Wealth is the ability to fully experience life. –Henry David Thoreau

2018 is but a distant memory as 2019 has come in fast and furious! In a very short amount of time we wiped away all of 2018’s losses in the unmanaged stock market indexes. This is a quarter that investors and financial advisors dream of, however now more than ever it is time to keep a level head. You hear me say the same thing over and over, and for good reason. Investing is a commitment and in this commitment you need to stay calm.

In the video I discuss humility and bias. Why? Because none of us can predict the future, we do our best to try by watching the news and this forecast and that one, however these media reports consistently report to stretch either negativity or positivity. Middle of the road, even newscasts don’t make headlines, so it’s our job to take everything with a grain of salt.

Watch my short video or read the transcript below and I give a quick breakdown of what we’ve seen so far in 2019.

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive financial services firm headquartered right here in Boulder, Colorado.

First quarter is over of 2019 and it was a banner year. These are the types of quarters that investors and financial advisors, frankly, live for. In a very short amount of time we wiped away all of 2018’s losses in the unmanaged stock market indexes.

Today I want to talk about humility and bias because I think that they’re very important. I mean just three, four, five months ago there was so much things are horrible and the stock market has continued to go down. A lot of pessimism. And then there was lots of optimism in January and February followed by, just three or four weeks ago I was reading an awful lot of pessimism. And the reason why I bring this up is humility. I don’t know the future any more than you know the future and definitely not any more than those that you see on TV or writing those newsletters or those magazine articles. I mean just take it with a grain of salt, okay, because I think that it’s important for us to have a long-term plan, stick with it and not get too deviated by their particular biases.

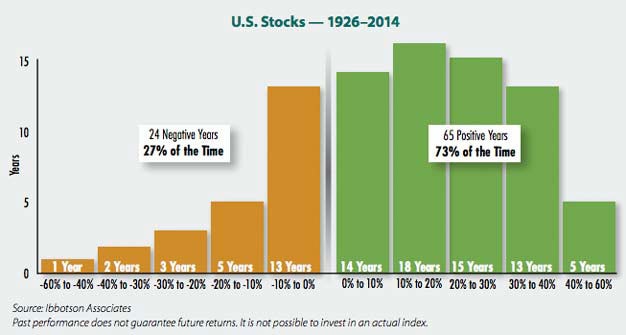

And so now I want to kind of shift into bias. The bias of those in the media is not to be even-keeled. It is to be sensational either to pump things on the upside and be overly enthusiastic or to be very negative. Just to say oh my god, the world is about to end. Because both of them get headlines. Both of them run the viewership up into record digits. Saying “oh, everything’s all fine. Let’s just do the middle way” doesn’t really fly. And so you’ve got to read or listen to your news that way with that particular filter. I would actually argue that’s a good way to go through life because what is your personal bias? Is your personal bias to be optimistic or to be pessimistic? Right now I’m just telling you that going back to 1929, three out of four years is positive. One out of four has been negative in the unmanaged stock market indexes. So that means if you’re pessimistic you’re really only right one out of four times. Being pessimistic might serve you well if you are in a bad neighborhood, to keep your guard up, to be fearful. But it doesn’t really serve you very well, frankly, in your investments.

So think about it even from a relationship point of view. If you are afraid of being disappointed in friendships is the answer to have no friends? No. The answer is why don’t I look at myself and see if I can moderate my reaction to my disappointments when a friend might disappoint me. That’s the more logical way I would argue in your relationship or friend relationships but also as it relates to investments. Is the better way to be overly optimistic, overly pessimistic or to take your news with a filter but look for the even way? To understand that hey, my bias might be pessimistic but wait a second, is this the real truth?

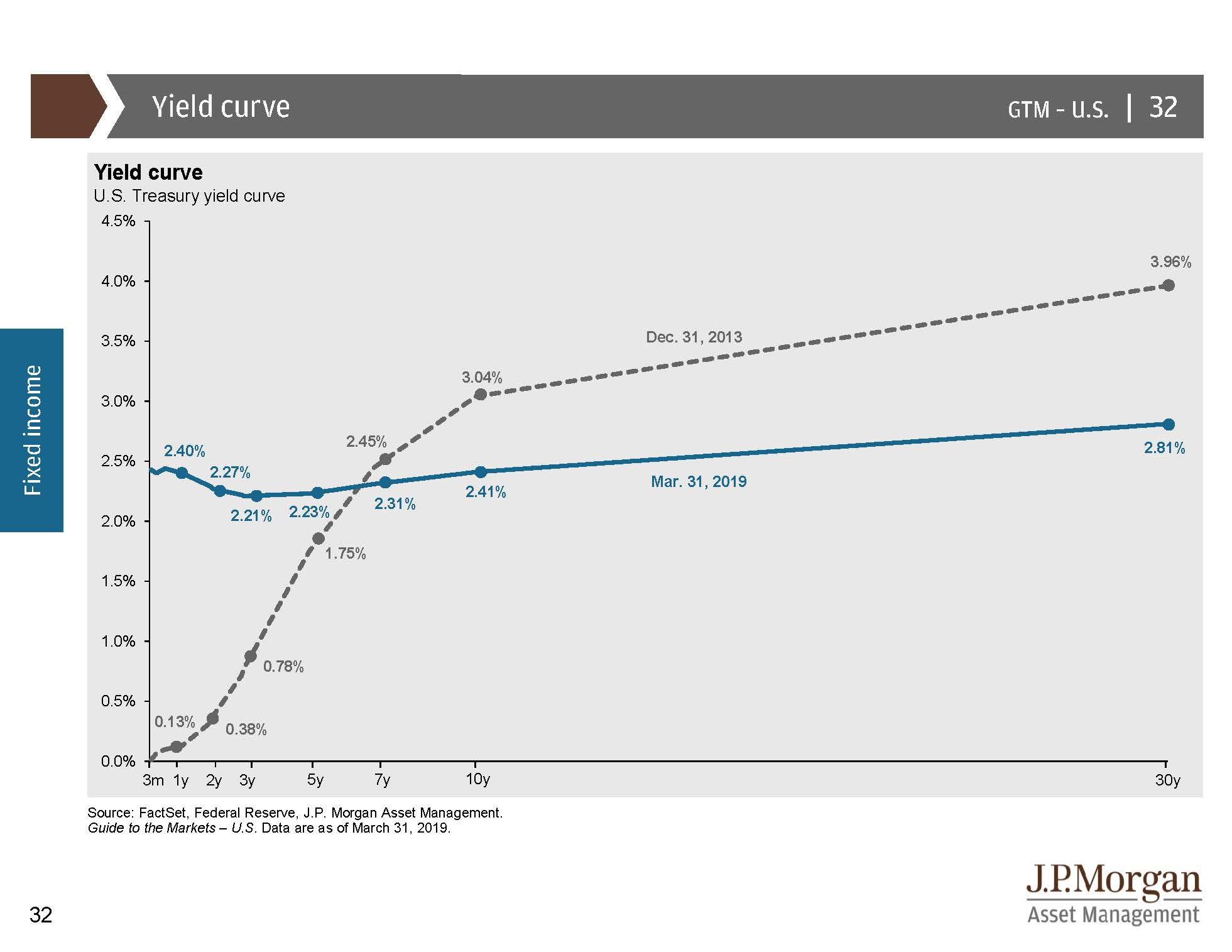

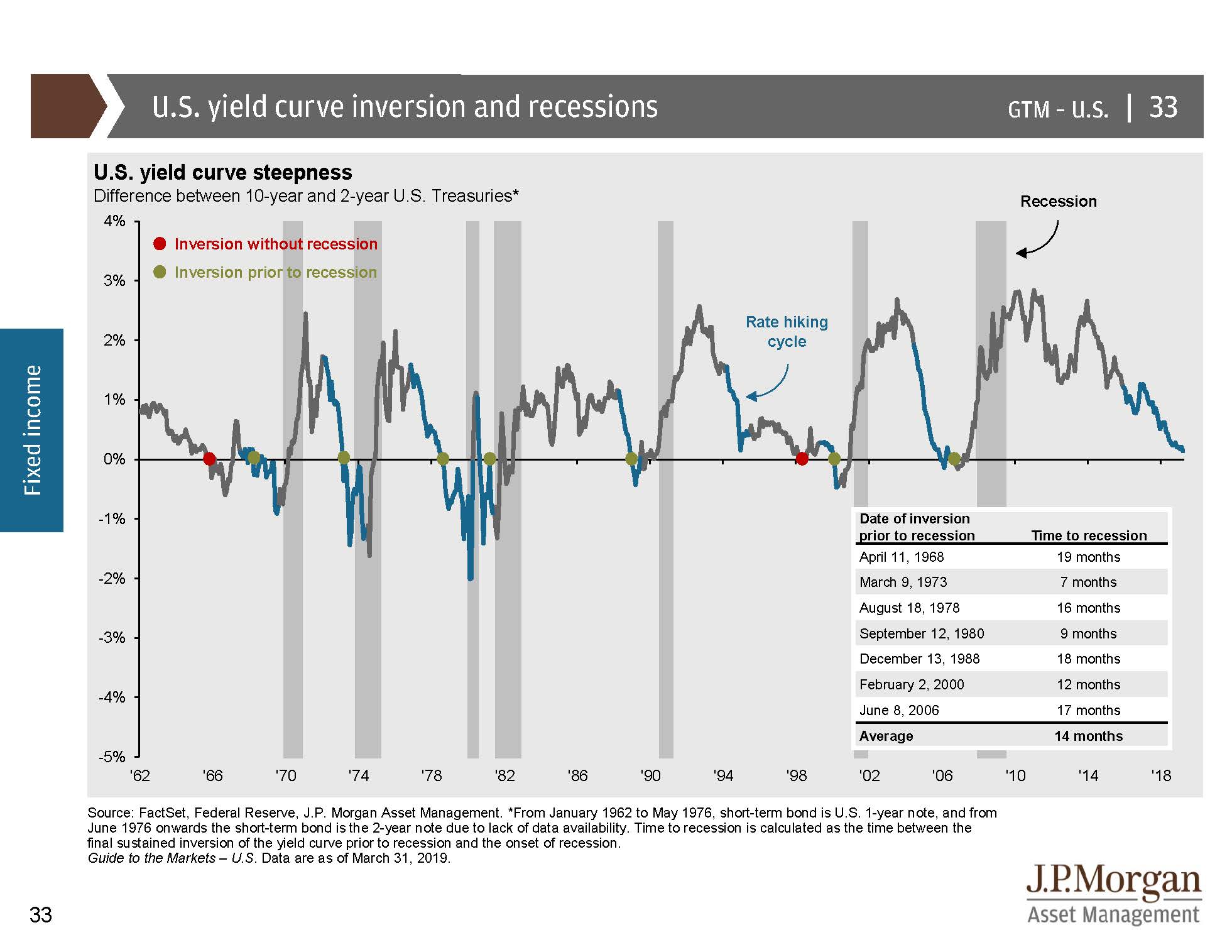

Recently and before I end today’s newsletter there’s been a lot of talk about the inverted yield curve and I wanted to talk about that for a second. The economy is not the stock market. That’s very important to make that differentiation. The inverted yield curve and we can talk about the difference between the ten year and the two year (maybe I’ll do that in an instructional video next month), but when you see that yes, that has led eventually or at least predicted most of the time to a recession. But it’s been a huge differential between seven months and nineteen months. And during that time as I look back over the last – I’m going to put a graph up there on the screen – there’s been some nice stock markets during that timeframe and some nice times to be invested.

I would argue that since there’s a huge variance there of delay and some false positives that it’s not as good of an indicator as you would be led to believe. But even then it’s an indicator of the economy. The economy is not the stock market. It’s very important to remember that. If you look back at the early 90’s there was an indicator of a recession which did happen. However, does that mean that you shouldn’t have investments? No way. The 90’s were one of the best ten year timeframes ever and I certainly wouldn’t take that as an indicator. The last ten years has been a relatively moderate recovery from the Great Recession when you look at all the underlying GDP numbers versus the averages. However, this last ten years I’m certainly proud that many people invested in the markets and kept their investments over the last ten years. The unmanaged stock market indexes have been very favorable even if the economy was not as ripping and roaring as they have in prior decades.

Anyway, Mike Brady, Generosity Wealth Management, 303-747-6455. Give me a call at any time. Have a wonderful day. Thank you. Bye bye.

The first quarter of 2017 is over, and it was a good one.

The “Trump Rally” continued almost unabated, and new records for the unmanaged stock market indices were made most weeks.

It’s nice to have a “tail wind” behind you in your investments, but one quarter does not an investment philosophy make.

In my video to the right, I talk about the 3 most important things I’ve found to be helpful in reaching your financial goals.

And they’re not complicated.

FULL TRANSCRIPT:

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive full service financial services firm headquartered right here in Boulder Colorado. Today I want to talk about their first corner quarter and I want to talk about the rest of the year, but of course I’m always going to throw in some general advice. It sounds like I’m a broken record at times because I do bring up certain things over and over again, but I think that they’re the foundation of as I view the world how clients should be successful. The first-quarter very strong for almost all of these unmanaged stock market indexes; a continuation of an upward trend every sense the election. So November/December really just kind of carried forward into January, February and into March. I’m doing this video a couple of days before the end of the quarter so I don’t have the numbers right here to spit out at you but I will include them in the written news letter.

I was with a lawyer friend of mine, we serve on a board together, and we were looking at some solution to a problem. And I’m like, “Gosh, we really need to have an out of the box solution and here’s an idea.” And he’s like, “Mike that sounds like an out-of-the-box idea but it really isn’t. I’ve been a lawyer for 30/40 years and that’s what everybody always comes up with.” I’m like okay great I kind of felt stupid. But the reason why I brought that up is from his point of view he hears it time and time again, but to the person who’s bringing it up it sounds new and unique. And I’ve now been meeting with the clients, been in the investing world the financial services world for coming up on 26 years and I have seen ups and downs and sideways. I’ve seen kind of everything that can happen over 26 years. And when the unmanaged stock market index the Dow was at 10,000 people would come in and say well it’s quite obvious that the market is at a top. And I’d be really? Why is it obvious? And then, of course, when it’s at 12,000 and 15,000 and then it’s taking a little while to go from 18 to 20 in the last year or so but it’s like well it’s obvious it’s at a top. And even now as we end this quarter every once in a while I’ll hear someone say it’s so due for a correction and it’s obvious that it’s at a top. And my answer is there’s always corrections. I mean you’ve seen that chart probably, and I’ll throw it up on the screen again at some point during this video, but it’s normal for there to be declines in the market of some type. I mean that’s the normal that’s not the abnormal thing and so that’s just part of investing. And so while it might seem obvious that we’re at a top or that something is happening from your point of view, nothing is obvious. The future is always being written.

And we as investors are always making probabilistic predictions, hey I believe that having a diversified portfolio is probably going to be good for me and this is the probabilities of it. Or I ought to have all equities let’s say, one person might say, or I need to have all bonds. I mean these are just probabilities that we’re placing about the future, but the probabilities are never 100 percent. So when someone comes to me and says well it’s quite obvious, nothing is obvious.

I was meeting with a wonderful couple. I’ve known them actually one of the two for a long time, I mean it’s actually wonderful that both of them are just about to graduate med school, a great meeting. And we talked about investing and I said, “Well gosh, in your world there’s probably simple things and complex things. In order to have a good life you probably have to eat well, exercise and don’t smoke.” And they kind of laughed and were like, “Yeah, that’s probably about the best three pieces of advice.” And I said, “Well in my world it’s very similar it’s know what your income and expenses are on a monthly basis and make sure that your expenses, of course, are not greater than your income. Number two is avoid stupid stuff, that Chihuahua farm sounds great or some investment sounds great kind of avoid stupid stuff, and then three is know that there’s going to be things that are going to happen that might derail you from that plan. And that might be the loss of your spouse, the loss of the ability to work, things that perhaps can be fixed by buying some insurance. And so it’s understanding those things that we can control and those things that we can’t control and being comfortable with the things that maybe we can’t solve but also having a backup plan, whatever that might be. Or that backup plan might be I’m just going to have to deal with it. I’m just going to have to minimize the impact it can have in my whole plan but I’m probably going to have to suck it up and maybe just kind of move through it.” And so that’s it. Let’s not overcomplicate reaching our financial goals by spending so much focus on those things that we might not be able to control.

I’m going to put up on the screen that first chart that I talked about, which is the red numbers at the bottom are the – it’s normal for there to be declines, intra year declines. And you can see that it’s normal for there to be double digit intra year declines. However, you can see that the vast majority of years are positive and when we add them all up, at least historically, that has been in the favor of the investor and the long-term investor. If you need your money short-term you probably shouldn’t have your money in there anyway because by the time the business cycle, you know, it’s still in the middle of the business cycle you might need your money and so you don’t want to do that. So understand your risk tolerance, understand what your time horizon is and then, of course, a portfolio that fits for you individualized for you.

The second chart that I’m now throwing up on the screen is the benefits of being diversified and also having a long-term horizon. The three columns on the left-hand side are one year so this is going all the way back to 1950. And you can see that in one year there could be a huge variance huge ups and huge downs; you can see that bonds is that middle bar there, ups and downs again; and then a mixture of the two 50/50 in this case of two unmanaged indexes of stocks and bonds. But you can see that when you look out five, ten and 20 years a mixture of them there’s actually never been a five year, ten year or 20 year where you haven’t at least broken even or made a little bit of money in a diversified portfolio. So the future could absolutely be different. However, we’re dealing with probabilities here. We’re trying to do the best that we can as investors and keep our eye on the long-term advantage to you, which is reaching your financial goals possibly passing it onto the next generation income for you, et cetera.

And so I think that that is one of the key ingredients in reaching it, not whether or not the market is at a high or you’re going to wait for it to go down five or ten percent and then buy in. I mean if you’re in this for the long-term you need to make the decision and move forward because the number of times I’ve seen people lose more money trying to avoid the declines is more than they would have lost in the actual decline because they’re sitting here waiting out and the opportunity cost to them about what they would have had, the perfect time to be in is more than what they would’ve had to maybe purchase in at the imperfect time, but then understand that they’re in this for the long-term that it might go down before it goes up.

I continue to be optimistic about 2017. I think that all the ingredients are there when you’re looking at momentum in the market, a very pro business environment, consumer sentiment, lots of money, lots of cash there on the sidelines. I think that if there is a potential tax change, corporate tax change, a repatriation of capital backing into the United States these are all very positive moves that would help us out as investors and people who are trying to invest for the long-term and have a good portfolio. So I’m still continuing to be optimistic understanding that we’ve got to find the portfolio that works for what we want to do, individualize, et cetera. So if you’re my client, of course, I’ve talked with you and we can talk about that some more. If you’re not my client you should be; shame on you. Give me a call or meet with your advisor and find out what might make sense for you. But great first quarter; I think it’s going to continue. The probabilities as I read them things are good, but let’s keep our basic common sense, which is what’s your time horizon, what’s your plan, what’s the mix that’s going to allow you to stick with your plan and of course be diversified and keep your emotions in check and be rational about this thing. Understand those things we can control and those things we can’t.

Anyway, that’s enough for me today. I think I’m rambling on. I’m going to try to be a little bit better on getting these videos out more regularly. Always feel free to give me a call and I’m here at your service. Mike Brady Generosity Wealth Management 303-747-6455. You have an awesome day, awesome weekend. Thanks. Bye bye. See you. Bye bye.

Federal Reserve Chair Janet Yellen recently spoke, and was very blunt about her belief that raising rates later this year is a good thing, and will in fact happen.

I’ve stated before that the markets hate uncertainty, and would rather know a bad thing than not know a good thing.

Crazy, eh?

But, we’ve all been expecting this rate increase and it’s being priced into the markets, at least in my opinion.

That’s a good thing.