I was recently asked by a news journalist my opinion on how to avoid penalties on your required minimum distributions.

Of course, my first answer was to make sure you actually take them and problem solved! I think she was looking for more…..so I did in fact answer more seriously.

Personally, I always watch over all my clients that are at least 70 years old (or have a beneficiary IRA) to calculate the requirement and ensure it’s taken care of. If you don’t adhere to the rules, the tax penalty is 50% of what you should have taken out, in addition to Federal and State taxes you’ll have on the actual withdrawal.

The link below references my response to the journalist on what to do if you make a mistake.

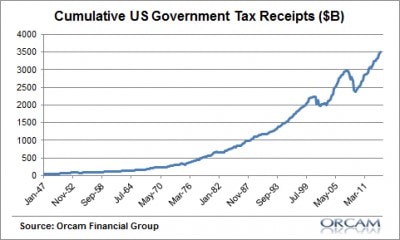

The deficit is the difference between tax receipts (inputs) and tax expenditures (outputs). The deficit has been declining over the past few years, but it’s not due to decreased expenditures, it’s due to increased revenues.

The private sector has been healing itself over the past 5 years, and it shows with the tax revenue.

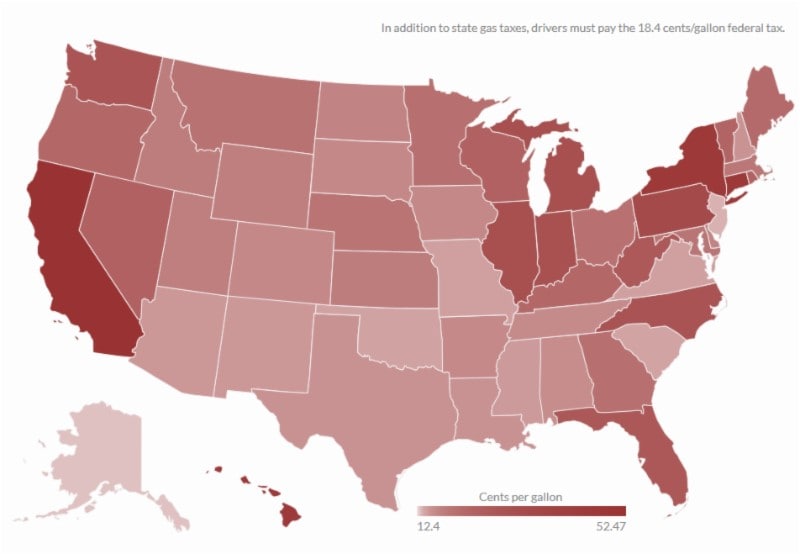

Summer is right around the corner, so I thought I’d share the really cool chart above (and link below for interactive) for the various state gas taxes across the country.

As a side note, I’m curious to see how gas taxes are addressed by states going forward. With higher fuel efficiency and hybrid technology, gas tax revenues are down since people are buying less gas.

2012 had some ups and downs, but ended up in the positive territory for the un-managed stock market indexes.

My outlook for 2013 is not quite as optimistic as it’s been the past few years for a number of reasons.

In my video, I recap 2012, provide some thoughts on 2013, and discuss my philosophy how different strategies should be considered going forward.

TRANSCRIPT:

Good morning! Mike Brady with Generosity Wealth Management, a full-service, comprehensive wealth management firm headquartered right here in Boulder, Colorado, and I am the President.

Today, I would like to talk with you about 2012, a little bit of a recap. We’ll also talk about the outlook for 2013 and what my analysis and what my opinion might be on 2013. Before I go any further, there will be a discussion here at my office, 45 minutes to 60 minutes, a seminar on the Outlook for 2013 on January 30, 2013, at 6 p.m. If you are interested in coming to that, please RSVP with Cassidy@generositywealth.com or you can call my offices: 303-747-6455. I will be sending out an invitation as well within a week or so.

Let’s look at 2012. I’m going to flip up there on the screen and you’re going to see the unmanaged stock market index for 2012. The first quarter was good. The second quarter was bad. Third was good and fourth pretty much held its own, although November wasn’t looking so good.

For the first quarter what you’ll see is if you missed January, you missed some of that first quarter’s gain and the second quarter was a tough one. That was very uncomfortable at that time. And when things like that happen (I’m going to throw up on the chart there again, there we go.) What you’ll see is it is common throughout the year for there to be declines. This does not mean that the year will end a decline. When those things happen, people have a tendency to get concerned, maybe even freak out. Last year was at 10%. The year before, it was 19% and then it was a16% decline. Three years ago, 28%. It is common for there to be a decline throughout the year.

At the end of the year, we had all of the election discussion. In case you haven’t been paying attention, President Obama did win re-election and then we went right into the fiscal cliff; right at the end of the year.

This video is really not so much about all the intricacies of the fiscal cliff and what was decided there. But in general, most people from a marginal tax bracket were not hit—39.6% for the highest tax bracket, if you’re at $400,000 or $450,000 income or greater, whether you’re single or married.

The capital gains and the dividends stayed the same for most people, except it’s now 20% for those at the highest rate. That does not mean that you are completely avoided any additional taxes. Before I go into that, there’s also a $5,250,000 exemption on estate tax and that rate did go up from 35% to 40%. However, there is a 3.8% tax for ObamaCare and the payroll tax that was 2% about a year ago, kind of a tax break, that was allowed to lapse. The full 6.2% of the employee portion of it is now going to be taken out of your paycheck going forward. You’re still going to see some kind of a tax bite at all the various ranges and income levels.

Last year there was also a little bit of a calming over in Europe but it is still, particularly in the credit market, but it is still disaster over there from a mid- to a long-term.

Let’s start talking about where we are right now in 2013. The last two or three years, I’ve been optimistic. You look back at the videos, you look back to my newsletters and you’re going to see that. I’ve always said that a diversified portfolio, while it does not guarantee a positive return, does not guarantee, particularly, in a generally trending down market that you know the perfect scenario on the outside, I do believe that it is a key ingredient to going from point A to point B in your goal planning.

Goal planning is really going from point A to point B, identifying those financial events that might knock you off and might derail you from getting to what your goal is, whatever that might be, and proactively addressing it and seeing if there is anything you can do to mitigate it.

There are a couple of different strategies from an investment management point of view as I like to think of it. There is sailing, which is like sailing your boat and then there’s rowing, like “row, row, row your boat.” Sailing and rowing.

Sailing is a little bit more passive than rowing and just think about the wind blowing it. If the wind is going in your direction, things are good and it is very forgiving of any errors you might have. The wind stops, you stop; the wind goes the other way, you might be going backwards.

If we’re in a generally upward market, this might be a good way to have your portfolio. The last two or three years, I felt comfortable, depending on the client of course. I am always making sure that it’s an individualized portfolio for them to meet their investment objectives, having less of an active trading strategy in there. Yes, we would move and allocate appropriately as the year unfolded, but it’s been very forgiving of any mistakes.

I believe in 2013 and looking into 2014, we’re going to be more of a trading range and that we might want to add in and complement some of our sailing strategies, some of our diversified asset allocation strategies with some managers who have a good track record of being a little bit more active.

Why do I think that? I think that 2013 and 2014, we’re already seeing that taxes are going up. I already mentioned that earlier. You’ve got the payroll tax, the ObamaCare tax and that is going to lead to some less disposable income.

I’m going to put up here on the chart, we’re going to see what some inflection points are and how things have looked in the last 10 years or so. From a technical point of view, we’ve had a great run in the last three or four years. The question is, are things going to continue to go straight up?

We’ve practically, in an unmanaged stock market index, doubled in the last three or four years. In the next three or four years, are we going to double? Is it going to be quite as easy? I’m a little hesitant to say something like that.

Earnings growth for the fourth quarter has not released, but it’s expected to be down. Manufacturing inventories are up, which is a bad thing. While forward PE ratios* I take with a grain of salt, the price to earnings growth ratio is higher, which is a negative thing which basically means the pricing market in relation to the expected growth.

PE ratios are higher now than they were a year, and even two years, ago. While the debt to GDP ratio for the federal government is about 103% which in my opinion, is in a danger zone. Not to make this into a political video, whether it’s a revenue or a spending problem depending on what your philosophical views are–Democrat, Republican, whatever it might be—everyone is agreeing that having too much debt is a problem. I think that we’re getting into a danger zone, particularly that debt in relation to the Gross Domestic Product (the GDP). That has me concerned.

Profits are good for corporations. They’ve been very efficient and have really cut a lot of their expenses. They are really trying to get “bare bones” in the last two or three years, which I think is great. The amount of cash that they’re holding on their balance sheets is good and high. But the question is with some bumps in the economy going forward, how much of a buffer do they have in order to ride it out? My concern is that they might not have quite as much of a buffer as we would like and what they’ve had in the past to cut expenses than they did in the last two or three years.

One of the big pieces of news in the last month that was really overshadowed by the fiscal cliff discussion was the Fed saying that they would like to phase out some of the quantitative easing in 18 to 24 months. They even pegged that 7.5% unemployment is something that would cause them to change their strategy. Whether or not what they say in their notes and what they’re actually going to do, that could be two different things.

Even Bill Gross, who is the manager of the largest bond fund in the world, he says that you have to pay the piper at some point and that it may lead to inflation. I believe that’s the case as well. I don’t know if it’s going to be inflation in 2013, but I do know that at some point, there will be increased inflation and that’s going to be a damper on some of the stock market. When you have slower growth and you’ve got inflation and when you have prices that have really seen a high rise in the last three to four years- that causes me to question whether or not that’s going to continue going forward.

Getting back to my philosophy, I do believe that there are different types of strategies—both sailing a little bit more passive and a little bit more active ones, more of rowing strategy–and having both of them may make sense in a portfolio for a client.

I’ll be talking with my clients in the next month or so to see what’s appropriate for them. I also think that having income strategies may make sense going forward and so I’ll be talking with my clients about that as well. If you’re going to take some risks, at least get some income as well. That’s one strategy and it may make sense with whatever the particular client might need going forward.

Those are my thoughts. I am going to expand upon them January 30, 2013, at 6 p.m. when I have a seminar here at my office. You’re always welcome to give me a call or an e-mail. Mike Brady, 303-747-6455.

I’m hoping that I’ve got all my notes here. I’m going to quickly look through here. It does look like it and the nice thing is I do videos throughout the entire year. If I’ve forgotten something here, I’ll just catch up with it on the next video.

You have a wonderful week and we’ll talk to you later.

Bye, bye now.

* “PE Ratio” is price to earnings ratio of a stock.

Discover 5 principles to align your wealth with purpose and possibility.

After more than three decades advising families and business owners, Michael Brady has seen that the most meaningful financial success comes from alignment.

This short guide shares five principles that help investors move from reactive decisions to intentional wealth stewardship.