I still owe you a video on China, and how I think it’s going to impact things.

It’s tough in that we’ve never had such a large player be so guarded in it’s data.

Economists for now are continuing to be optimistic about China, predicting a positive growth for 2015 even though the markets and their currency have gone haywire.

More to come next few weeks as I complete my analysis and video on China.

“Life is Really Simple–but We Insist on Making it Complicated” – Confucius

Over the next couple of weeks I’m going to talk about the reasons given for the market correction

1. Plunging Oil

2. China

3. Disappointing Profits

4. Trading Milestone (200 Day Moving Average)

5. Rate Jitters

Today I focus on Oil, as it’s declined from approximately $60 in June to $40 today. What is that indicative of, and is that a long term benefit or detriment for the economy?

I say it’s a long term benefit, and make such an argument in my video.

Click below

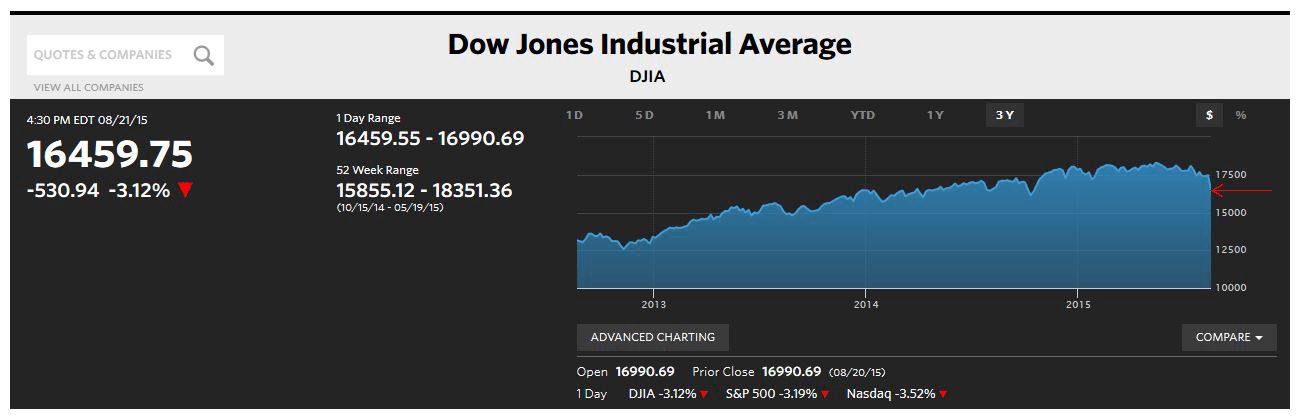

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive full-service firm right here in Boulder Colorado. I’m recording this on Thursday, August 27. Last video I recorded was last Friday. And Monday and Tuesday of this week very exciting; huge plunge in the unmanaged stock market indexes. Wednesday, yesterday from my point of view and so far today we’ve had a nice rebound. So it’s important to remember that even when there’s big ups in the market taking four steps forward, sometimes we take steps back. Well, the opposite is true. When a market is going down sometimes we have nice rebounds. And so I would anticipate, and it is normal for there to be a seesaw, some downs, some ups, et cetera, and so I wouldn’t read too much into a huge decline or too much into a huge advance at this point. I go back to my first video where I talk about, the video from last week, where I talk about what’s your time horizon, what’s your plan and what’s your conviction. I highly recommend you go back and watch that video.

Today I want to talk about some of the reasons being given for the decline in the market. There are five things, I have written them down here that you’ll read about. The first one is plunging oil and that’s what really today’s video is going to be about. Second one is fears about China. We’ve been talking for months and for years about China and so this should not, if you’ve been watching the videos and reading my newsletter, this should not be a surprise to you. Third thing is disappointing profits. The fourth is trading milestones like the 200 day moving average, there’s certain technical indicators. The fourth thing is rate jitters, which is concern about what the Fed might do in September.

Let’s focus just on plunging oil. What the heck does that mean? Back at the end of June oil a barrel was over $60, today is closer to $40. That’s a pretty huge move in just a couple of months. Now it’s good for us to remember that oil is an input into the equation of expenses for a company and for you as an individual. So would we want – so there’s lots of different variables: employee cost, oil, the cost of manufacturing, all your cost of goods sold. And those costs are passed on to the consumer. So it’s good for us to remember that. I mean if there’s an increase in one of those variables, in order for a company to be viable they have to pass on their expenses to the consumer so ultimately you pay for that consumer. Or, when you go to the gas station would you rather pay $30 for a fill up or $40 for a fill up? Of course $30. Now that allows more income to be diverted towards other things. So if I’m now spending $30 where I used to spend $40 for my gas tank, then that gives me $10 to go into the grocery store, to the movie theater or whatever it might be and help my economy in that way or enrich myself or reinvest that extra $10. From a company point of view, the vast majority of companies are helped by a lower cost of that input than are hurt. There are some that are hurt. I’m not going to lie to you. Some of the oil and energy companies are hurt by it, but let’s just look at the unmanaged stock market index, the S&P 500.

The top five sectors are technology, with about 18 percent of that unmanaged stock market index; healthcare of about 16 percent; financial services 15.5; consumer cyclical about 11; and industrials about 11 percent. You add all those things up and 70 percent of the S&P 500 unmanaged stock market index sector wise is non energy related. And it’s not that the other 30 percent is energy related, it’s these are ones that are going to be helped out, the vast majority, the greater good is with oil being at a lower price.

I’m going to throw up on the screen there real quick just oil production. You can see that the U.S. oil production, I put a red arrow next to it, has significantly increased in the last two and a half years. And so what we have with the price of oil is, and one of the reasons why people have concerns about it, is it can be an indicator of the health of the economy. So when the manufacturing is slowing down you demand less oil. And so therefore when you see less oil then that means that the economy is slowing down. That makes sense. However, that’s not the entire equation on the price of oil, it’s price and demand. So if demand is decreased – in this case we’ve had some demand decrease, which is true, but we’ve also had incredible production. So it’s not just the demand, it’s also the galots [ph], the quantity that’s available is significantly greater and increased and so therefore even with the same demand the price would have gone down. The fact that we’ve got some lesser demand just kind of exacerbates the particular problem.

I’m going to throw another chart up there real quick. You’re going to see the economic drag as JP Morgan has done it. You can see that lower price provides less of a headwind against the particular GDP for our particular country. This is a good thing. And so my whole summary of the video is yes some are hurt by lower oil prices and some of the stocks that are tied to that, energy in the S&P 500 unmanaged stock market index and some of the other unmanaged stock market indexes are hurt, or if it’s a part of a diversified portfolio and things of that nature. However, the greater good over the long-term, the one-year and the five-year of having more money that you can reinvest or to repurchase and put into the community is a good thing overall. So I see this as a good thing, not as a bad thing even, though there might be some short-term impacts and that might be one of the five reasons that have been given.

I’ll talk about China, I’ll talk about rate fear] in subsequent videos, I’ll talk about the trading milestones, some of these other things so that you’re well formed over the next couple of weeks. Mike Brady Generosity Wealth Management. 303-747-6455. You have a great day. See you. Bye bye.

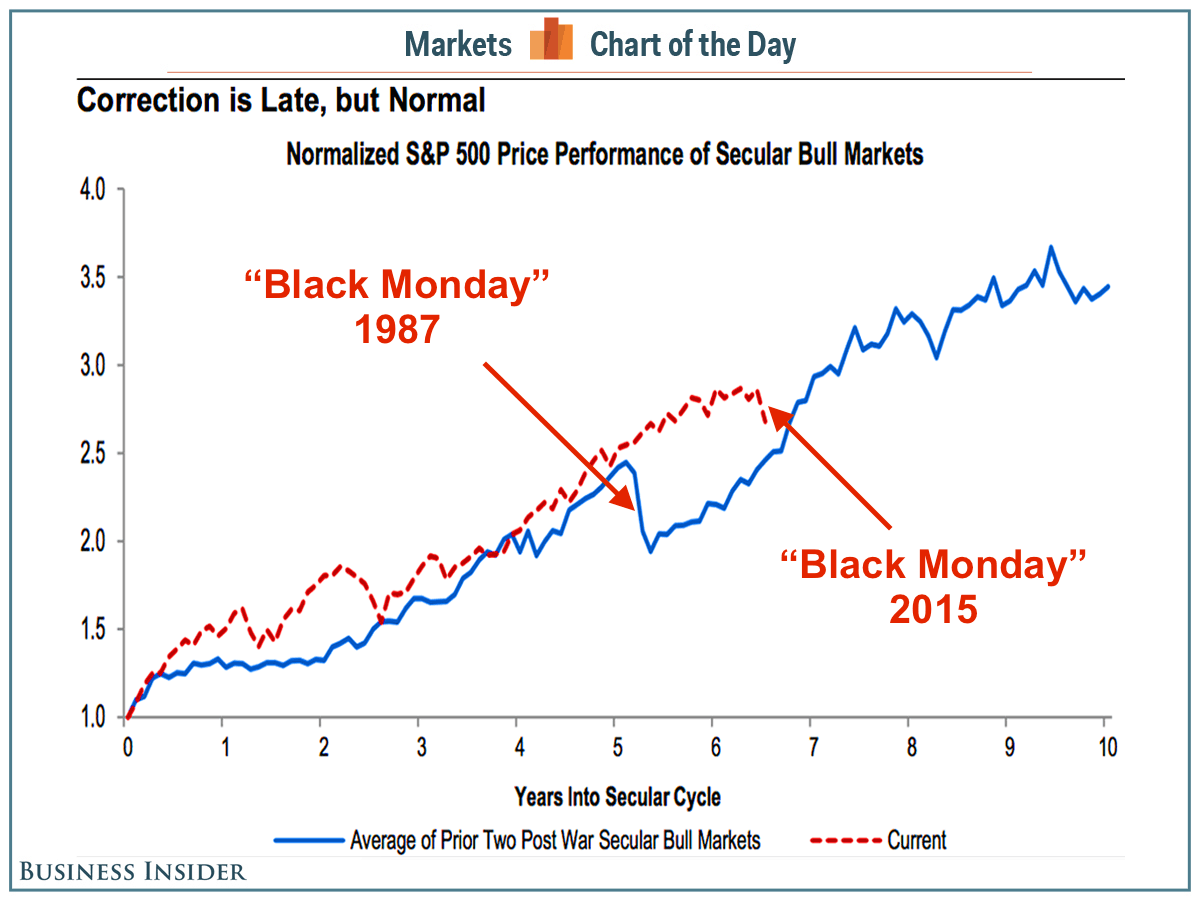

It is normal for there to be corrections with a generally bullish market, which we’ve been in for 6 years now and I believe will continue.

The chart above does NOT mean our RED line will continue, as it could be the end of the bullish trend. I don’t think so, but it’s possible. I’ve made the argument many many times why I’ve come to my conclusion (see previous newsletters and videos going back 2 to 3 years).

We have 4 months left in the year, but more importantly, if you’re invested in the stock market in any way, you should have years in your time horizon

“I never said it’d be easy-I only said it’d be worth it”–Mae West.

That’s what I think about when I think about investments.

Yes, the unmanaged stock market indexes are making the news, but the whole reason we have a plan, discuss the time horizon, and determine our conviction is because these events happen. Always have, and always will.

History has shown us that those who ignore and then over-react are the ones most hurt. I don’t do that, and I wouldn’t want any of my readers to do that either.

For my full thoughts, click below for the video.

Hi there. Mike Brady with Generosity Well Management, a comprehensive full service financial firm headquartered right here in Boulder Colorado. And I am recording this on Sunday after a pretty interesting week in the unmanaged stock market index; it’s like the Dow Jones and the S&P 500. Perhaps you read something about it or saw it on the news. And so the question is should we freak out or how freaked out should we be? And I’m here to tell you step away from the ledge and why I say that. I was recently at a conference. This was a big conference in Washington DC, I just got back last night with probably 1500/1700 people there, big key note speakers, the whole deal. And I know that not everything went according to plan. I noticed that there were a couple problems with the speakers and some other logistical things that happened. And I know the organizer and she was cool as a cucumber. And so I went up and I talked with her. I’m like, “Wow how can you stay so calm when a couple of things really didn’t go the way it was supposed to?” And she said to me I thought very wisely she’s like, “Mike, that’s why I do all the planning in advance. I’m here to execute the plan. That’s why it’s called a plan. Conference organizers who are running around like a chicken with their head cut off are those that haven’t done planning in advance because when a problem happens it’s too late. You already have to have a plan that you can stick to and you just work through it. You just know that nothing is going to go perfectly; there’s going to be some speed bumps and it’s just part of the deal.”

So with that as a lead in, the people who should be concerned are those with a short time horizon. If your short time horizon is six months, 12 months, maybe even 18 months to two years and you’re undiversified and you don’t have a plan and you’re going to need that amount of money, you shouldn’t be investing in the stock market in my opinion. I’ve said this time and time again in all these videos that if you have a short time horizon, and in my mind I think of that as one year, two year or even less, it’s inappropriate because the unmanaged stock market indexes go through ups and downs and sideways and that is too short of a time horizon for there to be a cycle. If you are undiversified, that’s not very smart because individual stocks can take a very long time in order to bounce back, if they bounce back at all. And you should be concerned if you don’t have a plan that includes stocks and bonds of some diversified nature, even though having a diversified portfolio does not guarantee against loss in a generally declining market, if you do not have a plan like that that’s the reason why you have it. Bonds have a tendency to pull things up when stocks go down and the other way around and you’ve got to find a plan that works for you because investor behavior is what hurts most people. That has been my experience in 24 years is that people ignore and then over react. And I certainly don’t do that and I’m here to tell you if you want to be, in my mind, the smart money, you’re not going to do that either.

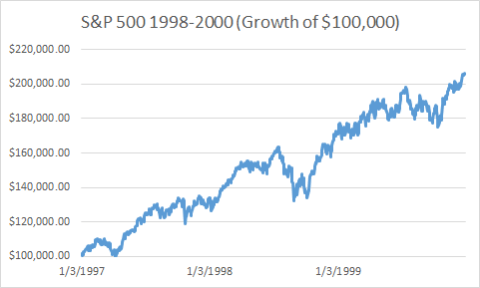

People have a tendency to wait too long to get into the market. Let’s think about ’98, ’99, 2000, my gosh you were a fool if you didn’t get into the Internet stocks because everybody made money there and you can’t lose and how could you be so foolish to be diversified, you need to go all into this. Well, that of course was the wrong time to buy. The market goes down and then people say well this obviously isn’t for me right before the market rebounded back all through the 2000’s. I remember in March of 2009 you couldn’t find somebody who wanted to, it felt like, I couldn’t find somebody someone who wanted to invest in equities and in stocks, when really that was the time that made the most sense. So our emotions cause us to do the wrong thing at the wrong time.

So let’s talk for just a little bit about just 100 percent stock market index. I’m going to put up on the chart there, on the screen, something that I do on almost every single video it seems like. And what you’re going to see the bottom number are the red numbers there, it is normal for there to be declines of even double digits throughout the year. And if you go back and watch everyone of my videos for the last three years I’ve been saying that every time it happens people get all concerned, when in fact that is the norm. The thing that has been unusual is that the last two/three years it has been unusually not on the downside. So what we have seen the last week or two that been so alarming because it happened very quickly over a week or so.

In a future video I’m going to talk about some of the reasons and I’m going to dissect them, but if you’ve got a diversified portfolio, which is what you should have, I’m going to throw another chart up there on the screen. You’re going to see at the far left-hand corner one year and then the second grouping of bars is five years, ten years and 20. The big green bar there is over the last 64 years the high for 100 percent stock market index S&P and the low. And so you can see there’s huge highs and huge lows. But then when you look at the second bar in that grouping is bonds. Bonds have a tendency to not have the high highs and not have the low lows. And when you group them together it has a tendency to bring down the highs and bring up the lows.

When we look to the second grouping, which is a five year time horizon, not one year, not two year, historically a combination of 50-50 stocks and bonds has never had a losing five year time horizon going back 64 years, when in fact, of course, it could in the future. I can’t guarantee what’s going to happen in the next five years, but I do know that historically the odds are in our favor, I believe, that if we have a diversified portfolio that is the way to go.

I’m going to put up on the screen talking a little bit about investor behavior. At the top of the screen you’re going to see, starting in October of 2007 all the way through 2008 and all the way to the decline of 2009, and you’re going to see the top two lines did decline, but they very quickly came back because they were diversified. The bonds have a tendency, and the bottom one by the way was 100 percent stock market index, which you shouldn’t be in anyway for most people. I mean if you can have your investments for a long time multiple and you can handle, you just put it in a shelf and say no matter what I’m not going to lose a minute of sleep, then that might be the answer for you. I don’t know. I’m giving very general thoughts here, but that might be the answer. Most people though get concerned. So that’s why we have to know what our investor behavior is. We want to be the smart money and so therefore we usually include some bonds in there, which has a tendency to buffer some of the downs and unfortunately also buffer some of the up as well. When we look at those lines, I’m going to throw it back up on the screen there, you’re going to see that within pretty quick order, and this is even after that horrible 2008, it came back.

So one thing we have to ask ourselves is what is our conviction? If you don’t believe that two, five, ten, 20 years from now the United States, and that’s where the majority of most investor’s money is, if you don’t believe that the United States is the bet that you want to make, why do you have any money in it? But if on the other hand your time horizon is five years, ten years, 20, and if you say wow I believe that in comparison to the rest of the world we’ve got the best ingredients, we’ve got the best workforce, we’ve got the best in comparison to others or the theory of relativity, I’m throwing in some Einstein for you, then this is part of the deal. We’ve got to stay invested and we stay calm and this is a buying – the world can be really scary if you let it be scary or it can be a world of opportunity if you let it be a world of opportunity. Warren Buffett, and I’ve said this many times, Warren Buffett has said that be greedy when others are fearful, fearful when others are greedy. And people are fearful right now. This is a wonderful opportunity if you believe five and ten years down the road and you’ve got a time horizon that is long. And most people have a long time horizon. If you’re within two or three years of retirement, I have to tell you unless you plan on dying the day after you retire, you got another 20/30 years probably to live even after retirement. If you’re in retirement, you know, you’re in your 70’s your probability of you and your spouse one of the two of you is going to live into your 90’s. That’s just the actuarial reality of it. And so what works for us is our time horizon. We have a plan of stocks and bonds, we have a positive conviction, which I personally do, and we don’t ignore and then overreact. Because frankly your unsophisticated investor has a tendency to wait too long to get in and then get out right at the wrong time and that’s why we have a plan. We think about it in advance so that frankly we’re cool as cucumbers when this happens, we’re not scared by Cramer on CNBC and all of the TV. The best thing for this are the news channels and all the newspapers because people, if you want to see negative you’re going to see negative. If you want to see positive you can see positive. Frankly I try to take both of them. I try to be agnostic, although I have to say my conviction is that I see the positive in there and there’s a buying opportunity from my point of view. I have no idea if one or six months from now the market is going to be higher or lower than it is right now. I believe that it’s going to be equal or greater. I’m not going to lie to you. Not one month perhaps but six months from now, but I could be wrong. I could absolutely be wrong. I could be wrong a year from now.

But you know what, if your time horizon is a year you shouldn’t be in it anyway. So it’s an academic discussion that we’re having right now. That’s why you have stocks and bonds meshed together in a diversified portfolio with a time horizon and with a plan that works for you. There is – I said something about a scary place, just in the last couple of years, I just want to throw out some topics here, remember how scary the Flash Crash, this is just what we saw in the last couple of years, the debt ceiling, the S&P downgrade of the U.S. government, Europe almost collapsed, Greece almost collapsed just last month. The emerging markets is not going to take down the world. That’s my opening. That’s my stake in the sand and I’m going to throw out there. But emerging markets should be a minority of your portfolio anyway. Is it going to affect the U.S. portion of your portfolio? Yeah it could. But even Greece, Greece is incredibly small compared to – I mean they’re a $185 billion GDP, we’re 14, 15 trillion. They’re one percent, less than one percent of us. So there’s always things out there that are scary. That’s why we have the plan in advance.

I’m going to continue with videos throughout, you know, assuming that some headlines happen. I’m going to try to explain; I’m not going to do them super long. This one now as I look at my clock looks like a really long one. I’m going to try to keep them shorter so that they are piffy but that you know that I’m on the job over here watching things on your behalf. (303) 747-6455. Mike Brady Generosity Well Management, give me a call if there’s anything I could do for you. Talk to you later. Bye bye.

Emerging Markets cratered 40%. Commodities fell over 25%. The dollar rallied over 20%. Asia looked like it was falling apart. The US Stock Market fell 18%.

I’m not taking about now, I’m talking about 1998. Right before the US had the best GDP growth rate of the recovery.