““It’s good to have money and the things that money can buy, but it’s good, too, to check up once in a while and make sure that you haven’t lost the things that money can’t buy.” —George Lorimer

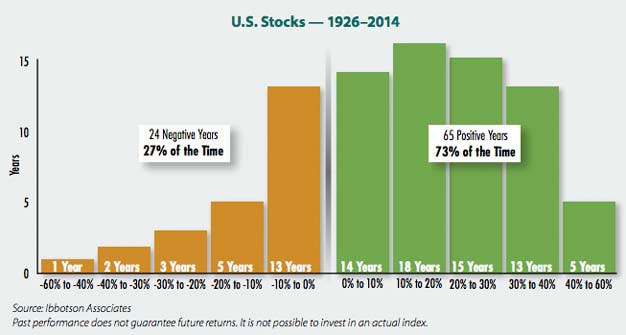

Each of us has an emotional and a logical side- in investments the emotional side can present biases in our thinking. As we get into the thick of things in terms of elections and leadership, I hear more and more political biases crop up with clients, investors and friends. No matter what side of the aisle they sit, they believe “my” person needs to win for the market to go up, or if “my” person loses it will go down. However the stats all illustrate there is no correlation between that political bias and reality. Let me show you:

Hi there. Mike Brady with Generosity Wealth Management; a comprehensive financial services firm in Boulder Colorado. Today though I’m recording this video from as I call it Generosity Wealth North, which is in Dubois Wyoming. This is where I like to spend a lot of time over the summer. It allows me the opportunity to get away from the hustle and bustle, focus on the business, what are my values, what are my beliefs, what are my core tenants of the business, of who I am as a person, how I interact with clients, all of these various things. And right behind me is the view from the south, so this is actually out of our bedroom, which is our cabin is right behind the camera. You’re going to see this is a ranch, a guest ranch and there’s a, well you probably can’t see it but there’s a little pond over there and our good friends the Prines have been there for five generations. We’ve had this cabin here for, my wife has had it for 45 years; her father got it in the early ‘70s, so almost 50 years.

Let’s get down to business. It’s my belief that we have a logical side and an emotional side in our lives and the way that we approach decisions and so, the problem is when one gets out of whack. So, if we’re all emotion then we’re going to be – I think we all know somebody like that who makes every decision on emotions and they’re just going through life in that regard. We know some other people who are all logic. We’ve got to have a combination of the two and I’m going to expand upon this in a future video; I’m not going to really talk too much about it today. But, it’s important for us to know what our biases are. That’s the emotional side of our investing. I would actually say that the logical side, the mathematics is pretty good from an investing point of view. Not good, it’s the easy part. The hard part is our emotions. We’re human beings.

What I’m hearing right now is a lot of political bias from various clients. And I’ve been doing this for 28 years. As a matter of fact, I got my licenses in August of 1991 so this is exactly my 28thyear of meeting with clients. And what I hear from people on both sides of the aisle, whether Democrats, Republicans, et cetera, is your rooting for your guy, which is fine or your party, you know, your political view, but you’re extrapolating that into what the market is going to do. So, if your guy wins or gal, your person wins, then the market is going to go up or the other person wins then the market is going to go way down. And I’m here to say that historically speaking that has not been the case. I don’t know the future any more than you do so when I look at some percentages I think it’s important for us to acknowledge that it could be different in the future. All we’re saying is what has happened historically.

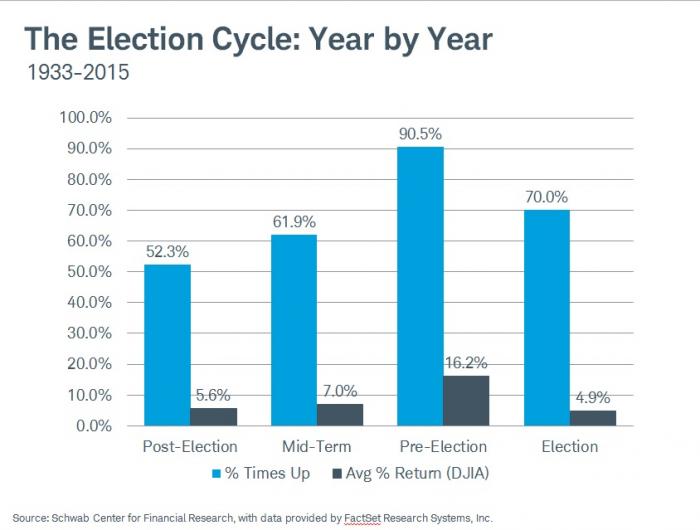

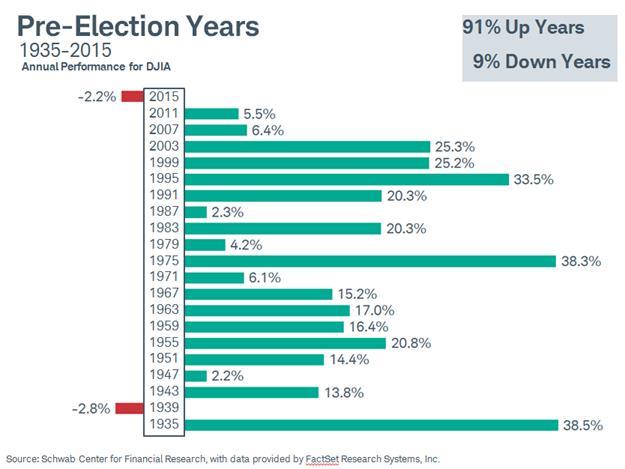

Up on the screen what I’m putting up there is the election cycle years going back 82 years. Historically speaking the worst has been the year after the election and at 52 percent of those years have been positive going back to 1933 all the way up to 2015. And if we were to include 2017 that was actually a positive year. That was the year after the most recent election, but this is the graph that I have. When we go into the pre-election year, which is that second bar graph over the third one over, is 90 percent of the years, I like it, this year have been positive, with an average return of 16 percent, which is pretty remarkable, pretty remarkable when you think about it. The election year, which would be something like next year, 2016, 2012, 2008, et cetera, 70 percent of them have been positive and, of course, 30 percent negative with an average return of about 4.9 percent.

Let’s go over to the next graph that I’ve got on there. What you’ll see is pre-election years, like we are having right now, the worst going back 82 years has been a few percent loss.

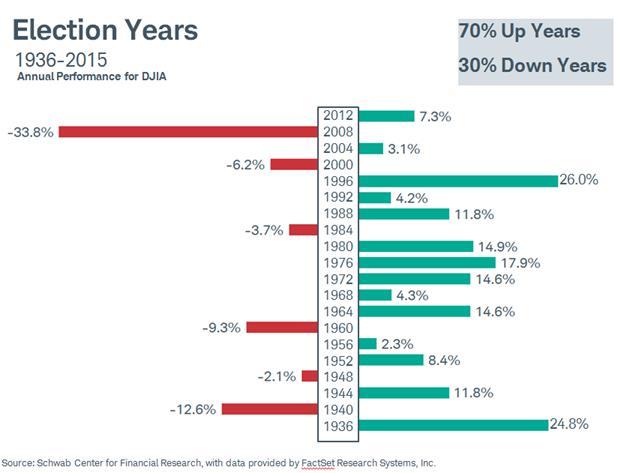

Election years like next year we’re going to see, that’s the next graph on there, the vast majority of them, 70 percent of them have been positive, you can see some have been negative, usually single digits, except for 2008; that was the financial crisis. I would argue that that had very little to do with the political, it just happen to be in an election year cycle. It could have happened in 2007 or 2009, it just happened to happen in 2008. So, the fact that it was an election year or any kind of a stamp on the current president at that point I just don’t believe. I think that the logic, the data is there to say that it was going to happen one way or the other no matter who the president was.

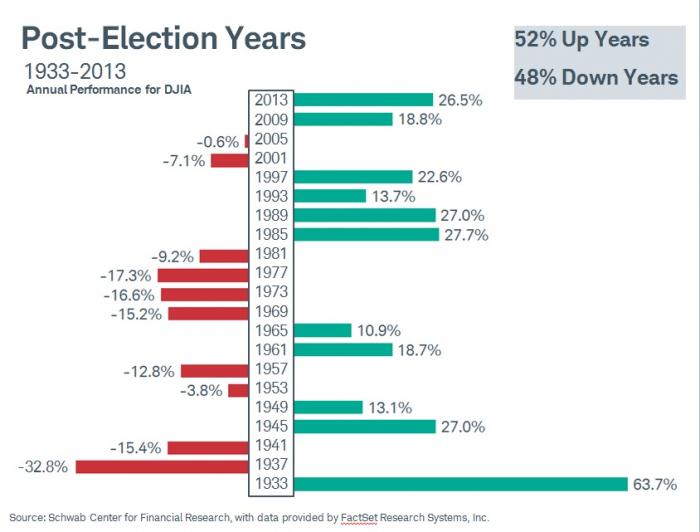

Post-election years is the next graph that I have up there. You’re going to see the majority of them are positive, 52 percent of them. Which when we really look at all of the years together I mean it kind of makes sense that most of the years are positive because you’ve heard me on previous videos that say that three out of four years historically have been positive and so we ought to have that mindset, assuming that we believe in the markets, we believe in the United States and in the world and that this is the best place for our money, why else would you have money in the markets if you didn’t think it was going to go up long-term.

So, I think that it’s important to remember that you can see that from a correlation point of view, whether or not let’s go back to the post-election year whether or not it was a democrat or a republican you can sit here and cherry pick whether or not you think that your guy or gal was the reason for that or your particular party.

It’s just not it.

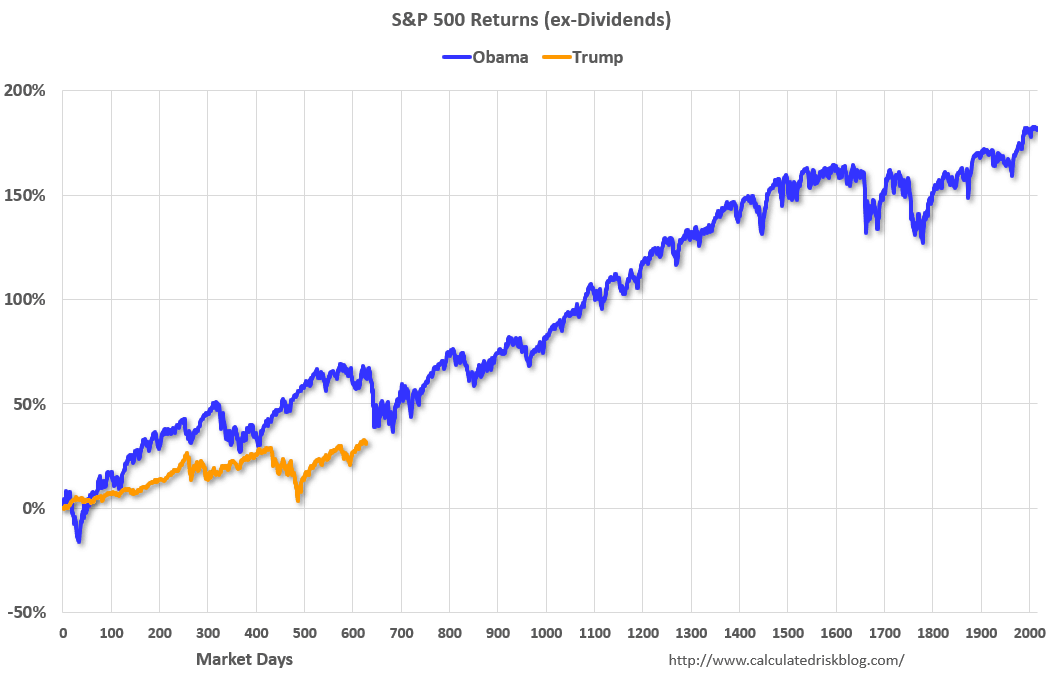

One thing that I hear as well is a lot of people saying well in the last two/three years have been incredible for the stock market, which it has. Hey, listen, it’s been a real good run. I have to say that there were people in 2016 that said if Trump was to win the market is just going to plunge. Well you know what, the exact opposite happened; 2017 was a very non-volatile year and very positive for the markets. 2018 more volatility. 2019 so far this year, very little volatility historically speaking and a very nice positive year. So, we’ve had two of the years so far positive, one year not so good. But here is a graph that I’m putting up on the screen, which will show the top graphic is how many months after the election for Obama. The bottom one is how many months after the election for President Trump. Listen, I don’t want to take away from anything that President Trump has done, but I’m just saying that we have to keep these things in perspective that Obama, from a market point of view, really had a tough time at the beginning of 2009. I would argue not his problem not his fault, that was a continuation of the bad 2008, but then it really kind of rallied through ’09, ’10, ’11, ’12. I mean remember were you there paying attention? I know I was. Nobody wanted to invest in equities. I mean everyone was so negative so negative that was the time to be positive and those that invested in ’09 heavy were the ones who were the big winners.

For Trump over the last couple of years you can see those years it’s been positive. Great. I want to say that that has proven that those people who said it was going to be negative because of him and a volatile person, individual, et cetera, no that’s not true. You can say maybe it was because it was a continuation of Obama. Okay. Whatever. But the fact is that it is positive but it hasn’t been as great as all of those who give all the credit to Trump or those who say no it should have gone negative it actually went positive. What you’re seeing here is a lot of not duplicity, a lot of hey, this is what is going to happen, lack of humility and the opposite happened many, many times, or there’s no correlation. If you’re looking for a pattern, our brains have a tendency to do that, you’ll find a pattern. I’m saying I don’t believe that there’s a pattern and this is how I view the world.

Mike Brady; Generosity Wealth Management; (303) 747-6455. Give me a call anytime or an email. Frankly, you won’t know if I’m there in Boulder or I’m up here in Dubois because I am all electronic up here with no problems. I’m going to end it with a little pan of the rest of the valley. You have a great day.

“It’s the steady, quiet, plodding ones who win in the lifelong race.” – Robert W. Service

The year 2018 is over, and what is most interesting is how different it was from the previous year 2017. This is a good reminder that every year is different, and 2019 will not necessarily follow the negative and volatile 2018.

When I write or say something like that, I inevitably hear from someone who says “yeah, but it’s different this time. Everything has changed because of X, Y, and Z”. In my almost 28 years working with clients, the fundamentals of diversification,time horizon, and complementary financial decisions around your portfolio have remained the same. And no, it’s not different this time. I’ve been hearing that for 28 years.

Watch my video and/or read the transcript. It’s less than 10 minutes, and will give you a good big picture perspective on how I see things.

Hi There. Mike Brady with Generosity Wealth Management; a comprehensive financial services firm headquartered right here in Boulder Colorado. 2018 is behind us. Thank goodness. Forget about it. 2019 let’s hope for a very happy and profitable one. I’m going to put up on the screen the unmanaged stock market index the Dow Jones industrial average, the one that you hear about the most on TV. What you’re going to see is the first quarter was negative, the second and third quarters were positive and that’s where we wished that the year has ended. But then we had the fourth quarter and it took it all away. In particular December very volatile and very negative month right there month of December.

Depending on what stock market index you want to look at you’re looking at the negative five, negative six percent for the year. When you get a little bit more non-common ones like the SMP mid cap, the small cap and you’re looking at the Russell 2000’s you’re looking at the negative double digits, the negative teens, the negative 12, negative14, 15, 16. And when you look at the international markets, whether it’s Europe, whether it’s pacific they were negative double digits as well, the negative teens depending on what particular country and what particular index. Very few places to hide in 2018. When we look over at the bonds the unmanaged bond indexes you’re looking at negative as well, negative single digit, negative one and negative six depending the percent that you’re looking at for that particular area and that’s kind of a unique situation, but with rising interest rates that’s just what happened for 2018.

Let’s think about it though for 2017, 2017 I sat here 12 months ago and talked with you about 2017. At that point what I said is wow this was an incredibly nonvolatile year, I mean pretty much every week every month was positive and it was a banner year, yay 2017, but it’s not real. Go back 12 months ago and watch that video and that’s what I said I’m like this isn’t reality guys, this is a unique situation that very low volatile no volatile year practically was then followed by an extremely volatile year, which is 2018. So we have these two contrasts two extremes right next to each other, which should remind us that every year is different. Every year is different and in 2019 it could be someplace in between. So let’s not extrapolate out and say wow 2018 was negative and really volatile so therefore 2019 is going to be negative and really volatile. It just doesn’t work that way.

There are many variables in the equation that go towards an economy, currency markets, stock markets, bond markets, et cetera, and anyone on TV or who is filling a headline in the newspaper or magazine that says this is the reason why the number one reason or this is the sole reason is fooling themselves and they’re fooling you and don’t listen to it. There are a number of factors in a multiple trillion-dollar economy and world market and it’s simply not as simple as this is the reason. When we are creating a portfolio, when you as an investor are trying to reach your financial goals it is important that we stack the odds in our favor to the degree that we can. Absolutely nothing is guaranteed in this world. I just want to say that. But what we can do is look at history and say how can we stack things in our favor knowing that the future might be different? And I’m going to say that there’s three things that we can do: number one, stay diversified, have the right timeframe and then look at all the things that are around it surrounding all those decisions. Let me break each one of them apart.

Number one, stack in our favor with the timeframes. Talk about that first. On a daily basis the market is going to be up or it’s going to be down. That’s it. That’s a very short timeframe and I don’t know on a day-to-day basis anymore than you do whether the market is going to be up or it’s going to be down. When we look out to a year we zoom out like a mosaic we kind of get a little bit more perspective, we step back from the wall and we look at a year we say okay going back to 60, 70, 80 years of market data three out of four were positive, one out of four were negative and sometimes those negative years were strung together. I mean I remember in my career 2000, 2001 and 2002 were three negative years right next to each other. Now I will tell you that 2004 and 2005 were good years. I know because I was there. But 2000, 2001, 2002 were negative years, but three out of four are positives. So when we look at on a yearly basis we’re starting to stack things in our favor if what has happened historically was to continue in the future.

When we look at five years has there ever been a time horizon were a diversified portfolio, 50 percent of an unmanaged bond index, 50 percent of an unmanaged stock index together has lost money? The answer is no. I’m going to put that chart up on the screen. When we look out five years, ten years, 20 years now historically the odds have been in our favor when we can hit our particular mark. So it’s important for us to remember that the future could be different, I just want to let you know that. Having a diversified portfolio does not guarantee market losses in a declining market. I just want to say that. But we’re looking at the right time horizon for what you’re looking at from a client point of view.

Diversification, I said that that was very important. That is important. When you see on TV people who have lost everything that makes great news; oh my gosh little older lady lost all her money in this particular stock or this particular shopping mall or scheme, et cetera. That’s why it’s important to not invest in one individual stock or just a few stocks or a shopping mall or whatever it might be, they make great spectacular horrible stories that’s why you avoided them. A diversified market, diversified portfolio, even when we look back at 2008 the recovery period was two to three years. That was the absolute worst that we keep talking about the great recession was two to three years. And when I explained just a minute or two ago about the five-year and the ten-year time horizons that’s important to remember. Even in the worst situation when we kept our eye on the big picture reaching our financial goals that’s how we were successful.

The third thing is what are all the decisions around it? It doesn’t matter if the market is up if you haven’t save enough money. It’s that simple. It doesn’t matter if the market is up if you’re withdrawing too much money. It’s that simple. So you’ve got to know what your withdrawal rate is and what your deposits rate is depending on which cycle of life you are in. If you are older 60, 70, 80, listen I’m hoping you still have a long time horizon. Hopefully you have a time horizon of five, ten, 20 years, maybe longer depending on what your age is. Perhaps you’re investing the money for not just yourself but for your heirs, that’s important to remember that the time horizon then becomes a longer time.

So every year is different. I’m not going to sit here and tell you that 2019 is going to be positive or it’s going to be negative, I don’t know. But what I do know is that I’m a believer in the economy, I’m a believer in the United States for one thing, and I’m also a believer in a diversified portfolio for the long-term is going to be a wonderful thing for the vast majority of people, but only you can really decide whether the time horizon that you have and a portfolio that we’ve crafted together or that you’ve crafted with your financial advisor, if you’re not a client of mine you should give me a call, is appropriate because volatility and risk in my mind are two different things. The risk of you not having enough money, you not saving enough or you withdrawing money or not reaching your goals those are risks. A subset of that risk is volatility and volatility is always going to be there, particularly when we’re looking at things from a short-term. Short-term means days, weeks, even months, but when we start to look at longer multiple year strings together, string the years together, the volatility starts to tamper down because then we can get some perspective of how it fits towards the end goal.

Mike Brady; Generosity Wealth Management; 303-747-6455. Give me a call at anytime. Bye bye.

“Life is really simple, but we insist on making it complicated” – Confucius

The first half of the year is over, and the year has been up and down on an almost weekly basis.

There are reasons to be positive, and pessimistic.

In this month’s video, I outline why you should be optimistic, and reasons why you can be concerned. In most areas of life there are pros and cons, but the question is which one wins out on balance.

In this case, and I outline this in my video, the positives outweigh the negatives.

But that being said, the fundamentals of reaching your goals remain the same–diversify, have a long term vision, and keep your emotions in check.

Hi there. Mike Brady with Generosity Wealth Management; a comprehensive full-service financial services firm at headquartered right here in Boulder Colorado, although I’m recording this video from our cabin in Wyoming. Hopefully you had a wonderful 4th of July, maybe you took the whole week off. I came up here for the whole week it’s kind of an annual tradition and it allows need to get some business projects done, but even more importantly to get away from the hustle and bustle of the daily life, get my emotions in check, which is of course one of my big recommendations for my clients and for investor.

I’m going to cut right to the chase of today’s video because it’s going to be a mid year report, but the fundamentals of investing and being successful in my opinion have stayed the same, which is to stay diversified, be long-term and keep your emotions in check. That’s one of the fundamentals and I just think that that’s absolutely important.

Today I do want to talk about what’s happened so far and talk about the reasons for being optimistic or pessimistic for the rest of this year. Nobody knows the future. I certainly don’t so this is my analysis so this is one of the reasons why those three that I brought to you, be diversified, long-term, keep your emotions in check are so very important because when someone says they know absolutely what’s going to happen, the impact of this policy or that policy they know exactly what’s going to happen they’re lying to themselves, they’re lying to you and so I don’t think that anyone is well served by that particular approach. So here so far this year the market was up pretty dramatically in January, continuation of low volatility and good market in 2017 coming into 2018; February and March very difficult. And then the second quarter recovered as some of that, but really was really more in general in the unmanaged stock market indexes and bond indexes basically a flat year so far. Plus or minus a couple percent in my mind is flat.

I’m going to throw a chart up on the screen where you’re going to see is we’re in a consolidation period. The markets go up, down and sideways and so far this year it’s a sideways. It’s always irritating to have; everybody wants the up with no volatility and that’s just not the world that we live in. What we’re seeing right now is a time where patients makes a lot of sense. Those are the people who are rewarded long-term and so remember that as you look at your particular investments and your particular approach.

Now, I’m going to put a number of charts up on the screen and I’m going to talk about some of the reasons to be optimistic, some of the reasons that things could look very good. So let’s go through them. The first one is strong U.S. economy and that’s shown a really above average pace with tax cuts, higher government spending, ultra low unemployment rate, the biggest increase in business investments in years, we’ve had an earnings per share that’s very high and the Fed is normalizing monetary policy, and the last is equity valuations are not as pricey as they were just a couple of years ago. And so this is a good reason to be optimistic and in my opinion, I’m not going to lie to you, the pros outweigh the cons. Here are some of the cons: The price of the oil is back up high in the last year or two; it’s around $75 for a barrel. However, I will also put it into context that it is where it was three years ago and lower where it was four years ago and I don’t remember the stock market being horrible during that time frame. Always up and down that’s just part of the deal, but it is not a travesty. Excessive fiscal stimulus in a full economy could lead to an overheat. Got it. And then the third is the tariffs, which I want to talk about here today.

Tariffs over the last number of administrations they have talked about how the barrier to entry, some of the costs of doing business with other countries is greater than it is here. It’s easier for people to import it into the United States than it is for us to export to other countries. That’s what the tariff discussion is all about. So the discussion is out there, has been out there for a long time, the question is what do you do with it? So one of the reasons why, and I’ll jump to the conclusion on this too, while it’s an irritation it’s a wrench into all of the pros that I just brought up it’s not necessarily a deal killer and the U.S. could actually win on it. Some people say they know absolutely this is horrible for the U.S. or they say it’s absolutely horrible for other countries. The bet that President Trump is making is that others will blink before the U.S. will or before he will. And so one of the reasons why that might be the case is the reliance that other countries that we have had these discussions with and imposed some tariffs on are much more vulnerable than we are. Their stock markets are not doing as well as ours are and their economies are not doing as well as ours. We are the strongest out of all those that we have imposed these tariffs on. Our exports are 12 percent of our economy, whereas in China it’s 20 percent, in Canada it’s 1/3 and in Germany it’s 50 percent. They’re much more reliant on exports to us and to other countries as we are exporting to others. So we only do 12 percent of our economy is based on exports from the United States because we have such a big country, we have such a vibrant interstate commerce from city to city state to state that we are less vulnerable than many other countries.

And so that’s why when I weigh something negative like the tariff discussion and wars against all of the positive it’s the net still going towards the positives than it is on the negative. If you’re only focused on the negative, sorry you’re going to be very disappointed and of course you’re quite dark about that. I on the other hand want to balance both of them and that’s why I’ve come out net on the positive. So I’m optimistic for the rest of this year. I’m not making any changes wholesale in client portfolios, in my discussions with clients, et cetera. Sticking with those particular fundamentals it’s served us well the first half of the year, I think it’s going to serve us well the second half as well. Be diversified long-term, be cool, cool as a cucumber.

Mike Brady; Generosity Wealth Management; 303-747-6455. Give me a call at anytime. Thanks. Bye bye.