today I’m recording this right before Thanksgiving. Not sure when you’re going to get the newsletter, as I’m writing the rest of it and adding this video, but it’s been going really well.

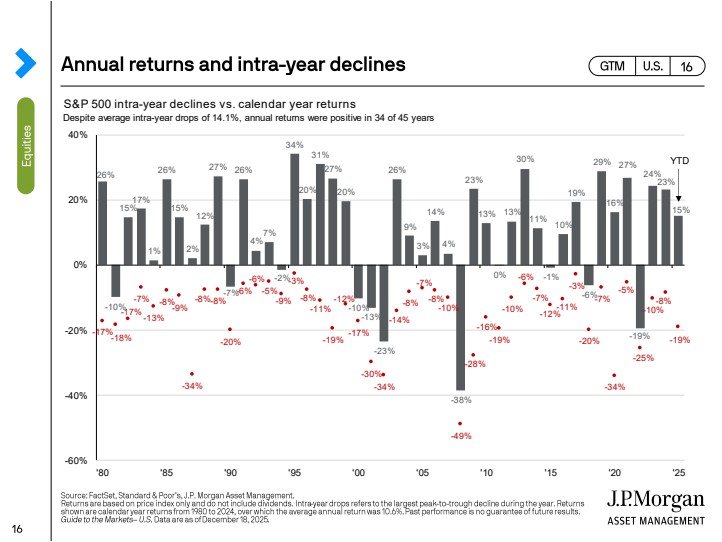

From an investment perspective, the unmanaged stock market index is really on a tear. I think that it’s important for us to remember that, from a market point of view, it is normal for the unmanaged stock market indexes to have a double-digit decline that happened earlier this year. Who knows how the rest of the year is going to turn out? But I am always keeping clients focused on what their time duration is and making sure that it matches up with what their goals are. Because, frankly, the investment management part of what I do feels like the simplest part:

Where do you want to go?

Which tool in the toolbox helps you get to what your financial goals are?

What’s your time horizon?

Can you keep your emotions in check?

And of course, avoid stupid stuff.

I made plans for people 20 or 30 years ago, and some met their goals and some didn’t. It usually had nothing to do with investment A or investment B, but it did have to do with some of the abstract, some of the satellites around that core of having good investments, which is you got excited about your brother-in-law’s Chihuahua farm or you did some other investment that sounded great at the time but really didn’t help you achieve your goals. Or it was that you simply didn’t save enough, or you had some other unfortunate incident happen in your life, unable to work, loss of your spouse, things of that nature. That’s why I really want to keep all those things in mind.

Today, though, I wanted to pivot from the investments, which are going great this year, and I’m hoping that 2025 ends in as good a situation as it is right now here in November.

But I want to talk about some of the things that have been going on from a seminar perspective. I just spoke in Las Vegas recently, which was great, and in my newsletter, I’ll talk a little bit about that. I was talking about how I use my note-taking AI to help me be more efficient and stay present in every client meeting. I’ve had clients for 20 years, 30 years, and of course, I’m always bringing on new clients as well. So thank you to those of you who continue to refer your friends, family, and acquaintances to me so that I can help them out. I use my AI note taker because it hears things I might have missed. It really helps me be present in the meeting when you and I are talking, so I can hear what the problem is, what the issue is, and what your emotions are, so I can then, of course, come back with the best recommendations for you. I was honored to be a part of that panel there in Las Vegas, talking about how I believe AI is going to revolutionize the relationship that advisors like me can have with our clients, can go even deeper, and really understand where you want to go so that we can come up with the solutions in order to get there.

I was also recently in Austin, Texas, at an Ed Slott Elite Advisor seminar, and that was training for me. Most people’s single biggest expense, aside from everything else, is taxes. Most people’s single biggest asset outside of their house is their retirement account. So I have to be an expert in everything retirement accounts, and I have to be an expert in taxes, even though I’m not a CPA. I’m not going to do your taxes, but I work at a high level with your tax planner. Now, here’s one thing I like to tell people: do you have a tax preparer or a tax planner? A tax preparer costs you money; that person is a historian. They take your number in that box, put it on that line, and provide very little proactive guidance. A tax planner helps save you money. They are working with you throughout the year and proactively giving you advice. They are in the wealth-maximization business, like I am, not necessarily in the tax-minimization business. I think that’s a really key distinction: they are there to sometimes say, maybe we pay a little bit more taxes this year, but over your lifetime or over multiple years, this is in your best interest. You’ll actually be wealthier in the long run if we pay a little bit more in taxes right now.

This leads to my next conversation, which is satisfaction and gratification. There’s this old study called the marshmallow study, where they had a bunch of kids, around 6 years old, brought into a room and put a marshmallow in front of them. They said, “You can have the marshmallow now, but I’m going to be back in six or seven minutes, and if you wait that long, I’ll give you another marshmallow.” All they had to do was delay their gratification for a few minutes, and they would get twice the reward. Those kids who were able to delay gratification tracked better throughout their lives than the control group, who needed instant gratification. They found that those who delayed gratification had greater life satisfaction, greater career satisfaction, were married longer, had higher incomes, and had higher net worth—all of the things we want in our lives. They were able to do it because they were in control of their emotions and delayed the gratification.

One of the things I talk with clients about all the time is what’s right for you. Is it a Roth IRA, a Roth 401(k), where you pay the taxes now but delay the gratification for the tax-free income all along the way and the tax-free withdrawals? Or do you want that instant hit right now, which is a tax saving today? It’s really an individual choice. We have to individually do the math, but this is something I want to work with you on, and I want to work with your CPAs. My ask of you is that I want to grow my business. I want to help your friends and family and acquaintances, and one of the value adds that I bring is that I really listen to you. I use the AI in order to help my notes—the boring part—so that I can truly be present and hear what you want to do and match up those investments. Here’s the value add: I’m going to really look at what your assets are and position them accordingly, and be an expert in them. Like I said, that’s why I’m continually traveling to go to seminars, to be the absolute expert in your biggest types of assets, and also work with your CPA on your biggest expense, which is your taxes.

If we manage and control that expense and hopefully minimize it over multiple years and over your lifetime, then you’re going to be better off. That’s what I want to do with clients. With that extra money, with those extra assets, what do you do with it? That’s where the generosity comes in, so that you can be generous with yourself, with your family, and if you believe it’s in your best interest and the community’s best interest, you can be generous with your community, both local and global. That’s really what I’m about, and that’s why I’m saying to you: I want to be that trusted advisor. If we keep some of these key things in mind, then I believe that you’re better off, the community is better off, and your family is better off if we keep some of these fundamentals in check.

Michael Brady, Generosity Wealth Management, 303-747-6455. You have a wonderful rest of the year. You’ll hear from me again in January as I recap what happened in 2025 and, of course, as we look forward to 2026. Thank you.