“The best way to find yourself is to lose yourself in the service of others” — Mahatma Gandhi

As the quarter is now over, it’s a wonderful time to reassess our mindset–do we have an investor mindset or a trader mindset?

An investor understands the long term and is not deterred by short-term events. They do not look for reasons to be pessimistic or instantly act upon a negative reaction.

A trader mindset does that. Short-term events are important, even if you’re invested for the long-term.

This was a tough quarter, and negative. Negative quarters are part of long-term investing, and what investors will experience periodically.

Let’s take a look at what we’ve seen so far in 2022 and compare it to years previous.

Transcript

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered right here in Boulder, Colorado.

I want to take us back to some recent history, just the first quarter of 2020. Covid hit, markets down 20%, 30%, 40% in the unmanaged stock market indexes and everything just looked horrible. At that time I said, “Hey, I think this is an overreaction and an oversold position.” But never in my wildest dreams did I imagine that by the end of 2020, not only had the unmanaged stock market indexes and the unmanaged bond indexes had recovered what they had lost, but they then went into strong positive territory.

So, 2021 which was last year, nice positive territory again. The first quarter of 2022 is negative for the unmanaged stock market and bond indexes. That’s part of the game.

One of the recurring themes that I have in my videos, whether they’re within the quarter or at the end of the quarter like this one is, is that we need to have an investor mindset, not a trader mindset. The difference is an investor understand the long term and is not deterred by short-term events. Does not look for reasons to be pessimistic. Does not say to him or herself, “Okay, it was so obvious,” or, “Oh my gosh, I should have been able to avoid that.” No, that’s a trader mindset. If a quarter of decline is not something that is palatable, then you have either a trader’s mindset or you really should not be in the stock or bond markets at all. It’s just that simple because it will always happen.

If you are an investor anywhere in the U.S. or the world, you have a portfolio that is probably down so far this year. But what history has shown even if it is in correction territory, which is what we have been in, correction territory is negative 10%. I’m recording this on Thursday, March 24, so I don’t know exactly how the quarter has ended. But if it’s around 10% that’s correction. A bear market is 20% negative or greater. If it’s negative 10%, what history has shown is that 75% of the time it’s positive again a year to a year-and-a-half out. And sometimes it’s longer.

When we look at major, major impacts like 2008 and a blended portfolio of 60/40, it took about three years to recover. However, that stands out in memory because it’s so unique when events like 2008 hit. So, 75% of the time going back decades it has recovered within 12 to 18 months. And that’s part of the process of being an investor. Having the temperament to remember that no, we should not have short-term vision. We should not have a short attention span. We need to think about what does this mean for the long term because you don’t invest for the short term, you invest for the long term. You trade for the short term and that’s not what we’re doing. We’re investing for the long term.

As we look to see what this actually means – I’m kind of curious but I’m watching it very closely. What does globalization look like with China and Russia? What does globalization look like with the supply chain breakdown over the last couple of years? Is there more onshore versus offshore? Are we going to bring a lot of that manufacturing, a lot of the being self-sufficient from an energy point of view to our country? Is there going to be more of that with many countries throughout the world than there is now.

We’ve become interdependent which is a good thing in my opinion. It’s better than not being interdependent with others, but this is a shake to the system. The geopolitical events that are happening is reshaping how Europe sees itself and it’s reshaping how the world sees its supply chains and its dependency. Does doing business with someone mean that they won’t invade you? No. The answer is no. We’ve just seen that. Does it mean that you can be a pariah and still invade your neighbors even though you’re part of the global economy? The answer is yes. So, what are the longstanding impacts of this is what I’m always looking at.

When we look at things from a portfolio point of view, from an investment point of view, there is still huge cash reserves by the main companies in the S&P 500 which is an unmanaged stock market index, the Dow, et cetera. The Apples of the world, the big companies have huge cash reserves and this is a good thing. They have seen and weather bad things over the last 10 to 15 years, and the alternatives of cash – just putting your money into a CD – is very unattractive.

So, I continue to be a long-term investor and recommend that for clients. Volatility is something that with experience you become well, experienced. That’s why we call it experience. And so that’s something that you have to live with.

That’s it. Things are going to be down for this first quarter. That’s the way the temperament of an investor has to acknowledge. I love what Warren Buffett says. “In times like this, it transfers money from the impatient to the patient.” Give or take a few billion dollars, he and I we hang out in the same crowds – I kind of wish.

Mike Brady, Generosity Wealth Management, 303-747-6455. Give me a call. Let’s hope the second quarter and third quarter and as things move forward when are we going to break even again? We don’t know, but history has shown that it does break even. Not a long time, but usually in a short time. Thank you. Have a great day.

“Learn from the ocean; not fearing turbulence, it uses the wind against it to rise instead.” – Matshona Dhliwayo

We invest because we believe the long-term is going to be better than the present. During turbulent times like we’re seeing right now with Russia invading Ukraine, in the midst of a mid-term year we need to remember this strategy.

Short-term events shouldn’t dictate our long-term financial strategy. In this video update, Generosity Wealth Management founder, Mike Brady, reiterates the strategy he recommends to his clients: Time Horizon Long-Term Vision.

Humility, like gratitude, is not so much a technique as it is a way of life.” – Ed Latimore.

New Year, same tried and true financial plan. While your goals may change, having a steady and reliable plan is crucial all year round.

In our latest video, Generosity Wealth founder, Mike Brady, briefly reviews 2021, and talks about the perils of predictions. Instead of a prediction, he offers you his 3 best to-dos and not to-dos for financial planning in 2022.

On the top of the to-dos:

Have some humility

Be disciplined

Concentrate on what you can control

Watch the complete video to see the additional three not-to-dos that serve as a warning of what to avoid.

2021 saw a positive stock market index and even with rising interest rates negatively impacting bonds, the year still had low volatility. While you may be tempted to hang on the words of pundits prognosticating the year ahead, remember that 2022 is an unknown. However, with these practical tips, you can weather any storm.

Transcript

Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered right here in Boulder, Colorado.

2021 is now behind us and 2022 is here already. Let’s call 2021 what it was which is a great year, low volatile for the stock market indexes. Pretty much anyone that you look at across the board it was positive and many of them in the double digits, the teens all the way into the 20s. We’re talking value, growth, international. You name it, it was a good, relatively low volatile year. One thing that was not good in 2021 was with rising interest rates, bonds. One of the reasons why you have bonds in a portfolio is to dampen the volatility, so nobody ever complains about making money quickly and having high highs, but nobody likes losing money on the downside or having low lows. So, when you combine these two things together – bonds and stocks – you combine them together and instead of having volatility like this, the volatility is a little bit, not as much on the high side unfortunately, but also you don’t have it on the low. So, over multiple years it is, in my opinion, a better way to go and you can live with it without the emotionality that comes with, “I’m a genius, it’s so high” to the “I’m a loser, it’s so low.” It allows you to say with your plan which is really what I think it’s all about.

You’re going to hear a lot of pundits whether it’s on the radio, the TV, maybe even in print media, talk about what they think 2022 is going to bring. Oh, the market is going to be up this or it’s going to be down that. I avoid it. I’ve been doing this for 30 years and those guys are always wrong, but yet everybody always asks about the next year and they always give out their opinion, and nobody knows what the future is. I think that there’s lots of reasons to be concerned about inflation and the economy and things of that nature, but what we’re not going to do, at least not what I’m going to do, is change a long-term plan that I have for clients based on short-term events which I’m going to talk about here in just a little bit.

I want to share with you three pearls of wisdom and then three things not to do. Since this is my year-end video, or beginning of the year video, whichever you want to look at it, these are core values to what I think so I would like to impart them with you.

Number one to do – and I’m going to put them up there on the screen – is have some humility. The world is complex. Every time that I think I know absolutely everything, you can be sure I probably don’t. The duality of life is true. You can be happy and sad at the same time. You can have things happen in the market that don’t fit real nicely into a headline. The markets can be up one week and down the next week and neither of them made sense. Why would there be a flip like that? Up, down, up down. No, people’s pessimism and optimism isn’t changing every day, but if you’re a newspaper reporter you’ve got to figure out how to make it to a nice, cute little headline. Avoid simple answers to complex issues, and in the finance world things are complex.

Number two, be disciplined. Think about how you were successful up to now in your life. Was it being overly emotional? Was it allowing your emotions to dictate your logic? Probably not. It was because you had some discipline. You were methodical, you hopefully had control of your emotions. I’m going to encourage people to always do that and to continue what made you successful up until now.

Number three is concentrate on what you can control. There are lots of things in this world that we can’t control, but things that we can control is how much we save, how much we spend, when we decide to retire. Some of the factors that could derail us from our financial plan whether that is mitigating the financial loss that might be from our inability to work or a loss of our spouse. There’s lots of things that we can focus on to help ensure that we reach our financial goals. But let’s also not spend so much time and most of our effort on the things that we can’t control.

Here are three things that I have found over the last 30 years that are not helpful. The first one is short-term data is dictating your long-term actions. That makes no sense. If you’ve got a long-term plan, don’t let short-term data dictate that. That’s not helpful whatsoever. Just because the last couple of weeks or the last couple of months have been up, it doesn’t mean the next couple are going to be up. Or just because the last couple of weeks or the last couple of months have been negative and everything you read on the news or watch on the TV is negative, that doesn’t mean the next two or three months or the next year is going to be negative. It just doesn’t work that way. So, don’t do that.

The next thing is let your emotions be manipulated by the media. Most emotions are through the TV media, maybe some through radio and a little bit less on the print. Don’t do that. If it bleeds, it leads and that is the same thing with finances. I’ve already talked about being disciplined and controlling your emotions and things of that nature. This is a part of it. This is one of the variables to you being successful is don’t let yourself be manipulated by entertainment people who really just want you to keep tuning in. Don’t be that person.

The third thing is don’t have a feeling. You know what, I just have a feeling the market is going to turn. I know more than the market is really what you’re saying. Don’t be that person. I have yet to see that work out. Stay invested, have your long-term plan and don’t mess with it. Find something that works for you that you can stick with, and then stick with it. Don’t listen to your brother-in-law, don’t listen to the TV guy. Stick with what works for you and not always listen to the other people who are not focused on what your financial success looks like.

That’s it for my pearls of wisdom and also things to avoid. This next year I’m very excited. I’ve got a couple of good charities that I’m giving money to in relation to all the people who are having birthdays this year. Every month this year I’m going to have a lottery where I pull a name out of a hat and I will contribute $250 to the charity of their choice. I’m really excited about that and we have a great birthday package in store for 2022.

That being said, I’m here at all times. I love what I do and I want to do this for another 20 years. I just absolutely love it and it doesn’t even feel like work and as long as I’m physically and mentally capable I’m going to be right here.

Mike Brady, Generosity Wealth Management, 303-747-6455. You have a wonderful day, week, month, year. Bye-bye now.

“Perpetual optimism is a force multiplier.” – Colin Powell

It’s important to keep the big picture in mind when looking at your financial investment portfolio performance. The first 6 months of 2021 were good, the last 3 have been pretty much break even and the final 3 months of the year have yet to be determined. While things are positive in the unmanaged stock market index and bonds and zero in the cash/CDs, when we look at the big picture we see that we need to stay the course and remain confident in our long-term plan.

Every year there is a reason for there to be pessimism, if pessimism is what you’re looking for, conversely the same is true for positivity. The future is unknown, however our attitude and resolve doesn’t have to be.

If you have short-term needs to prepare for, of course it’s beneficial to set aside money now. Connect with Generosity Wealth Management founder, Michael Brady today if you have a situation requiring specific assistance.

Transcript

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive, financial services firm headquartered in Boulder, Colorado.

This is the last day, sadly for me up here at my cabin in Wyoming. This has been a magical summer once again. Many of you I’ve had Zoom meetings with and emails and phone calls, so there’s zero interruption in the business, but it certainly does enrich my life, the ability to spend a lot of time up here doing outdoorsy things. If you get me on the phone I’ll tell you all the things that I did this past summer to improve our place. But I also think that it’s great to get away, to get some perspective, to get outside of your bubble, to look at things in a new way. Some things will be different, some will be the same, but I think that it is important to proactively do that with your own thinking.

So, 2021. We’ve got three quarters down. I’m recording this on September 29, which is Wednesday. You’re probably getting this the first week of October, and by the time you get this you probably have your end-of-the-quarter statement if you’re my client.

What we’re going to see so far this year is that nice run-up for six months, and then the last three months has been about a breakeven. The unmanaged stock market indexes are positive, high single digits or low double digits depending on what index you want to look at. Bonds are positive as well in the low single digits. Cash whether that’s CDs or money market, et cetera, frankly almost zero. I was looking at some CD rates and some money market rates for a client a couple of weeks ago as he had an extremely short-term liquidity need, and it was very, very low – almost zero.

I think that it’s really important for us to keep the big picture in mind. You’ve heard this from me over the years. I’m like a broken record, but I believe that is one of the keys going forward, the duration. One of the things you might ask yourself is, are there any short-term needs that you have over the next year or two that you need to prepare for. Because, if so, then we should set that money aside because that’s a short duration need.

Now, if we go back to 1980, what you’re going to see is 31 out of those 41 years were positive for the unmanaged stock market index, the S&P 500. Three out of four years. When we actually go back – I’ve seen another study going back to 1929, same thing. Three out of four years, and in that case I think it was 73 percent were positive. So, this is a good thing. When you flip a coin, 50-50 is tails and 50-50 is heads. And when you do 1,000 of those flips, you should have 500 heads and 500 tails. Some of the distribution of it as you look at it though, they’ll be runs. They’ll be head, head, head, head, head, head, head or tails, tails, tails, tails, tails, tails. The stock market is very similar in that there will be some distributions where some years will be positive, positive, positive, negative, negative, negative. But as we look back 41 years, three out of four of those years are positive.

I’ve been doing this for 30 years since I graduated college in the early 90s, 1991. I was 22 years old, and I’m now 52 years old. During that time I have to tell you that every year inflation’s about to rear its ugly head. Every year the other political party is going to ruin this country. It flips, of course, depending on who’s in power. Every year there’s a reason for there to be pessimism if pessimism is what you’re looking for.

I hear pretty much every year from some people saying I’ve just got a feeling. I’ve got a feeling that we’re about to have a correction. I want to tell you that corrections are normal. Of course, like a broken clock, you’re right twice a day. Yes, there are always corrections. Double-digit declines are actually the normal within a year with some of the unmanaged stock market indexes. However, my experience has been that we forget the times that we thought there was going to be a correction and there wasn’t. The amount of money that would have been lost through the opportunity gain if you move to cash and then the market continues to go up is kind of an abstract loss. Whereas, just staying invested, keeping it for the long term, you can see in the short term that there’s an actual loss there. Hey, I used to have $100,000, now it’s worth $90,000 or $85,000. But over time that’s the reason why we keep the long-term vision in place is that it comes back, and it has historically. The future is always uncertain.

However, you know what. I think that’s the best for you, for your health, for your portfolio, for your peace of mind is not to try to decide exactly when and in and buys and sells and things of that nature. It is to be diversified because different areas of the market also do different things. Last year, 2020, value section of the market didn’t do so well. This year it’s near the top. And fixed income, same thing. So far this year, high yield has been the winner. Last year it was not. Last year it was TIPS, Treasury Inflation Protected Securities.

Even within the stock market, the bond market, different areas of it go in and out of favor year by year. That’s why we have a little bit of all of it because it’s difficult. Only in hindsight is it perfect. In the future, it’s always unknown and you can kill yourself, you can really cause yourself a lot of discomfort by always trying to guess what it is going forward.

I have no huge changes that I would recommend for my clients, for you if you’re not a client. Stay calm. Corrections are normal. We should always be looking at the duration of what our needs are for our cash, and the longer that we can keep it invested, the happier we will probably be. That was true 30 years ago, and it’s true today.

Mike Brady, Generosity Wealth Management, 303-747-6455. You have a wonderful day. Thanks. Bye-bye.

“The individual investor should act consistently as an investor and not as a speculator.”

― Ben Graham

There are so many things to feel optimistic and positive about, and conversely there are so many things to be pessimistic about. Which you focus on is your choice. We are inundated with data and noise about what’s important and while we could run ourselves in circles trying to address each thing, it’s more important to identify the two or three things that will make the biggest impact in our lives and focus on those.

Each Summer I spend the season at my second home in Dubois, Wyoming. With the new location comes a fresh perspective. Finding practices that can help you cut through the noise and focus on identifying your goals and strategies is imperative. While the market is good right now, it’s always uncertain, keeping your sights set on your big picture will help you weather any storm.

In our end of quarter 2 updates we discuss the key points in our current market.

Transcript

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered right here in Boulder, Colorado. Although right now I’m actually at my cabin where I’m privileged to spend the summer just east of Yellowstone, east of the Grand Tetons right next to Shoshone National Forest which is right there. In today’s Zoom world you would think this might be a picture, a backdrop but it’s actually reality. This right here – see that little orange thing – that’s the water well that I had dug about a week ago. See that woodpile. That’s a pretty good looking woodpile. And those mountains back there. That’s the Absaroka Mountains just right outside of the Wind River region in northwest Wyoming. There’s so many things to be optimistic about, so many things to be pessimistic about if you choose. Lots of chaos, lots of data, lots of noise, and I think that it’s important whether you’re running a business like I am, whether or not you’re worried about it for your own personal life for reaching your financial goals that you decide what to focus on. You could sit here and worry about a hundred of them and do a pretty bad job on a hundred, or you could worry about the one or two or three things that are going to have the most impact on what it is that you want. I think it’s important to do that and I do that every summer. What is it that’s the most important thing for the next 12 months and that’s where I am right this second.

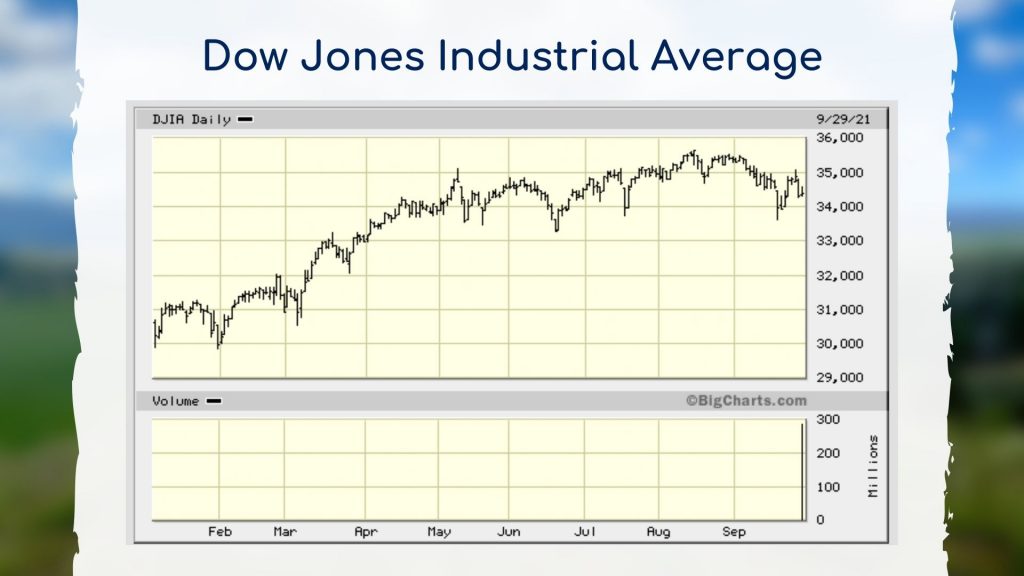

So, this past quarter – another good quarter. Sometimes when I do these videos at the end of a quarter it’s sort of like well, let’s not try to overanalyze this thing. Things are going great and let’s take it when we can. So far this year in 2021 it has been positive, very low on the declines meaning that there’s been basically about three or four steps forward and really only one small little step backward. That’s a really good thing. There’s been very little volatility. With the unmanaged stock market indexes like the Dow and the S&P hitting new highs then when they’d go down by 100 points or 200 points, we used to all freak out. Well now because the Dow is well over 30,000, it’s statistically not as meaningful as it used to be.

So far this year most of the unmanaged stock market indexes are right around almost double digits or into double digits positive which is, once again, just wonderful. Who complains about that.

Bonds give or take. This is broad because there’s so many different types of bonds but in general the bond markets are breakeven to negative. If you’ve got a balanced portfolio with stocks and bonds and some cash and stuff like that, of course you’re not going to be double digits most of the time. If it’s just a broad picture here because the bonds have a tendency to bring that return down when they’re down and they dampen the effects of negative stocks in other years. It’s just kind of give and take. That’s why you have a diversified portfolio for those people where it makes sense to have a diversified portfolio which is pretty much everybody.

Up on the screen I want to put something. There is the weight. On the righthand side there, the top righthand corner I’m going to zoom in on that just a little bit. You’re going to see the weight of the top ten stocks is almost 30 percent. So, when we look at the S&P 500 which is an unmanaged stock market index, the top ten are 30 percent. So if they all went down to zero, the market would go down 30 percent. They have a huge impact on the S&P 500 and that has increased over the last three or four years. I mean we know this. Some of the big technology firms have had a huge impact and so they are having even more of an impact today than they did just two-three years ago.

Now, the same thing with that bottom righthand corner and I’m going to zoom in on that. That’s the top earnings so, of course, their earnings have just been killing it over the last 12 months. I mean COVID was very bad for some small companies in particular and very good for some of the big companies. And we’re seeing it right there. In that chart we’re seeing that in the returns as well of the unmanaged stock market indexes.

This next chart I’m going to put up on the screen is – look at that, way over on the righthand side. I’m going to circle it in red. I said at the beginning of the video that it’s important to keep your eye on what are the major things, the major decisions that you need to make. And one of them – the very best advice that you should have had for yourself or, if you listen to me, that I gave you was hey, listen. These things happen. Stay invested in the market. Stay invested for the long term. You don’t let short-term decisions, data, emotions determine what you’re going to do for the long term.

That right there at the very bottom to where it is right now, that’s what we have to keep in mind. It’s the big picture. Don’t let yourself be persuaded by that pundit on TV or your brother-in-law or whoever it might be who’s whispering in your ear to say, “Oh my gosh. It’s different this time.”

I’m going to show in this next graph that three out of four years, historically at least, have been positive. And that’s what we have to keep in mind is the duration that we have for our investments. If you need the money in the short term you shouldn’t have the money in the markets anyway. It’s not the market’s fault, it’s your improperly placing money in a long-term vehicle, money that you need short term.

I’m going to put up on the screen my third chart and the bottom righthand corner there, if we are so focused on the declines of the market we are not going to have the ups of it. If I am so concerned, as an example, of getting into a car accident that I never get into my car, my life is not as rich. My life is pretty darn local because I never leave my house or it takes me an hour to get from here to the grocery store. So, it is risk mitigation. It is not risk elimination. And so when we look at the bottom you can see that when there’s been a decline in the market, it’s followed by a huge upswing as well. Yes, you’re probably saying to yourself, “Wait a second, Mike. Just the math is if I lose 50 percent, in order to break even I have to make 100 percent.” That’s true from a math point of view. This still shows that when the market goes down, it has rebounded back to breakeven and then some and keeps going. And that’s what we have to keep in mind. The hard thing – and many times in our lives is to do nothing. We want to be industrious. At least we’re doing something. Sometimes the best thing that you can do is to do nothing or to stay with your long-term plan even if your questioning it on a short-term basis.

This next thing I’m going to put up on the screen – you’ve seen me show this before – is going back all the way to 1980. So, that’s 40 years. Forty years of data and three out of four years in general are positive. If you look at the far righthand side you’re going to see that the last ten years have had a lot of positive numbers, but they’ve also had the numbers underneath – the ones in red – are the intra-year declines. Those are within the year a step backward. So, if it went up ten percent and then it went down six percent for the year and maybe it ended positive, it went back up. But that negative four percent from the top, the biggest draw down is that intra-year decline.

You can see there for this year it’s been super low single digits. Very positive. Yes, it went high and then it went back down, it went back up, et cetera. Up and down, seesawing around, but that’s the nature of it. That’s the reason why we can’t look at things like a mosaic. You can’t get too close to your face. You’ve got to have some perspective and that is one of the major things that I emphasize all the time is you’ve got to keep the duration, the big picture in mind and what are the two or three things that are going to make you successful. And one of them, of course, is the big picture in mind. The second is do you have the right duration, the right timeframe for that particular pool of money.

So far this has been a great year. Let’s hope it continues. Now we’re hitting some of the summer months – July, August, September, October. A lot of times historically they’re not as attractive but sometimes they’re good. I mean there’s no absolutes. We don’t want to make a short-term decision here based on we don’t need the money in two or three or four months hopefully, so let’s not necessarily freak out.</p?

I’ll continue to have videos throughout this next quarter, but in the meantime I hope that you’re having a wonderful summer and I hope that you are, like me, that you get to change venues. Change something up in your life so that you see things in an even better way than you did before.

Mike Brady, Generosity Wealth Management, 303-747-6455. You have a wonderful day.

“I find television very educational. Every time someone turns it on, I go in the other room and read a book.” ― Groucho Marx

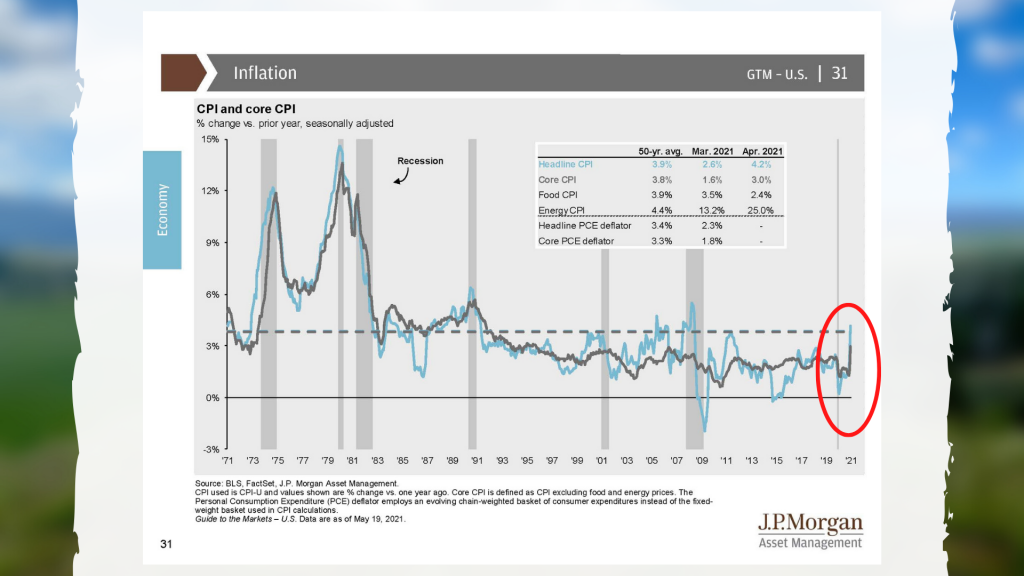

Last month’s inflation was 4.2% year-over-year percentage growth. That’s a large number and if you get your news from the TV news outlets, which we highly recommend you don’t, you are likely up in arms.

The news outlets are there to elicit emotion from you. If you’re going to have a detailed analysis of a complex system like the world economy in two minutes or even five minutes, watching TV news is not going to give you what you need to make an informed decision. Even the news programs on dedicated financial news channels is not where we get our analysis. We always turn to economists that we’ve learned to trust so that we can provide our clients with clear and concise updates.

So, is now the time to panic due to inflation? No, we don’t believe there’s ever a time to panic. But is there a time to be concerned about the impact to you, your life, the economy, your portfolio, things of that nature? Well, that’s not quite the right question to ask. The real question should be, is this temporary or is this systemic?

Watch to hear the answer and a full discussion on inflation.

Transcript

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered right here in Boulder, Colorado. Although I’m hoping that this will be the last video that I do in Boulder for the next four months or so, it’s the end of May. I’m going to head up next week to the cabin and, as you know if you’ve been watching my videos for a long time I can do everything I can do here in Boulder right there from my cabin. It’s 30 minutes outside of a 900-person town overlooking these beautiful mountains and pastures and all that. This next summer I’m very excited because they’re going to put in fiber optics right to my cabin. The whole valley there is getting fiber optics so thank you Rural Electrification Act, whenever that was.

Listen, I want to talk today about inflation. Last month’s inflation was 4.2% year over year percentage growth. That’s a large number and I have to tell you that if you get your news from the TV news outlets, which I highly recommend you not do, you, of course are probably all up in arms. Let me just address something that I said there. It is my belief – just my opinion and you can have a different one – that news outlets are not there to inform you. They are there to elicit emotion from you. If you’re going to have a detailed analysis of a complex system like the world economy in two minutes or even five minutes, watching TV news is not going to give that to you. Even the news programs, the dedicated financial news channels, that’s not where I get my analysis. I get my analysis from economists that I’ve learned to trust – Alex Tabarrok and Tyler Cowen and others and their detailed analysis. They’re usually writing every day great blogs. I post them in my newsletter periodically.

But the question is, is now the time to panic due to inflation? And the answer is no, I don’t believe there’s ever a time to panic. But two, is there a time to be concerned about the impact to you, your life, the economy, your portfolio, things of that nature. So, it’s the wrong question frankly. The real questions are is this temporary or is this systemic? What are all the factors in it? What are the conditions today that might be similar or dissimilar from the last time we had huge inflation which was in the 1970s, and people always go back to. There’s an old adage that every general is fighting the last war. Well, let’s make sure that we’re not fighting the last war against inflation because things were significantly different in the 70s. I mean think about the cars and TVs and microwaves that you had back in the late 70s, or your VHS which was probably a Betamax. I mean things are a little bit different 40 years later. The response and the understanding from an economic point of view about how the economy works has also evolved over that timeframe. It doesn’t mean that we shouldn’t be humble about the future because it’s about the future. Nobody knows exactly what the future holds.

So, let me get back to some of those questions that I’ve thrown out there. Let’s remember that 12 months ago pretty much everything came to a stop. So, the demand for our goods and services came to a screeching halt in general. Now, we’ve got an economy that is almost like a postwar growth economy. The demand for products and services is super high. Is the supply there to meet? No, not necessarily. I mean I was going to finish my deck on my cabin this summer and I can’t because wood has gotten super high. Right now they’re up at my cabin building a new water well and it’s costing me significantly more because of all the metal shortage for the piping that goes down to the aquifer. These are short-term demands that are not being necessarily met by supplies and by the supply chain.

Now, let’s step back for a second. By the way, before I complete that thought, these are short term. When there’s a huge demand there’s other people who come in that will meet that demand whether it is done in one month, one year. But it doesn’t mean that everything is doomed from here on out. At a certain point there is a give and take with supply and demand. There’s never a perfect amount of supply. There’s never a perfect amount of demand. Sometimes they get out of whack and for many core inflation items that’s the situation right now.

So, let’s move on. Is it nominal or is it relative or is it absolute inflation? That’s another thing we have to ask ourselves. If your wages are going up by 5% and inflation is going up 5%, it’s kind of a wash. Or the opposite. If your wages are going up which is what is happening now in order to get service workers in and many workers gets the employment down is wages are going up. If your wages are going up by 8% and inflation is going up by 4% to 5%, you don’t really care. You’re actually relatively wealthier even though inflation is going up as well. And one of the things that has happened over the last 20 to 30 years is we’ve become very addicted to inflation that’s very, very low and has been declining practically down to zero. That’s not necessarily the norm. So, when inflation from one year ago until now goes up, when we’ve become accustomed to a low rate and now there was oh wow, wait a second. Maybe it’s not always low like that. It does come back up. Let’s not extrapolate that out into the everything is horrible and it’s going to continue to extrapolate out in the future.

That’s one of the things that continually surprises me is from a stock market point of view, we know that every year there are going to be, in most years – not every year – but in most years there is a double digit decline within the year. So the market might go up a certain amount and then it usually goes back and forth. Four steps forward, three steps back, et cetera. And when that happens it’s like it’s never happened before. Some people get very excited about it. I’m not sure that helps getting excited about it. Inflation is the same thing. Inflation goes up and it goes down. It doesn’t always go in a straight line.

So, let’s talk about what that really means for the market. So, I’m going to put up one sheet – that far right hand – I’m circling it in red. That is what happened last month. That is over the last 50 years or so you can see that what I just circled is what happened. It went over 4%. It’s 4.2%. These things happen. The last time that happened was 2007 right before it declined. There’s some huge fluctuations there but one month does not make a trend. So, let’s remember that and we have a datapoint of one. Let’s not blow it out of proportion.

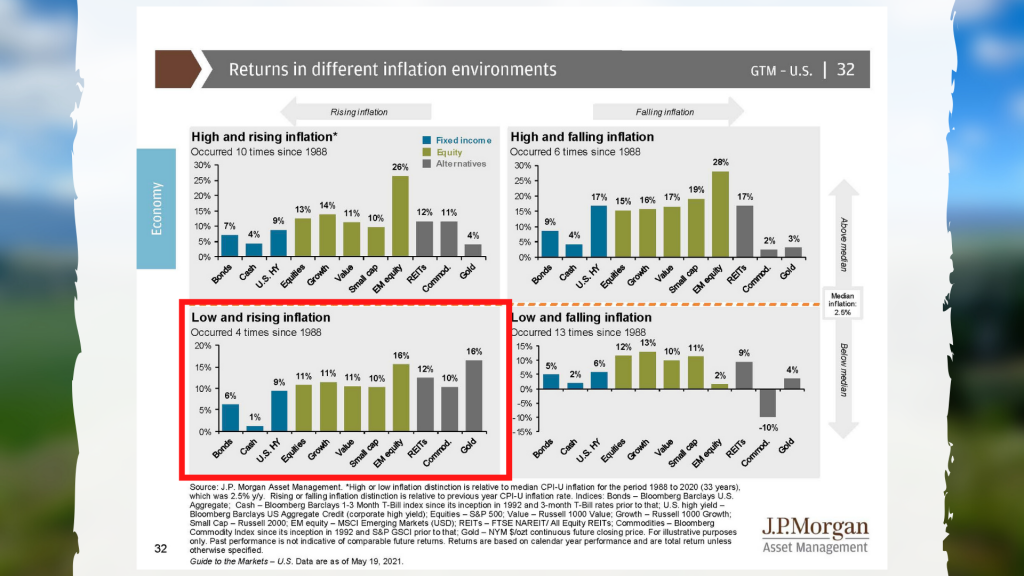

So, what happens? There’s this perception that when the inflation goes up, therefore the stock market is going to go down. That’s not true. Here I have just highlighted that bottom left quadrant and this is when we have low inflation and inflation is rising. What has happened? On average since 1988 – so that’s the last 30 years or so – the four times that has happened the market has increased over the next 12 months. That’s not a guarantee. This next time it could be different. We’re talking about the future here. But if there’s some knee jerk that inflation goes up and stock market goes down, that’s just not the case.

You’ve heard me before talk about duration and how important that is. As a matter of fact, the longer I am in this industry and the longer I work with clients and with money and financial planning, yada, yada, is the more important I believe the duration is which means hey listen, if you’re going to ask for a guarantee from me that the market won’t go down over the next month or two I couldn’t give you that. I could never give you a guarantee anyway. However, when we look out one year, two years, five years, ten years – which is what we should do – inflation has not been the deciding factor of whether or not you’re successful or not. If you need the money in a month or two or even six months you shouldn’t have that amount of money – you should have it in money market or in cash ready and not invest it however we’ve got our stuff for a longer term.

One of the things in the 1970s that’s different from today is it was stagflation, remember. A stagnant economy with inflation and high unemployment and all these things. We have low unemployment that’s decreasing. We have an economy that is growing, not stagnating. But yes, we have one month, one datapoint of inflation from an incredibly strange and bizarre event 12 months ago to lead us to an inflation year over year. So let’s not extrapolate this out. Let’s not panic and let’s not do anything.

One of the hardest things is to not do something at times. And many people say what, we’ve got to do something. You know what? “At least I’m trying. At least I’m doing something.” No, sometimes doing something in a knee jerk reaction is the worst thing that you can do. And the best advice that I can give as your financial advisor is not to do anything. Frankly, some of the best advice that I have ever given in my career was 12 months ago or 13 months ago or 14 months ago when it was like “hey, get off the ledge”. Don’t do anything because the real people who got hurt were those that panicked. And by the time that you, as the end consumer, hear the news from that news TV channel, it’s already been priced in. It’s already happened. And so if you feel you’re getting ahead of the game, you’re not. The best thing that we can do is keep our eye on the ball which is not panic. Let’s realize that inflation, not a big deal right now. What is really inflation? Is it relative or is it nominal? Is it short term? Is it systemic or is it temporary? These are the things that we need to ask ourselves. And right now, no. The warning flags are not out there. And know those who are economists, who are really managing money, the ones that I read are not panicked, which therefore means I’m not panicked and you shouldn’t either.

Mike Brady, Generosity Wealth Management, 303-747-6455. I hope to see you soon I suppose. I’m going to be up at the cabin, but I have so many Zoom meetings. Hopefully we’ll have those Zoom meetings as well. I think I’m going to grow a beard like I did last November and turn into true mountain man except when I’m working during the day. Have a great day, a great beginning of the summer. Bye-bye now.