“By staying calm, you increase your resistance against any kind of storms.” – Mehmet Murat Ildan

Every single year there is some kind of market volatility. It is normal for there to be ups and downs. Therefore, preparing ourselves for it early on is the key. We know it’s going to happen, so we will have a multiple year strategy in mind at all times. And if there are any concerns, of course, you’ll call your favorite financial advisor Mike Brady!

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered right here in Boulder, Colorado.

Last month I did the year end review and it was a little bit longer so this time I thought I would talk shortly about a topic that I know is going to happen in 2020 which is volatility. I’m big into setting up expectations. I’m big into controlling our emotions and having a plan. The reason why I bring that up is in 2020 like every single year there is some kind of volatility. It is normal for there to be drops in the market. There are ups, there are downs.

I’m going to put a chart up on the screen which shows the market going back decades, and you’ll see on the bottom below the axis there are red numbers. Those are the intra-year declines and it is normal for there to be intra-year, within the year, declines in the stock market, the unmanaged stock market indexes, of double digits or more, 10 percent or more.

I’m recording this at the very end of January and, of course, you’ll get it the first part of February and nothing has happened so far this year. However, we have 11 more months. We have an election. We have many different things. We have a global economy that’s very complex. But one thing that I can almost guarantee is that the market will go up and down at various times. And our reaction to it is going to be much more impactful to reaching our financial goals than that actual event of the ups and the downs. That’s my opinion at least.

Therefore, setting ourselves up now and saying okay, great. I know it’s going to happen. I’m going to be cool. I’m going to have my multiple year strategy in my mind at all times. And if I ever have any concerns, of course, I’ll call my favorite financial advisor Mike Brady.

That’s what I want to talk about this year so when it happens don’t be surprised. With the market as high as it is right now, hundreds of points on the unmanaged stock market index, the Dow Jones Industrial Average doesn’t mean as much as it used to frankly, 5, 10 and 20, 30 years ago. We look at the percentages, we know it’s going to happen but we keep the long term vision in mind. What I believe is one of the key ingredients to long term success is keeping our emotions in check, keeping the big picture in mind and really looking at how are we going to reach our financial goals not only with our investments but with all the financial decisions that are going on in our lives.

Mike Brady, Generosity Wealth Management, 303-747-6455. Thanks. Bye bye. Have a wonderful week, a wonderful month. We’ll talk to you in a month. Bye bye.

“Your net worth to the world is usually determined by what remains after your bad habits are subtracted from your good ones.” -Benjamin Franklin

Many folks are worried about market volatility and yield curve. Whether it’s an inherent worry or a byproduct of negative news coverage, it’s helpful to know if it is warranted or not. Some people are excessively worried about airplane crashes, when the greater worry is driving to the airport. But, the first one is dramatic and gets media attention, whereas the second doesn’t.

In this month’s video, I discuss:

Have we had unusual volatility, or has it been unusually calm but it

just seems volatile?

What’s all the hubbub about yield curves? Should I be worried?

Hi there. Mike Brady with Generosity Wealth Management; a comprehensive full service financial services firm headquarters right here in Boulder Colorado. Although you can probably tell by the background that I’m actually at Generosity Wealth Management North, which is up in Wyoming where I do spend some time up at the cabin getting away thinking about the business getting my thoughts in order. Now, the last couple videos I’ve done up here, and you probably have this perception that I’ve been up here the entire summer and it’s just not true. I was in Boulder all of August and all of June and part of July. I just got up here three or four days ago and decided to do the video. I’ll be back in Boulder for the rest all the year and all the way till next June in just a couple of weeks after working up here.

Now, you’re probably wondering why I picked this particular spot in order to record the video. Is it the most beautiful spot? Maybe not. Is it the least windy? Yeah it’s kind of windy up here in Wyoming right now. Is it kind of shady and it’s really sunny out? Yeah it’s shady. But what I’m really proud of is that wood pile right over there that I spent an entire day cutting and stacking. I mean isn’t that a good looking wood pile? I can’t wait to burn it. So, that being said let’s move right on.

The first thing I’d like to talk about is volatility. Someone came up to me two or three weeks ago and said oh my God things have been so volatile it’s just so painful. My answer is has it really been volatile? Up on the screen you’re going to see a graph you’re going to see a bar chart and that is 2019. And on the far right hand corner you’re going to see that the ten year average for plus or minus one percent in movement in one day 72 days in a year. Thirty year average is 86 days. So, 72 to 86 days is the average over a ten or 30 year timeframe for there to be a movement in one day, which means some volatility of one percent or more. In 2017 there were only eight days. I mean it was remarkably smooth. That’s what we got lulled into believing was the normal. 2018 it was a tough year we still were below average at 64 days. And then the number that they have there is only as of June 30 so I pulled my records myself for the unmanaged stock market index S&P 500 and so far this year in 2019, as of September 3rd, which is yesterday, I’m doing this on September 4th, we have 32 days out of 171, which is almost 19 percent, that are plus or minus one percent movement in one day. That means 80 percent of the days are less than a one percent movement, one percent or less. Two percent those are big movements, there’s only been seven days out of 171, which is four percent. Four percent of the days have been two percent or more.

So, I’m repeating myself 80 percent of the days have been relatively low in volatility and we definitely are below the average, both the ten and the 30 year for volatility in a year. So, some things that we believe just aren’t true. We might believe very strongly, we might see it on the news and they pump it up and they get you all excited and that’s not helpful to you. One of the things that I talk about with people is let’s be worried about the right things and this isn’t one of the things to be worried about at this point. So many people are afraid of flying, I mean really their fear should be driving to the airport. That’s significantly more risky statistically than actually being in the plane. Being in the plane is just a more dramatic way to have an accident and there’s no walking away from that.

Now, the yield curve we’ve heard a lot about that in the last two/three/four weeks or so. Am I worried about it? The answer is no. The way a yield curve works is you should have a higher return on your yield on your bonds as time goes by, ten years, 30 years, than you should in the short-term. If that gets reversed where you are actually penalized for holding it for a long time then that’s an inverted yield curve. Yes this has given some indication in the past. The averages are long it’s usually a year or two before there is a recession. My argument would be that that’s not the thing that we need to worry about. The fact that it’s become so common the fact of observing an action sometimes changes that action, it really has to depend on what the Fed does. And so, am I worried that this is going to lead to a recession? The answer is no. Recessions are remarkably, particularly in the last 40 years, infrequent. We had one in ‘73/’75, that’s one, 1980 that was almost 40 years ago, ‘81/’82, early ‘90s, early 2000s, 2007 so that’s six. That’s six of them in 50 years. So, people might say yeah but then we’re due for one. Well, maybe, maybe not. Some of the factors that led to those recessions are not here today and just because it’s been a while since we had the great recession of 2008 that doesn’t mean that we should have one now. It doesn’t have a timer an egg timer. The question is how hot is the economy and how does that relate to the market?

We have had a remarkably, not remarkably, an underperforming, a mediocre is probably the better word, a mediocre recovery since the great recession. And that’s not necessarily bad. I mean if we have a really hot market those things that go really high can come down. It’s like a bright shining star that can burst and fizzle out very quickly. We’ve had a slow burning star for the last 10/11 years and this is a good thing from my point of view. It leads me to believe that it does still have some life. We don’t have high valuations, overly crazy high valuations in the stock market, we haven’t had a lot of the other actions that precede a stock market decline in a recession like people throwing all their money into equities and other things like that so I’m not worried about it.

And the yield curve that’s just one indicator. We joke in our world in the financial services world that economists are always predicting recessions. They’ve predicted nine out of the last three recessions. And so, considering that we’ve had 75 percent, three out of four years are positive, I would rather invest looking towards that than worrying about maybe there’s a recession, which might lead to a stock market decline versus hey I would rather be invested keep this long-term and work on my odds that I believe are in my favor of being in the market long-term. Short-term the recession might happen and if you are in a job that might be recession, the opposite of recession proof capable of being hurt by the recession that’s very sensitive, recession sensitive, then yeah you should worry and make sure that you’re saving a lot in order to whether that particular storm. If you’ve got investments now is a great time, in my opinion, to continue with that strategy going forward.

That’s what I’ve got this particular month. Mike Brady; 303-747-6455. While I’m not always in the office I am always available, email, phone. And one of the things I pride myself on is being particular. Every day is a Saturday and no day is a Saturday as far as I’m concerned because this is what I do and this is what I’m going to do for the next 20 years so I’m very excited about it. To end it here I’m going to take a little pic. There we go. We’ve got that picture right there, which is – can you see that? And we’re going to go around there as well all the way towards our truck. So anyway, you guys have a wonderful, wonderful month and I will talk to you in about a month. Bye bye.

“Being rich is having money; being wealthy is having time.” –Margaret Bonnano

It is important to take a macro versus micro approach to investments, meaning we have to take a very big, long-term view in order to start to make some sense of the stock market. There are many variables in this equation that we call the market and only by looking at it as we would approach a mosaic by looking back months and even multiple years does it start to make sense.

Listen for more on how to keep perspective when looking at the market.

Watch my short video or read the transcript below.

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered right here in Boulder, Colorado.

Today I want to talk about making sense of things. I was meeting with a client a week or two ago and he said Mike, it doesn’t make any sense in the stock market. It’s something that I don’t understand. It goes up high one day and down the next day for a reason that I can’t understand. And my answer to him was stop trying to understand it. Stop trying to understand it on a daily basis, a weekly basis, even a monthly basis because I don’t know the future, you don’t know the future and for us to try to guess the emotions, the intents, the actions of millions of other people is very difficult.

We have to take a very big, long-term view in order to start to make some sense of the stock market. If we’re looking at it from a daily basis, one day if you listen to the newscasters or read some article they always have some reason why it went up like they know definitively what millions of people are thinking. The next day it might completely reverse and then they give a different answer that might be very similar. No, not that many people change from day to day. There are many variables in this equation that we call the market and only by looking at it as we would approach a mosaic by looking back months and even multiple years does it start to make sense.

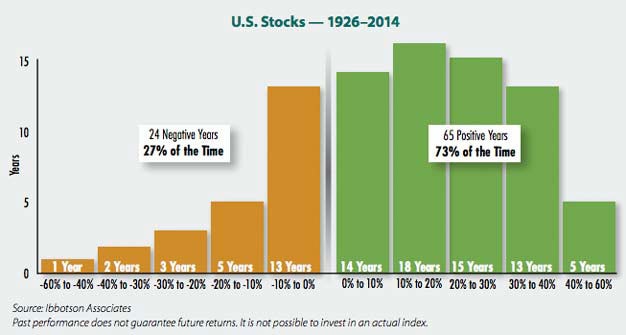

So you have to look at yourself and your own emotions and say wow, am I going to allow myself to be whipsawed from day to day, from week to week, or am I going to take the long-term view. And your bias is very important to know. If you’re a naturally optimistic person I would argue that history has shown you to be a winner in this because three out of four years going back to 1929 the market has been positive. One out of four years have been negative. That doesn’t mean the future is going to be that way. All I can really say is that historically that has been the average when we look at many multiple years, many five-year, ten-year and twenty-year time horizons. Those that are pessimistic and are trying to time the market are worse off than those that say hey listen, I’m going to take a long-term view. On average I am going to be the winner. Sort of like going to a casino and you get to be the house. You don’t get to win every single hand but over time you certainly are the winners.

And so the future is never certain. It could be different in the future but this is what I think would be a better approach for most people.

Mike Brady, Generosity Wealth Management, 303-747-6455. I’m always here if you want to talk. Thank you. Bye bye.

Wealth is the ability to fully experience life. –Henry David Thoreau

2018 is but a distant memory as 2019 has come in fast and furious! In a very short amount of time we wiped away all of 2018’s losses in the unmanaged stock market indexes. This is a quarter that investors and financial advisors dream of, however now more than ever it is time to keep a level head. You hear me say the same thing over and over, and for good reason. Investing is a commitment and in this commitment you need to stay calm.

In the video I discuss humility and bias. Why? Because none of us can predict the future, we do our best to try by watching the news and this forecast and that one, however these media reports consistently report to stretch either negativity or positivity. Middle of the road, even newscasts don’t make headlines, so it’s our job to take everything with a grain of salt.

Watch my short video or read the transcript below and I give a quick breakdown of what we’ve seen so far in 2019.

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive financial services firm headquartered right here in Boulder, Colorado.

First quarter is over of 2019 and it was a banner year. These are the types of quarters that investors and financial advisors, frankly, live for. In a very short amount of time we wiped away all of 2018’s losses in the unmanaged stock market indexes.

Today I want to talk about humility and bias because I think that they’re very important. I mean just three, four, five months ago there was so much things are horrible and the stock market has continued to go down. A lot of pessimism. And then there was lots of optimism in January and February followed by, just three or four weeks ago I was reading an awful lot of pessimism. And the reason why I bring this up is humility. I don’t know the future any more than you know the future and definitely not any more than those that you see on TV or writing those newsletters or those magazine articles. I mean just take it with a grain of salt, okay, because I think that it’s important for us to have a long-term plan, stick with it and not get too deviated by their particular biases.

And so now I want to kind of shift into bias. The bias of those in the media is not to be even-keeled. It is to be sensational either to pump things on the upside and be overly enthusiastic or to be very negative. Just to say oh my god, the world is about to end. Because both of them get headlines. Both of them run the viewership up into record digits. Saying “oh, everything’s all fine. Let’s just do the middle way” doesn’t really fly. And so you’ve got to read or listen to your news that way with that particular filter. I would actually argue that’s a good way to go through life because what is your personal bias? Is your personal bias to be optimistic or to be pessimistic? Right now I’m just telling you that going back to 1929, three out of four years is positive. One out of four has been negative in the unmanaged stock market indexes. So that means if you’re pessimistic you’re really only right one out of four times. Being pessimistic might serve you well if you are in a bad neighborhood, to keep your guard up, to be fearful. But it doesn’t really serve you very well, frankly, in your investments.

So think about it even from a relationship point of view. If you are afraid of being disappointed in friendships is the answer to have no friends? No. The answer is why don’t I look at myself and see if I can moderate my reaction to my disappointments when a friend might disappoint me. That’s the more logical way I would argue in your relationship or friend relationships but also as it relates to investments. Is the better way to be overly optimistic, overly pessimistic or to take your news with a filter but look for the even way? To understand that hey, my bias might be pessimistic but wait a second, is this the real truth?

Recently and before I end today’s newsletter there’s been a lot of talk about the inverted yield curve and I wanted to talk about that for a second. The economy is not the stock market. That’s very important to make that differentiation. The inverted yield curve and we can talk about the difference between the ten year and the two year (maybe I’ll do that in an instructional video next month), but when you see that yes, that has led eventually or at least predicted most of the time to a recession. But it’s been a huge differential between seven months and nineteen months. And during that time as I look back over the last – I’m going to put a graph up there on the screen – there’s been some nice stock markets during that timeframe and some nice times to be invested.

I would argue that since there’s a huge variance there of delay and some false positives that it’s not as good of an indicator as you would be led to believe. But even then it’s an indicator of the economy. The economy is not the stock market. It’s very important to remember that. If you look back at the early 90’s there was an indicator of a recession which did happen. However, does that mean that you shouldn’t have investments? No way. The 90’s were one of the best ten year timeframes ever and I certainly wouldn’t take that as an indicator. The last ten years has been a relatively moderate recovery from the Great Recession when you look at all the underlying GDP numbers versus the averages. However, this last ten years I’m certainly proud that many people invested in the markets and kept their investments over the last ten years. The unmanaged stock market indexes have been very favorable even if the economy was not as ripping and roaring as they have in prior decades.

Anyway, Mike Brady, Generosity Wealth Management, 303-747-6455. Give me a call at any time. Have a wonderful day. Thank you. Bye bye.

“Money is only a tool. It will take you wherever you wish, but it will not

replace you as the driver.” -Ayn Rand

From a horrendous 4th quarter in 2018, to a complete 180 in merely the first month of 2019 it’s still important to keep your sights on the big picture.

It’s easy to be optimistic when the market is going up. It’s harder when the market is going down and all those reporters on TV are giving you all the reasons to be negative. That’s why we have to look at the underlying valuations, the underlying data, the money flow, the money velocity, the corporate earnings to look at what’s the real truth here. What’s the true story?

Watch my video and/or read the transcript. It’s a quick one, under 5 minutes and I continue to illustrate why it’s critical to keep your emotions in check.

Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered right here in Boulder, Colorado. Recording this on Wednesday, January 30. It was right here a month ago that I recorded my year end video and at that time I was talking about what a horrendous December and fourth quarter of 2018 we had. I talked about how 2017 had very little volatility and was strongly up for the unmanaged stock market indexes. In contrast it was followed by 2018 which had all kinds of volatility and was negative with, well the fourth quarter in December really going downward very sharply with huge volatility.

1 Year DJIA

So far in 2019 the month of January has shown another reversal. What great examples that every year is different. I’m going to show you a graph that shows the last 12 months and what you’ll see is so far this year we’ve made back much of what we lost in December and the fourth quarter of last year.

5 Year DJIA

It is important to have a diversified portfolio. It is important to keep the big picture, the long view in mind. Here is a five year graph and you can start to see how one year is not the entire picture. It’s just one piece of the puzzle. And if you only look at the one piece of the puzzle it doesn’t really make sense. Like a mosaic you have to step back and have some perspective for how the pieces, how the years add up toward reaching your 5, 10, 20 year goals.

If you’re older in life you might say wait a second, I don’t have a long view. No, even if you’re retired you don’t want to outlive your money. So whether you’re in the accumulation phase or whether the withdrawal phase of your life with your portfolio having 5, 10 and 20 year points of view is very important.

I believe that there continue to be reasons to be optimistic. It’s easy to be optimistic when the market is going up. It’s harder when the market is going down and all those reporters on TV are giving you all the reasons to be negative. That’s why we have to look at the underlying valuations, the underlying data, the money flow, the money velocity, the corporate earnings to look at what’s the real truth here. What’s the true story?

Let’s say that I am wrong. Let’s say that we continue in the unmanaged stock market indexes to have downward and maybe more volatility as well. That’s the reason why we have diversified portfolios which doesn’t guarantee against losses in declining markets. That’s why we have though a long term view.

So what I would say is let’s get out of our own way. Let’s keep our emotions in check. The mind has a tendency to have a bias toward making patterns where there might not be a bias. We lay on the grass on a nice summer day, look up at the clouds and we’re finding hey, there’s a dog, there’s a building, there’s this famous person right there in the clouds and we are certain that’s what it looks like when, in fact, our mind is creating patterns where there is no pattern. Let’s not do the same thing in other areas of our lives including our portfolios and in the markets.

Mike Brady, Generosity Wealth Management, 303-747-6455. Call me at any time. I’m here to talk about how this is relevant to what you’re doing in your specific financial goals. Here at any time. Thank you. Bye bye.

Up on the screen you’re going to see a graph you’re going to see a bar chart and that is 2019. And on the far right hand corner you’re going to see that the ten year average for plus or minus one percent in movement in one day 72 days in a year. Thirty year average is 86 days. So, 72 to 86 days is the average over a ten or 30 year timeframe for there to be a movement in one day, which means some volatility of one percent or more. In 2017 there were only eight days. I mean it was remarkably smooth. That’s what we got lulled into believing was the normal. 2018 it was a tough year we still were below average at 64 days. And then the number that they have there is only as of June 30 so I pulled my records myself for the unmanaged stock market index S&P 500 and so far this year in 2019, as of September 3rd, which is yesterday, I’m doing this on September 4th, we have 32 days out of 171, which is almost 19 percent, that are plus or minus one percent movement in one day. That means 80 percent of the days are less than a one percent movement, one percent or less. Two percent those are big movements, there’s only been seven days out of 171, which is four percent. Four percent of the days have been two percent or more.

Up on the screen you’re going to see a graph you’re going to see a bar chart and that is 2019. And on the far right hand corner you’re going to see that the ten year average for plus or minus one percent in movement in one day 72 days in a year. Thirty year average is 86 days. So, 72 to 86 days is the average over a ten or 30 year timeframe for there to be a movement in one day, which means some volatility of one percent or more. In 2017 there were only eight days. I mean it was remarkably smooth. That’s what we got lulled into believing was the normal. 2018 it was a tough year we still were below average at 64 days. And then the number that they have there is only as of June 30 so I pulled my records myself for the unmanaged stock market index S&P 500 and so far this year in 2019, as of September 3rd, which is yesterday, I’m doing this on September 4th, we have 32 days out of 171, which is almost 19 percent, that are plus or minus one percent movement in one day. That means 80 percent of the days are less than a one percent movement, one percent or less. Two percent those are big movements, there’s only been seven days out of 171, which is four percent. Four percent of the days have been two percent or more.

burst and fizzle out very quickly. We’ve had a slow burning star for the last 10/11 years and this is a good thing from my point of view. It leads me to believe that it does still have some life. We don’t have high valuations, overly crazy high valuations in the stock market, we haven’t had a lot of the other actions that precede a stock market decline in a recession like people throwing all their money into equities and other things like that so I’m not worried about it.

burst and fizzle out very quickly. We’ve had a slow burning star for the last 10/11 years and this is a good thing from my point of view. It leads me to believe that it does still have some life. We don’t have high valuations, overly crazy high valuations in the stock market, we haven’t had a lot of the other actions that precede a stock market decline in a recession like people throwing all their money into equities and other things like that so I’m not worried about it.