“Ego kills knowledge, as knowledge requires learning, and learning requires humility.” -Rolsey

In this video, Mike Brady, founder of Generosity Wealth Management, dives into the profound role humility plays in financial planning, especially as the year comes to a close. Reflecting on decades of experience, Mike emphasizes that “that which seems so very obvious sometimes does not play out the way that we think it will.” With the future inherently unknown, he encourages viewers to stay grounded, avoid emotional decision-making, and focus on long-term goals and risk tolerance. By filtering out the noise and distractions from pundits, politics, and market hype, you can approach your financial journey with clarity and confidence. Watch to discover how humility can guide your decisions and help you prepare for the opportunities and uncertainties of the year ahead.

Trasncript

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive full service financial services firm here in Boulder and Fort Collins, Colorado. But I’ve got clients all over the United States.

Today, I want to talk about humility. I usually discuss this once a year because I think it is so important. When I talk about humility, I’m talking about the future. We don’t know the future–it is inherently unknown.

So one of the big things that I like to watch out for, or when someone, whether it’s a pundit on TV, whether or not it is a newspaper article, or whether or not it’s another person that I’m talking to, is talking with a level of confidence that they shouldn’t have because it’s about the future. Well, we know that this is going to happen. This is absolutely going to happen. From a financial point of view, we’re going to have this recession. This policy is going to be bad. I think that it’s going to be really not good. I know it will be a disaster next year, and we’re going to have all kinds of volatility.

That’s where I start to discount whatever the person says. Because knowing anything about the future is impossible. You might feel very strongly, you might have a high probability, hey, I believe that this is what’s going to happen. But we also have to have the humility that we could be wrong. I’m absolutely certain unless I’m wrong.

And as I look back at my life, I’m 55 years old. Some of the things that I was so certain of turned out not to be true. Some positions that I had 30 years ago, I have changed over the last 30 years. I mean, if I was the same person today at 55 that I was at 25 or at 20, how boring would that be? I would not have grown as a human being or as a person if I hadn’t at least refined certain beliefs or certain things that I hold true, which have changed a little bit.

But the reason why I bring this up is at the end of the year, and especially as we think about politics with our investments, we’ve got to divorce the two. I think that that’s really important. I have been advising clients for over 33 years at this point. It’s remarkable that when one political party gets into the White House, the other party is certain that the next four years are going to be horrible. And the other way around, okay, it’s remarkable. And neither of which turns out to be true. I remember when the big upset, the first time that Trump won over Hillary Clinton, that I heard people talking absolutely with conviction. “Well, you know, it’s obviously going to be very volatile. How are we going to handle all the volatility?” “This is absolutely what’s going to happen.” And if you look back, 2017 was one of the least volatile years we’ve had in the last 10 years. I don’t say that that will be the case going forward. I don’t know since it’s about the future once again, but I use it as an example of let’s have some humility. That which seems so very obvious sometimes does not play out the way that we think it will.

One of the most important things that we should have as investors is to know what our goals are. What is it that we’re trying to shoot for? Meaning, what’s our 5, 10, 20, or what’s our financial goals? What are we trying to do in life? What’s our duration? What’s our time horizon to get there? And what level of risk allows me to get there, but also allows me to stay with it without trying to change it every month or every quarter, or for me to listen to people on the news or read something, et cetera, who are trying to excite my emotions, not necessarily to inform me.

I think that’s really important as well about humility is understanding the objectives of the people who are talking to me so that I can filter it. I’m the. I’m the hearer. I can take all the data in. It doesn’t mean that it’s God’s truth. It doesn’t mean that it’s absolutely going to play out the way whoever it is that’s saying it or writing it says it will. I’ve got to listen and use my own judgment on that, but also gauge them and what their objective is. Are they here to inform me, or are they here to excite me? And I think that, especially in emotional and political environments, we can get ourselves all worked up if we allow ourselves to.

I have recommended that no one make any changes due to the election. I have said this for the first, you know, 10 months, 11 months of the year, and I’m saying this now. We just got done with November. Remarkably, it was the best month of the entire year for the unmanaged stock market index, the S & P 500. And do I think that it would be different if the other candidate had won. No, I don’t. Okay, I’m just going to tell you that right off the bat.

Let’s divorce what our pundits are telling us and what we believe, you know? We have to have some humility. As we go forward from our investments, we stay with our duration, we stay with our plan, we stay with the level of risk that allows us to stay with that plan. And we don’t get distracted by who won this election, and that election–this particular policy or that particular policy.

It is about the future, and it is inherently unknown. And we don’t know the future. And anyone who says they do know it with conviction, discount them.

That’s all I’m saying. Mike Brady. Generosity Wealth Management offices in Boulder and Fort Collins. Always love to hear from you. Hope you have a wonderful December.

At the end of December, beginning of January, I’ll have a more technical outline, rehash of 2024. And as we look into 2025. So have a wonderful, wonderful month.

“Someone’s sitting in the shade today because someone planted a tree a long time ago.” – Warren Buffett

In our latest video, Mike Brady of Generosity Wealth Management discusses the importance of focusing on actionable, forward-thinking strategies in investing rather than getting caught up in the minute-by-minute analysis often seen in the media. With a look back at the previous quarter’s successes and insights into future market potential, Mike emphasizes a practical approach to investment that’s designed to navigate the inherent uncertainties of the financial markets.

Transcript

Hi there! Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered here in Boulder, Colorado. I’m here with my quarter end video and newsletter.

I want to start off with a question that someone gave me this past quarter. They said, “Mike, your videos are not often very technical. Why is that? Is there a thought behind it?” I want to assure you there absolutely is a thought behind it. There are lots of value-based and technical analyses out there every single minute of every day whether you want to read it or you want to watch it on CNBC or Fox Business News. You can watch for an hour or an entire morning and get lots of technical analysis on the cable news. You’re going to be very exact about something that might not really matter. It’s very interesting, but I’m more interested in the aspects in a very short amount of time, which is a lot of our thinking that will make us successful. I will tell you that one of the problems that I have – you’ve heard me say this before that I don’t watch TV news is because it’s 24/7. When we had a half-hour news, maybe in the evening, you have to be concise. What are the most important things? That means you get rid of a lot of superfluous information and talk and opinion. That’s just not the case when you have to be very clear and concise. That’s the approach that I take with the videos as well. What is the most important in a few minutes that I can impart that will be actionable, and that will make a difference? Being completely exact about something that doesn’t really matter isn’t interesting to me. Go ahead and read that in the Wall Street Journal or watch that on some of the specific business ones and you’ll get that. Every once in a while I sprinkle some into my videos but not very often.

Let’s talk about what I think about the last quarter. It was great. By the time you’re watching this video and I’m recording this on Sunday, March 31. By the time you get this video, if you’re my client, you’ve already gotten your statement. You’ll have seen that the unmanaged stock market indexes are positive. The bond indexes, depending on the duration, are either up a little bit or down a little bit – the unmanaged bond indexes. So, pretty flat or, like I said, plus or minus a few on the unmanaged bond indexes.

The real big news is how strong the equity markets have performed. It is very common just about now in the cycle where people say well, it’s obvious that it’s at a high. What do we do when the market is at a high like it is right now? My answer is well, it’s a high compared to what? I mean, it’s a high compared to a year ago, and it’s a high compared to five and ten years ago, but I hope that it’s a low compared to what it’s going to be. To be honest with you, the Dow Jones Industrial Average, which is an unmanaged stock market index, used to be 5,000. Then it was 10,000, then it was 20,000 and then it was 30,000. Now it is almost 40,000, and by the time you watch this video, maybe it will have gone over 40,000. I don’t know – it hasn’t as of Sunday, March 31.

All along the way, when it was at 10,000, I heard people say, “Oh yeah, it’s obviously at a market top. What should we do? Oh, it’s obviously at a top, it’s 20,000.” And then at 30,000. We’ll continue to say this all the way up as it continues to go forward, which I believe that it will. If I didn’t believe that it would, why would I have investments? Why would I have any exposure to any kind of a stock or equity-based investment if I didn’t think that the future was going to be higher than it is today? I don’t know when it’s going to be higher, but why else would I have investments if I didn’t think that the future was brighter than putting it into some kind of a cash or stick it in my mattress or my pillow.

I think that’s a really key concept that we have to remember, and don’t listen to others who might say, “Oh no, now it’s going to go down as we hit the election” or “This is a year that’s going to see all kind of turbulence” and this, that and the other. The future is inherently unknown and we have to keep that humility in mind at all times. That’s what I want to impart on the end of the first quarter. We have three quarters left. We have an election and we have a lot of stuff happening. Hopefully we’ll have some decline and decrease by the Fed on the interest rates.

What I want us to really remember is we have investments for a reason. That’s because the future, we believe, is going to be better than it is right now and we’re going to make profits along the way. If we don’t feel that way you’ve got to give me a call because there’s a mismatch. There is a mismatch in your thinking to what you might be doing, and it’s better to do that proactively now than later. That’s my message for today.

Michael Brady, Generosity Wealth Management, 303-747-6455. You have a wonderful week, a wonderful quarter and don’t listen to 24 hour news. It’s horrible. I hate it. Thank you. Bye-bye.

“Money, like emotions, is something you must control to keep your life on the right track.” ― Natasha Munson

Knowing whether you have an investor or trader mindset is a really important aspect of ensuring that you are satisfied with your financial plan and goals. Discover the fundamental principles that underpin effective investment planning. In the latest GWM video, we explore the importance of setting clear financial goals, understanding risk tolerance, and crafting a well-defined investment strategy tailored to your unique circumstances. Financial growth and security can really only happen when you know yourself fully. Take a watch and let us know what you think!

Transcript

Hi, there. Mike Brady with Generosity Wealth Management, a comprehensive, financial services firm here in Boulder, Colorado.

Today I want to talk about investment management and planning. One of the first questions to start with is are you a trader or are you an investor.

Before I really talk about that and how that flows out into our planning, there’s this great book called A Conflict of Visions by Thomas Stowell, who is this famous economist. He’s now in his 90s, and what he said is when you have a disagreement with somebody whether it’s political, religious, it doesn’t really matter, you’ve got to think of it like a tree. You’ve got a tree. You look at my hands and the root of the tree is here and then branches come out. There are all these decisions – a decision matrix. If you’re disagreeing way up here at the top level, the top leaves you’ve got to go back down the tree, down the limbs to where you might have had a conflict division, where you might disagree. We agreed all the way up to here and now we disagree and that disagreement from a philosophical point of view then has repercussions all the way out here like that.

I think of the same process when it comes to investment management and planning. Are you a trader or are you an investor? Very key. An investor is someone who purchases something, purchases an investment, assumes the investment will be greater in the future and knows that there will be ups and downs along the way, but makes very few changes to that along the way.

A trader, on the other hand, is very actively managing saying wow, I want to buy this stock, that stock, this mutual fund. They want to time the market, they believe that now is the time that the market is going down so I want to move over to cash. Very actively managing it. That is a trader and a trader mindset. A lot of the uncomfortable, the displeasure, in the future is when you say that you’re an investor, you’ve set things up like an investor but then you have a trader mindset. That might be your tendency and your bias.

Once you decide whether you’re a trader or you’re an investor, then you have to decide do I take individual business risk or do I not. That means individual stocks. Do you buy a certain company and be very specific to it or do you buy that broad sector, do you buy the broad market? You could by in the automotive sector and be very heavy in that versus an individual automotive stock. Or do you buy the market as a whole, the S&P 500, the international unmanaged stock market index. It’s really a philosophy of in addition to market risk do you take individual business risk.

That is a very key ingredient and once you’ve decided that, then the question is how do you do that? Do you do that through the various ways like mutual funds? Do you do it through separately managed accounts? Do you do it through ETFs, all of which require a very detailed video to describe some of the pros and cons in each. All of them can be not necessarily good or bad. It’s just a preference. What’s better, a sports car or a truck? Well, neither of them. It depends on what the purpose is. It depends on the individual as well. It’s the same way with your particular investments.

One of the most important decisions as well is are you a believer in mathematics, the CAPM, the Capital Asset Pricing Model, meaning that “hey, I can figure out where the value of this and market is or this particular stock and that’s what it’s either overvalued or undervalued”, or are you more of a behavioral finance person believing that the market is filled with human beings who are emotional and sometimes make irrational decisions. That’s a very key decision to ask yourself and to think about. And of course to talk with your financial advisor to say “hey, what do you think? What’s your philosophy on all of these various aspects?” They are important to craft a portfolio that you’re going to be happy with.

The most important thing is that not that every single day, month, quarter or year is happy for you, but that you’re able to survive it. I think of it like a marriage. When you get married you know that there’s going to be some disagreements and not every single day is going to be sunshine and roses. But, of course, there’s more days that are good than are bad and that you know hey, I can weather this and this is for the long-term good and I’m a better person because I’m mashed up with this other individual in this thing we call marriage. It’s no different with investments. You’ve got to stick with what the plan is that you’ve got and that’s where good investment management comes into play.

Warren Buffett says that bear markets transfers money from the impatient to the patient. Whether you’re a trader or an investor, whether or not you believe in individual business risk or individual market risk or how these things come together. The most important thing is to be patient because even if you’re a trader buying and selling and doing all this other stuff there is a streak that’s going to happen at some point that is not in your favor and you’ve got to weather that as well.

I believe in taking individual market risk but not business risk. I believe in a more passive approach being an investor and not a trader. I believe in many other things that help, but I guide that with my clients.

If you want to talk about investment management and planning and the thought process behind it I’m always happy to talk about my philosophy and how it might work for you. If you’re my existing client or if you’re not how it might fit with your individual situation. Mike Brady, Generosity Wealth Management, 303-747-6455. Thanks.

“The best way to find yourself is to lose yourself in the service of others” — Mahatma Gandhi

As the quarter is now over, it’s a wonderful time to reassess our mindset–do we have an investor mindset or a trader mindset?

An investor understands the long term and is not deterred by short-term events. They do not look for reasons to be pessimistic or instantly act upon a negative reaction.

A trader mindset does that. Short-term events are important, even if you’re invested for the long-term.

This was a tough quarter, and negative. Negative quarters are part of long-term investing, and what investors will experience periodically.

Let’s take a look at what we’ve seen so far in 2022 and compare it to years previous.

Transcript

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered right here in Boulder, Colorado.

I want to take us back to some recent history, just the first quarter of 2020. Covid hit, markets down 20%, 30%, 40% in the unmanaged stock market indexes and everything just looked horrible. At that time I said, “Hey, I think this is an overreaction and an oversold position.” But never in my wildest dreams did I imagine that by the end of 2020, not only had the unmanaged stock market indexes and the unmanaged bond indexes had recovered what they had lost, but they then went into strong positive territory.

So, 2021 which was last year, nice positive territory again. The first quarter of 2022 is negative for the unmanaged stock market and bond indexes. That’s part of the game.

One of the recurring themes that I have in my videos, whether they’re within the quarter or at the end of the quarter like this one is, is that we need to have an investor mindset, not a trader mindset. The difference is an investor understand the long term and is not deterred by short-term events. Does not look for reasons to be pessimistic. Does not say to him or herself, “Okay, it was so obvious,” or, “Oh my gosh, I should have been able to avoid that.” No, that’s a trader mindset. If a quarter of decline is not something that is palatable, then you have either a trader’s mindset or you really should not be in the stock or bond markets at all. It’s just that simple because it will always happen.

If you are an investor anywhere in the U.S. or the world, you have a portfolio that is probably down so far this year. But what history has shown even if it is in correction territory, which is what we have been in, correction territory is negative 10%. I’m recording this on Thursday, March 24, so I don’t know exactly how the quarter has ended. But if it’s around 10% that’s correction. A bear market is 20% negative or greater. If it’s negative 10%, what history has shown is that 75% of the time it’s positive again a year to a year-and-a-half out. And sometimes it’s longer.

When we look at major, major impacts like 2008 and a blended portfolio of 60/40, it took about three years to recover. However, that stands out in memory because it’s so unique when events like 2008 hit. So, 75% of the time going back decades it has recovered within 12 to 18 months. And that’s part of the process of being an investor. Having the temperament to remember that no, we should not have short-term vision. We should not have a short attention span. We need to think about what does this mean for the long term because you don’t invest for the short term, you invest for the long term. You trade for the short term and that’s not what we’re doing. We’re investing for the long term.

As we look to see what this actually means – I’m kind of curious but I’m watching it very closely. What does globalization look like with China and Russia? What does globalization look like with the supply chain breakdown over the last couple of years? Is there more onshore versus offshore? Are we going to bring a lot of that manufacturing, a lot of the being self-sufficient from an energy point of view to our country? Is there going to be more of that with many countries throughout the world than there is now.

We’ve become interdependent which is a good thing in my opinion. It’s better than not being interdependent with others, but this is a shake to the system. The geopolitical events that are happening is reshaping how Europe sees itself and it’s reshaping how the world sees its supply chains and its dependency. Does doing business with someone mean that they won’t invade you? No. The answer is no. We’ve just seen that. Does it mean that you can be a pariah and still invade your neighbors even though you’re part of the global economy? The answer is yes. So, what are the longstanding impacts of this is what I’m always looking at.

When we look at things from a portfolio point of view, from an investment point of view, there is still huge cash reserves by the main companies in the S&P 500 which is an unmanaged stock market index, the Dow, et cetera. The Apples of the world, the big companies have huge cash reserves and this is a good thing. They have seen and weather bad things over the last 10 to 15 years, and the alternatives of cash – just putting your money into a CD – is very unattractive.

So, I continue to be a long-term investor and recommend that for clients. Volatility is something that with experience you become well, experienced. That’s why we call it experience. And so that’s something that you have to live with.

That’s it. Things are going to be down for this first quarter. That’s the way the temperament of an investor has to acknowledge. I love what Warren Buffett says. “In times like this, it transfers money from the impatient to the patient.” Give or take a few billion dollars, he and I we hang out in the same crowds – I kind of wish.

Mike Brady, Generosity Wealth Management, 303-747-6455. Give me a call. Let’s hope the second quarter and third quarter and as things move forward when are we going to break even again? We don’t know, but history has shown that it does break even. Not a long time, but usually in a short time. Thank you. Have a great day.

““It’s good to have money and the things that money can buy, but it’s good, too, to check up once in a while and make sure that you haven’t lost the things that money can’t buy.” —George Lorimer

Each of us has an emotional and a logical side- in investments the emotional side can present biases in our thinking. As we get into the thick of things in terms of elections and leadership, I hear more and more political biases crop up with clients, investors and friends. No matter what side of the aisle they sit, they believe “my” person needs to win for the market to go up, or if “my” person loses it will go down. However the stats all illustrate there is no correlation between that political bias and reality. Let me show you:

Hi there. Mike Brady with Generosity Wealth Management; a comprehensive financial services firm in Boulder Colorado. Today though I’m recording this video from as I call it Generosity Wealth North, which is in Dubois Wyoming. This is where I like to spend a lot of time over the summer. It allows me the opportunity to get away from the hustle and bustle, focus on the business, what are my values, what are my beliefs, what are my core tenants of the business, of who I am as a person, how I interact with clients, all of these various things. And right behind me is the view from the south, so this is actually out of our bedroom, which is our cabin is right behind the camera. You’re going to see this is a ranch, a guest ranch and there’s a, well you probably can’t see it but there’s a little pond over there and our good friends the Prines have been there for five generations. We’ve had this cabin here for, my wife has had it for 45 years; her father got it in the early ‘70s, so almost 50 years.

Let’s get down to business. It’s my belief that we have a logical side and an emotional side in our lives and the way that we approach decisions and so, the problem is when one gets out of whack. So, if we’re all emotion then we’re going to be – I think we all know somebody like that who makes every decision on emotions and they’re just going through life in that regard. We know some other people who are all logic. We’ve got to have a combination of the two and I’m going to expand upon this in a future video; I’m not going to really talk too much about it today. But, it’s important for us to know what our biases are. That’s the emotional side of our investing. I would actually say that the logical side, the mathematics is pretty good from an investing point of view. Not good, it’s the easy part. The hard part is our emotions. We’re human beings.

What I’m hearing right now is a lot of political bias from various clients. And I’ve been doing this for 28 years. As a matter of fact, I got my licenses in August of 1991 so this is exactly my 28thyear of meeting with clients. And what I hear from people on both sides of the aisle, whether Democrats, Republicans, et cetera, is your rooting for your guy, which is fine or your party, you know, your political view, but you’re extrapolating that into what the market is going to do. So, if your guy wins or gal, your person wins, then the market is going to go up or the other person wins then the market is going to go way down. And I’m here to say that historically speaking that has not been the case. I don’t know the future any more than you do so when I look at some percentages I think it’s important for us to acknowledge that it could be different in the future. All we’re saying is what has happened historically.

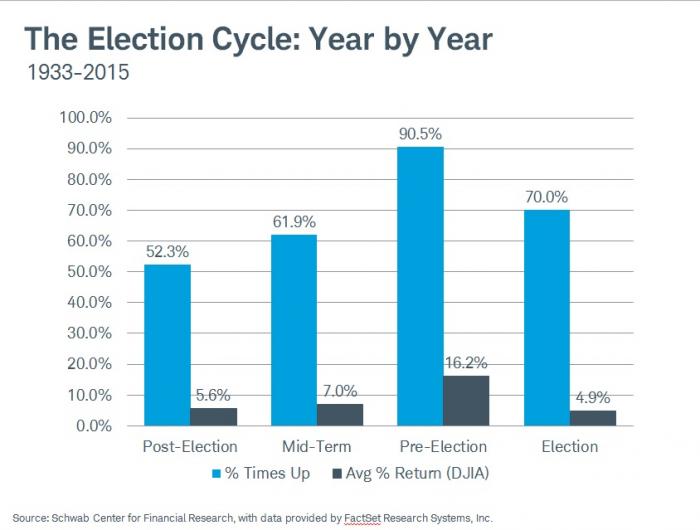

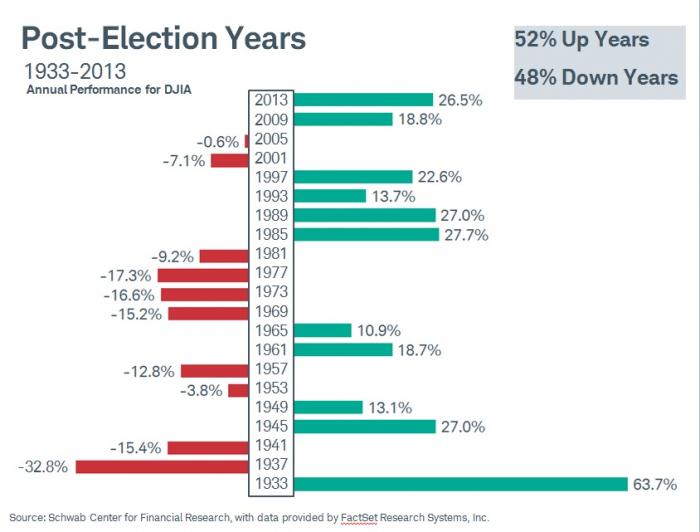

Up on the screen what I’m putting up there is the election cycle years going back 82 years. Historically speaking the worst has been the year after the election and at 52 percent of those years have been positive going back to 1933 all the way up to 2015. And if we were to include 2017 that was actually a positive year. That was the year after the most recent election, but this is the graph that I have. When we go into the pre-election year, which is that second bar graph over the third one over, is 90 percent of the years, I like it, this year have been positive, with an average return of 16 percent, which is pretty remarkable, pretty remarkable when you think about it. The election year, which would be something like next year, 2016, 2012, 2008, et cetera, 70 percent of them have been positive and, of course, 30 percent negative with an average return of about 4.9 percent.

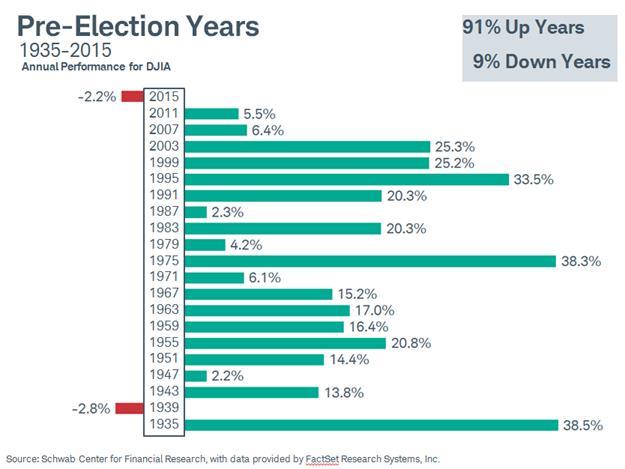

Let’s go over to the next graph that I’ve got on there. What you’ll see is pre-election years, like we are having right now, the worst going back 82 years has been a few percent loss.

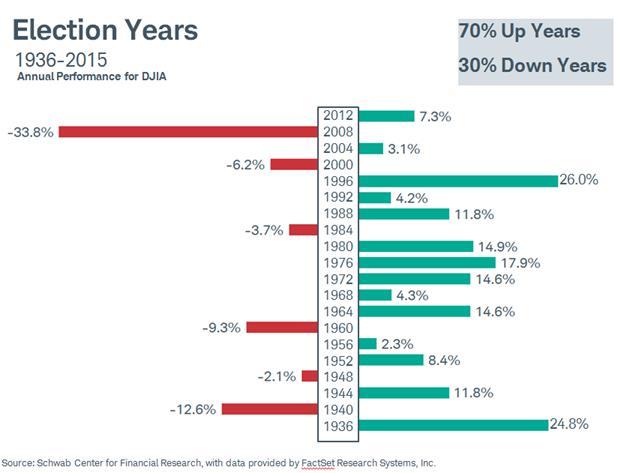

Election years like next year we’re going to see, that’s the next graph on there, the vast majority of them, 70 percent of them have been positive, you can see some have been negative, usually single digits, except for 2008; that was the financial crisis. I would argue that that had very little to do with the political, it just happen to be in an election year cycle. It could have happened in 2007 or 2009, it just happened to happen in 2008. So, the fact that it was an election year or any kind of a stamp on the current president at that point I just don’t believe. I think that the logic, the data is there to say that it was going to happen one way or the other no matter who the president was.

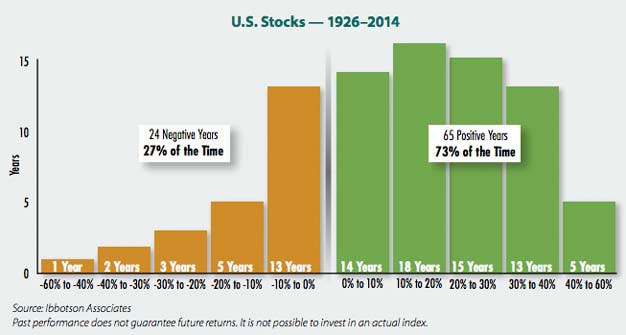

Post-election years is the next graph that I have up there. You’re going to see the majority of them are positive, 52 percent of them. Which when we really look at all of the years together I mean it kind of makes sense that most of the years are positive because you’ve heard me on previous videos that say that three out of four years historically have been positive and so we ought to have that mindset, assuming that we believe in the markets, we believe in the United States and in the world and that this is the best place for our money, why else would you have money in the markets if you didn’t think it was going to go up long-term.

So, I think that it’s important to remember that you can see that from a correlation point of view, whether or not let’s go back to the post-election year whether or not it was a democrat or a republican you can sit here and cherry pick whether or not you think that your guy or gal was the reason for that or your particular party.

It’s just not it.

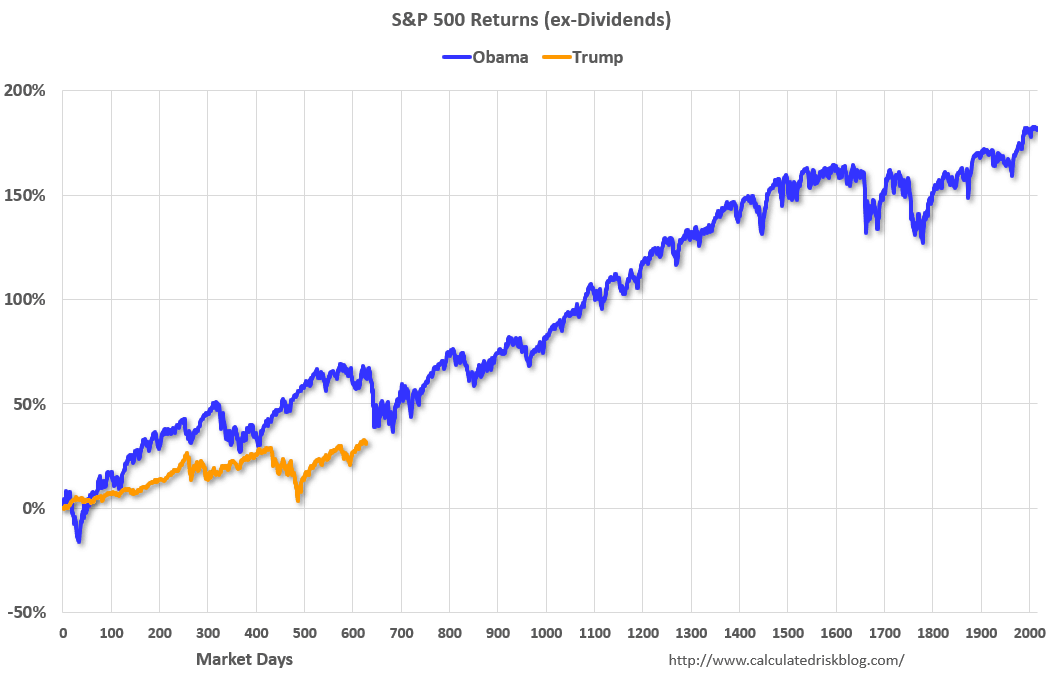

One thing that I hear as well is a lot of people saying well in the last two/three years have been incredible for the stock market, which it has. Hey, listen, it’s been a real good run. I have to say that there were people in 2016 that said if Trump was to win the market is just going to plunge. Well you know what, the exact opposite happened; 2017 was a very non-volatile year and very positive for the markets. 2018 more volatility. 2019 so far this year, very little volatility historically speaking and a very nice positive year. So, we’ve had two of the years so far positive, one year not so good. But here is a graph that I’m putting up on the screen, which will show the top graphic is how many months after the election for Obama. The bottom one is how many months after the election for President Trump. Listen, I don’t want to take away from anything that President Trump has done, but I’m just saying that we have to keep these things in perspective that Obama, from a market point of view, really had a tough time at the beginning of 2009. I would argue not his problem not his fault, that was a continuation of the bad 2008, but then it really kind of rallied through ’09, ’10, ’11, ’12. I mean remember were you there paying attention? I know I was. Nobody wanted to invest in equities. I mean everyone was so negative so negative that was the time to be positive and those that invested in ’09 heavy were the ones who were the big winners.

For Trump over the last couple of years you can see those years it’s been positive. Great. I want to say that that has proven that those people who said it was going to be negative because of him and a volatile person, individual, et cetera, no that’s not true. You can say maybe it was because it was a continuation of Obama. Okay. Whatever. But the fact is that it is positive but it hasn’t been as great as all of those who give all the credit to Trump or those who say no it should have gone negative it actually went positive. What you’re seeing here is a lot of not duplicity, a lot of hey, this is what is going to happen, lack of humility and the opposite happened many, many times, or there’s no correlation. If you’re looking for a pattern, our brains have a tendency to do that, you’ll find a pattern. I’m saying I don’t believe that there’s a pattern and this is how I view the world.

Mike Brady; Generosity Wealth Management; (303) 747-6455. Give me a call anytime or an email. Frankly, you won’t know if I’m there in Boulder or I’m up here in Dubois because I am all electronic up here with no problems. I’m going to end it with a little pan of the rest of the valley. You have a great day.

“Success is nothing more than a few simple disciplines, practiced every day.” – Jim Rohn

Investing and life are more like poker than chess. I recently listened to an interview with Annie Duke. Ms. Duke’s book, Thinking in Bets along with the interview really resonate with me because her thinking is quite similar to mine.

In this quick video, I detail the parallels of investing and poker and why it is critical to keep a “poker face,” keeping your emotional composure during bad….and even good investment periods!

About Thinking in Bets: Making Smarter Decisions When You Don’t Have All the Facts

Annie Duke, a former World Series of Poker champion turned business consultant, draws on examples from business, sports, politics, and (of course) poker to share tools anyone can use to embrace uncertainty and make better decisions.

I like this book for many reasons, the greatest one being the statement, “Even the best decision doesn’t yield the best outcome every time.” In poker, like in investing, you can make the best decisions but there are still unknown elements at play.

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive, full service financial firm headquartered right here in Boulder, Colorado.

Today I want to talk about how investing and life is more like poker than it is chess. I got a lot of these ideas I’m going to share with you today from an interview and a book that I read by Annie Duke. I’m going to put a link in the newsletter and in the transcript of this. (http://a.co/aw2KM5f) Annie Duke, Thinking in Bets.

And when I heard her interview on this podcast it was like she was speaking right to me because that’s the way I think. And so of course I thought she was brilliant. If you watch my videos going back seven, eight, nine years you’ll hear that I talk in well let’s increase our probability of success. And I think the odds are because that’s really the way life and investing is. Let’s think about chess for a second. Chess there’s these pieces on the board and all of them are visible. You see it and so does your opponent. With all that visibility it’s a completely logical game. The person who is the more experienced, the person who is the better player should always win. And if that person doesn’t win then they can go back piece by piece or play by play and say oh, this is where I made a mistake.

That’s not the case with poker. Let’s talk about poker for a bit. You don’t get to see all the cards so there’s a hidden element there. It’s all a bunch of odds. You might have an 85 percent probability, 90 percent. But there’s still 10 percent that you could be wrong. And it doesn’t mean that you were wrong because the outcome went against you. But there were things that you didn’t know. There were unforeseen things and there is luck. I’m not going to ask you to raise your hand but if I was to say who has run a red light, most of us would raise our hand. Even if it’s only once in our life or if it’s once a day. Just because you run a red light doesn’t mean you automatically get hit although it dramatically increases your odds of getting hit. Just like if you’re following the rules and you go through a green light it doesn’t guarantee that you won’t get hit, T-boned by somebody else. So there are factors outside of our control that we have to understand.

When we’re looking at a poker game, a typical poker hand a professional might take two minutes. Therefore, you might have 30 hands in an hour. And a professional poker player is going to know the odds. They have to work really hard to know the odds, play the game, to be cool. Maybe there’s a string of bad luck that you have but you stick to your particular core knowing that you’re a really good player. You know the odds better than the people that you’re playing against and you just can’t get too emotional one way or the other. If you’ve ever seen a poker game nobody’s jumping up and down when they win or at two, three or four hands they’re getting super depressed. Maybe amateurs are but definitely not the professionals.

So investing is very similar. We can do the best that we can with all the different variables that are known to us we can come up with a strategy. We can say wow, I think the market is going to do this, I think the market is going to do that. And we could be wrong because there are going to be things that are unforeseen that are going to be in the future. Nobody knows the future. So that by definition is going to be a variable that we’re not able to account for fully. Therefore, what do we do? What we do is we, of course, look at a diversified portfolio. We say well how can I not stick my neck out so much that if that 10 percent or that 20 percent or whatever the number is that I’m wrong, I’m really stuck that I’ve lost so much. How much are you willing to risk? So a diversified portfolio is very, very important. Staying in it for the long term. If you find your strategy that works with your risk level, your tolerance, that allows you to stay emotionally cool it’s got to be a long term. If you were a poker player it might be many hours. If you are an investor it should be many years. And so you’ve got to keep that in mind as well.

Life is full of unknown variables so we try to increase our knowledge. We try to increase it so we can make the best decisions. We try to learn from those decisions as well. It is not a chess game. It’s not a guarantee. So if you’re looking for a guarantee then investing in life, you know, you’ve come to the wrong place so you’re never going to get that and you’re going to be continually disappointed.

Mike Brady, Generosity Wealth Management, 303-747-6455. You have a great day. Thanks. Bye bye.