For the longest time I’ve counseled against gold as a part of a client’s portfolio.

I’ve heard all the arguments (“it’s a hedge against inflation”, “it lowers the volatility”, it’s real versus paper”), and I discount every one of them.

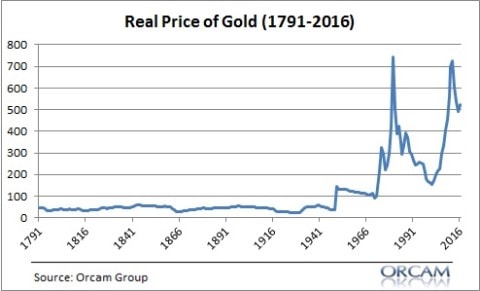

The problem with Gold is that it is unpredictable, and for every instance where it does what you think it should do, I can find an instance where it does the opposite.

Here’s a good blog talking about this more in detail

The last month has been interesting to say the least. This is a wonderful time to ask yourself

Are you an Investor or a Trader?

The mindsets are completely different, leading to different behaviors, and different outcomes.

I ask this question in my video this month, talk about the differences, and let you decide by the end which of the two you are.

So, what do you think? Are you an Investor or a Trader?

Click on the video

Transcript:

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive, full service financial firm here in Boulder, Colorado. Today I’m going to ask the question and by the end of the video hopefully you’ll answer it for yourself. Do you have the mindset of an investor or as a trader? Because they are two different mindsets. An investor is long term, a trader is short term.

Let me talk about a few things in order to help you answer that question. When I talk with people – when the market goes down and I talk with people and perhaps I hear some trepidation, some concern, some worry, I think unconsciously they’re worried about losing everything. Their hard earned savings all gone. They go from having money to nothing. Unconsciously even if they don’t even know it themselves that’s what’s going through their heads.

Let’s talk about some situations on TV or in the newspaper that you’ve heard about where that has happened because that does happen periodically. First off it’s usually a sweet lady or a sweet couple, okay. And they’ve invested everything into maybe a single stock. They’re completely undiversified. And many times that might be something that is exotic. They invested everything in some gold that maybe their brother-in-law or their son-in-law convinced them to buy. Or maybe it went all into one sector like technology or Internet. Or maybe they bought something like coins and then they lost it all and they found out that it was a scam. Many times included in this story is non-liquid. Maybe they bought into a shopping mall and that shopping mall, you know, come to find out is filled with asbestos or something bad and they lost everything. Or it was some kind of a private investment that went belly up. And so I think that these are some of the most common themes when you see people lose it all on TV or when you hear about that.

So therefore let’s talk about that. What are the lessons from it? One, hey if you’re a sweet lady and couple you can stay that. That’s cool okay. But all the others we can avoid, okay. Let’s not go into individual stocks. I am a firm believer in diversification and while we’re in a general decline market diversification does not guarantee against losses, okay. That’s one of the disclaimers we have and it’s true. I’m going to talk about why diversification does make sense.

You shouldn’t go into things that are exotic, okay, in my opinion. Gold and tech and coins and things of that nature. Instead invest in those things that are the market. I talk about the general stock market and the general bond market whatever that mix might be for you specifically in your situation. And I believe that liquidity is very important. And understanding that when you are illiquid if it turns against you you can’t get out of it. And so knowing what your liquidity is and how quickly you can convert to cash if you feel that you’ve erred in our choice of those things.

So one of the other things that I think people do is they feel that the market is linear, okay. And when I mean linear that’s, of course, means a straight line. And it just doesn’t work that way. When a market has gone down five percent it does not mean it’s going to continue to go down another five percent. You can’t annualize. You can’t take a short time and make it a big time. And, of course, the reverse is the same thing. You can’t take well the market went up five percent so therefore it’s going to end in a year at 10 percent of 15. You just can’t do that. Just because it went up doesn’t mean it will continue. Just because it went down doesn’t mean it will continue. As a matter of fact, the market has a tendency and I’m going to show a graph later on to go up and go down. And so therefore if you believe that Point A is here and Point B is here, okay, further out then it’s going to be wavy along the way. And so the higher it goes the sooner it is to a downturn. And the sooner it is when it’s going down the sooner it is to an upswing. So that mentality I think is very, very important.

But let’s pretend like what we’re seeing right now is 2008 again. Let’s pretend like that’s the situation, okay. I’m going to put up on the screen there a graph and I’m going to try to highlight it, make it really big. But if you had invested in the S&P the highest point. You had three different portfolios there, a 60 percent stock and bond or a 40 percent bond and stock or a 100 percent stock market index the S&P 500. You invested spectacularly in October of 2007 at the worst time. And you went through the decline of 2008 which was the worst decline in the S&P 500 going back except for the early 1930s, okay. So it was the absolute worst and definitely in our lifetime, for most of our lifetimes.

And so two year breakeven on a 40-60 split. You know you had absolutely horrible timing or you invested and then you gave some of that up, some of those gains. Two years later you broke even, okay. Okay. I mean if your time horizon is two years you shouldn’t have any investments in my opinion except for cash or extremely short term instruments of some type – CDs, whatever it might be. But even if you’re retiring today or you just retired hopefully your time horizon is many decades. I’m hoping you’re not dying in two years or three years or four years. None of us know of course the future but hopefully we are going to have many many years, okay. And so that is very important.

If you had a 60 percent S&P 500 and a 40 percent bond index your breakeven was three years. I mean that’s on the worst in our time, okay. I’m going to put up on a chart there the time, diversification and volatility of returns. You’ve seen this before if you’ve paid attention to my videos which I certainly hope you have. And so at the first band of bars is one year, second is five years, third is 10 years and then 20, okay. And so the first bar is 100 percent stock market index. The second one is 100 percent bond index and that kind of ugly brown is a split of 50-50 stock and bonds.

So what you’re going to see is going back to 1950 – 1950, okay. That’s 50, 60, 64 years, 65 years, okay. We just finished a year. Sixty-five years of returns a diversified portfolio of stocks and bonds squished together like that. The worst that you’ve done – the worst – not the best, the worst is one percent on average per year. And you can see from that previous chart that sometimes there are years where you’re negative, okay. I mean you are not entitled to positive returns every year when you are invested hoping to get good positive returns over a long time horizon. That is part of the deal. If your time horizon is very short well that might be different. You’ve got to consider why the heck am I in some stocks and bonds if I need this money in a very short amount of time.

As you go out 10 years and 20 years the same, you know, has it normalizing. It continues to go – the absolute worst is making a couple percent a year on average, okay. That’s the worst. And the best is of course much better. This includes that 2008 timeframe. This includes the tech bubble. This includes 1987. This includes the 1970s which were pretty horrible. I was alive in the 70s but I was a young kid. I’m 47 so – almost 47, okay. This week. Send me a birthday card.

So I want to show a graph right there. You see it up on your screen. This is going back to 1926 and this includes the Great Depression. This includes the great recession, okay, of 2008. And what you’re going to see is 73 percent of the time we had positive years. Three out of four, okay. And then when we add in that one bar there of zero to 10 percent this is how the year ended by the way. Almost nine out of ten years are positive. Not 100 percent. You can see on the left hand side one and two years, you know, out of 89 years were the really bad ones that we really, really hate – negative 30 and 40 and 50 and 60. Oh, those are horrible. We hate those. But they’re very infrequent. That’s the point, okay. And even when they do happen, even when they did happen if you had a diversified portfolio then the recovery period was very short. And so these are one of the things that we as investors have to understand.

Going forward it could absolutely be different. Anyone who tells you that they know the future is lying to you and trying to sell you I don’t know – a sack of potatoes or something. And I’m not trying to do that to you. I’m trying to be as realistic as I can understanding that we live in uncharted territory. And by definition the future is uncharted territory. Which is one of the things that I want to talk about. I mean every once in a while someone will say to me yeah, but it’s different. I mean you can’t really say that the 1950s and 60s are the same thing as 2015 or 2016. Yeah, absolutely. I totally get it. And 2008 is not the same as here, okay. Every year is different and every year there is always something whether it’s the downgrade of the government by the S&P, you know. The trip way down. Whether or not it’s a war. Whether nor not it’s the concerns about a war. Whether or not it’s quantitative easing or it’s not or it’s tightening. Every year I could sit here and point out a year and I’ve been doing this for 25 years.

I like to think of it like the presidential election. You know how every four years you hear well this is the most important election of our lifetime. I don’t know. After a while it starts to lose its impact on me because if every four years is the most important of my life, darn, you know, they’re all important. I get it, okay. To say that they’re all the most important and it’s the same thing with an investment, right. You looking at it from a long term point of view and do you believe that Point B, that future, is better than it is today. If the answer is no then that’s your own choice to do then why do you have any investments whatsoever? I mean really why do you have any?

So I believe that every year is different, okay. However, history does have a tendency to repeat itself and that’s what we are working on. And I believe that I’m still very bullish on the markets and I do believe in diversification. Gold, silver, commodities. I don’t like them, never have. Essentially they are very, you know, let me just tell you a little insight. They have a tendency to go up with inflation except when they go opposite, okay. And they really go up when the stock market goes down except when they go down with the stock market too. I mean I hate the correlation. They have a tendency to have a mind of their own and I’m just not – and I don’t think that true investors are going into something that you have no control over like a commodity of gold and silver and things of that nature.

Let’s not forget that the pundits that you see on TV, that you see on any of the cable news or at the end of the day, their job is to get you excited. They’re sort of like when they cover – like a politician. A politician who’s trying to win election is there for hey look at me – bright, shiny light right on me. Their job is to be entertaining and to tell you maybe what you want to hear. Maybe get into your fears and also feed your hopes, okay.

I’m like a policy wonk, okay. I’m sometimes boring. You’re like gosh Mike, you know, why do you have to say that when it’s exciting to get maybe ignore and then overreact. And that’s just not me. I’m here to try to be as upfront and try to be as non-emotional as I can. Still being passionate – hopefully you get that as you listen to me. I have passion for what I do but I want to be non-emotional. And so getting back to my original question an investor is someone who looks at things from a long term point of view, understands that the decisions that you make, your behavior, is probably going to – your behavior and how you react to it or not emotional as you look towards to the long term. You know what? Ups and downs are a part of it. A trader on the other hand is always looking for well what about this and what about that. Always looking for maybe a short cut, maybe a get rich quick scheme. And also worried about these fluctuations that are going to happen. They will always happen and they always have, okay.

And so I want you hopefully to be an investor versus a trader. But if you want to talk about it some more you give me a call. (303) 747-6455. Generositywealth.com. Great to talk with you today. One month, one six months, one year. You know what? When your time horizon is multiple years and hopefully multiple decades it really doesn’t matter. In the whole scheme of things it doesn’t matter. Find something that allows you to stay with your plan. That’s what’s important I think. Anyway, have a great day. We’ll talk to you later. Bye bye.

If all else fails, I guess there’s always buried treasure.

In 1988 a art and antiques’ dealer millionaire was diagnosed with kidney cancer and not expected to live. He planned to take a treasure chest of loot out into the wilderness to die.

Then he recovered.

And decided to bury the treasure instead, and write a memoir with clues to find it.

Very interesting correlation between Chinese and Indian income levels and the price of gold.

Is China and India the reason for Gold’s continued price increase? At least contributing to it if not the cause (remember that correlation does not equate with causation).

I think the demand for gold is a factor, which causes me some slight concern due to the bubble that I think China is. India I’m not sure about yet. If the bubble bursts, the demand for and price of gold will decline.

The stock markets have been making some headlines recently. Last Friday, the DOW declined below 12,000.

Should you freak out? Is this the beginning of the end?

I also address whether I feel the gold rally will continue. Does it make sense to be a part of your portfolio?

TRANSCRIPT:

Hi Clients and Friends, Mike Brady here.

Just a quick video just to let you know what I’m thinking about this week. And this week I’m thinking about, sort of, the news headlines about the kind of, the steady erosion in the Dow and the stock markets, the equity markets, over the last week and a half to two weeks. The momentum has certainly slowed, but is this something you should freak out about, and completely sell all your stocks, and this is the beginning of the end? I don’t believe so. An official correction in the market is when you hit ten percent, and we have not hit that.

As of the recording of this video it’s down about six and a half percent from its high. And you have to ask yourself if this is, you know, completely impacting your portfolio, maybe you have too much in equities and stocks. So this is a good time to evaluate whether or not you are getting the full force of that, the extent of that decline. And if so, then you probably have too much in your in your, too much equities in your portfolio.

I do believe that diversification is a very key ingredient. The last couple of years we’ve had a pretty strong, upwardly mobile market with a couple of declines here and there; and most notably last summer in July. But pretty much it’s been up, up, up. And so something like this makes great news headlines.

I’ve been asked in the past if I think that gold is a good compliment to your portfolio- and the answer is yes. Gold has had a huge rally over the last few years. And one of the reasons why, there’s three reasons why I think it’s going to continue to be attractive and a nice hedge, a nice part (a relatively small part) but a part of your portfolio.

Number one is I think low real interest rates world-wide still make it attractive. I mean, real interest rate means what you are getting after inflation. So if your rate of return is five percent and inflation is four, then your real rate of return is the difference which is one percent.

The second reason why gold is going to be attractive is some fiscal concerns, highlighted in you know, continued fiscal deficits. And so, I think this is something that is a real concern and what makes gold a little bit more attractive.

The third thing is just emerging market economics. It becomes, as emerging markets world-wide, globally, people…, it becomes commodity driven, and people in those areas do want some gold and some inflationary…some protection against inflationary pressures.

I think of, whenever you’re looking at which asset class to go towards, whether or not it’s stocks or bonds or gold, or whatever it might be; it’s like a beauty contest. It’s not always what you think is the most beautiful but you have to think about what everyone else thinks is the most beautiful. And I do think that gold is something that everyone finds very attractive. And so we always have to evaluate do they still think it’s attractive? And we have to be smarter than them about that.

It’s the same way with the momentum of the equity markets, the bond markets, whatever it might be. And so, I think that this summer it is going to be choppy as it relates to the equity and the stock markets. We’ll continue to evaluate that. Do people, getting back to my analogy of the beauty contest, do people still think that it’s attractive? But I think, you know, some of the profitability of the underlying balance sheets of corporations etc., make it attractive to me, and I have to continue to watch to make sure that it’s attractive for other people, to other people, if they are seeing it the same way that I’m seeing it.

So anyway, that’s, those are my thoughts. That’s it for this week. My name is Mike Brady, my company is Generosity Wealth Management. I am a, kind of a holistic comprehensive approach with clients, with their financial well-being. Give me a call, 303.747.6455. I am a registered representative with Cambridge Investment Research. You have a wonderful week and I’ll talk to you next week. Bye bye now.