It’s tempting to celebrate when your tax bill drops to zero—but is that always the smartest move? In this month’s video, Michael Brady explores why focusing exclusively on tax minimization could limit your long-term wealth and how strategic tax planning can set you up for a stronger financial future. From managing your tax brackets to considering Roth conversions, Mike shares the big-picture mindset that keeps you wealthier over your lifetime.

Read on, watch the video, and explore related case studies that show these strategies in action.

Transcript

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive full service financial services firm headquartered here in Boulder, Colorado. Although I am recording this from my place up in Wyoming, I spend the summer up in Wyoming, and it’s just a wonderful place for me to do a lot of business thinking and strategy. What are my convictions? What’s most important? Sometimes it’s good to get out of the day-to-day. Although I have to say this summer, thanks to wonderful clients like you, my friends, and my network, I’ve really met with a lot of people. I’ve had more meetings than normal this particular summer. But that’s okay. There are worse things, that’s for sure. I really enjoy staying busy, and I love my business. I like what I do. I never want to stop doing this, and hopefully you’ll always be my client.

So today I want to talk about taxes. There’s a philosophy: tax minimization or wealth maximization. Tax minimization means you do everything you can to get your taxes as low as possible, celebrating when they’re down to zero. I’m in the wealth maximization business. That means we want to make an individual, a couple, or a family as wealthy as possible. Sometimes that means paying more taxes. What would you rather have? Would you rather have $10 million in income this year and pay $2 or $3 million in taxes—which is a lot of taxes—or would you rather have $10,000 in income and pay a couple thousand bucks in taxes? Let’s keep the big picture in mind. The prize is that you become wealthier. If you double your income, your taxes are probably going to double. You could minimize your taxes by losing lots of money—a big tax loss—but that’s no good. Nobody likes that. So let’s keep our eye on the prize.

When I ask people, “Do you think taxes are going to be lower, the same, or higher in the future?” I have to tell you, nobody ever says they’ll be lower. Almost always, people say it’s going to be higher or at least the same. Then I ask, “What’s your standard of living when you retire? Do you want it to be lower or higher than it is now?” Everyone says they want it to be the same. Nobody ever chooses a lower standard of living. My experience has been that people think they’re going to spend a lot less in retirement, but that’s not true. You’re not buying suits or paying gas for commuting, but the same money gets redirected to visiting grandchildren, going on cruises, or healthcare expenses. So your expenses are not necessarily going to go down in retirement.

If we can agree that in the future taxes are going to be equal or higher, and your income needs and lifestyle might be very similar, the question is: when do we pay the taxes? We’ve got certain choices. Do we try to minimize our taxes to zero now, or do we try to pay taxes at the lowest average rate through our lifetime? One approach I take with clients is to say, “Maybe you’ve got some space within your tax bracket—10, 12, 22, 24, etc. Instead of working to get it all the way down, sometimes it’s good to say, wow, I have a lot of space in the bracket I’m in. Should I convert some money now and pay the taxes, like maybe over to a Roth, so that I don’t have more taxes on my IRA or 401k in the future when I’ll still need the money but might be in a higher tax bracket?”

We’ve got our income and our deductions. You pay taxes on the difference. If your deductions are equal to or higher than your income, you could convert IRAs all the way up tax-free. Money that would have been tax-deductible in the future becomes tax-free. We look at these things to see if there’s something you could do to minimally increase your taxes now but have a huge benefit in the future by converting to tax-free money upon retirement.

When I work with clients, I’m not a tax professional. I don’t have those letters after my name, I’m not a CPA, and I don’t have tax preparer errors and omissions insurance. I want to brainstorm with you and work with your CPA to find out—maybe as an outsider—what we can do to minimize your taxes because it’s your single biggest expense. At the same time, how do we increase your wealth over your lifetime by maybe paying a little bit of taxes now for a huge benefit in the future? At least that’s the question we want to ask so we don’t overlook it.

It’s good to know if your tax professional is a tax preparer who just takes your stuff and prepares your forms, really just a historian putting boxes in the right places, or if they’re a tax planner who gives you proactive advice. Do they meet with you during the year, maybe in the spring and fall, to decide what can be done to maximize deductions? The more deductions you have in a year, that’s great. I hope I’m not giving the impression that tax minimization is a bad thing. The question is, it shouldn’t be the only thing, the only focus. We should try to minimize our taxes, because once again, it’s the single biggest expense we have. But we also want to keep an eye on whether we should defer some of that benefit of tax minimization to the future because we might be in a lower or higher tax bracket in the future. We might want to have tax-free money, not taxable, in that future scenario. Good tax planners are worth their weight in gold. A good one is invaluable, but you’ve got to know how to work with them. I like to be part of a team.

If you’ve got a CPA you think I should talk with, please send them my way. I love having that conversation. If you have not yet sent me your 2024 taxes, send it my way. I’ll look at it, put it in the computer, look at it through my AI software, and give you some conversation pieces to discuss with your CPA. If you say, “Hey, Mike, let’s get on the phone or a Zoom with my CPA,” you can explain what you see. Tax preparers, especially around tax time, are so busy trying to do the best job they can as quickly as possible, and that doesn’t always give them the opportunity to step back and say, “Huh, what’s the tax planning opportunity here?” That’s where someone like me comes in. As an outsider, I can take the time to give you suggestions to talk with them or to give them directly to your CPA.

I love talking taxes with people. I’ve been a financial advisor for 34 years. There are few things I haven’t seen before. The best wealth maximization I can do for you means the happier you are, and then you’re bringing more people to me because you’re saying great things about me, which I would love. There’s more money left in your kitty that we can manage and that you can keep, which reduces your anxiety—and of course reduces my anxiety as well.

Mike Brady, Generosity Wealth Management. I am part of the Generosity Group, which includes Generosity Wealth Management, the wealth management part, Generosity Estate Planning, a full-service estate planning firm run by a licensed attorney, and Generosity Business Exit Planning, which is the business consulting side working with business owners who might want to transition or sell their business in the next three to five years. We help maximize the value of their business. We work and consult with them—through my business partner, Betsy—to figure out, if you’re a business owner, what do you need this to sell for to support your lifestyle, your legacy, and your retirement. If you know someone like that or if you own a business, send them my way. I love these conversations. It’s my passion. One of my niches is working with business owners who are ready to transition or want to get their business transition-ready so they get the maximum value for their legacy when they’re ready on their schedule.

Mike Brady, Generosity Wealth Management. I’d love to hear from you if you have any questions or concerns. Have a great rest of the summer. Bye-bye now.

“The world as we have created it is a process of our thinking. It cannot be changed without changing our thinking.” Albert Einstein

Generosity Wealth Management is proud to introduce a new dimension to our services: AI-enhanced tax analysis. This tool is designed to complement your comprehensive financial plan by thoroughly examining your tax returns. Leveraging advanced AI technology, this service scans your returns to identify potential strategies for further harnessing the tax code effectively. It’s not just about reducing taxes; it’s about enhancing your overall wealth strategy. Watch as Generosity Wealth Management founder, Mike Brady, explains how this tool integrates with holistic financial planning to increase your net worth, regardless of potential tax implications.

Transcript

Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered here in Boulder, Colorado.

Today, I want to talk about an added service that I’m providing for my clients and prospective clients, and to the degree that you think that I could help out one of your friends, neighbors, or family, I would love to do that. The reason why I’m doing it is I believe that there are things that you can control and things that you can’t control. As human beings, though, we’re not very good at discerning between them. We seem to spend an awful lot of time worrying about the things that we can’t control, and a lot of times, we just neglect that which we do have control over.

Taxes are one of the biggest expenses that Americans have, and they are something that we can control with certain planning. Yes, we’ve got to take this box and put it on that line, but when it comes to deductions and tax strategies, we have a very complicated tax code that, if we educate ourselves about that tax code, is in our best interest so that we pay that which we owe legally, but using the rules so that we’re not paying more than what we are legally obligated to pay and that is to your benefit.

This tax analysis is really cool. You upload a tax return to me (Secure Upload HERE), and what I do is I use something called an optical character reader, which automatically converts it into a computer line for me. Using AI and my software, it gives me maybe 20 different suggestions. After looking at your modified gross income, your taxable income, this deduction, and that deduction, and your entire tax return, it says here are 10 or 20 things that you might want to consider for this specific client. I go through that, and I say, “I really think that numbers 2, number 7, number 11, 12, and 13 are relevant for this client.” I click it, and it goes to a little report.

Click Here to Download a Sample Planning Report

I print that report out with a tax snapshot that we can then go over. The tax snapshot is your ordinary income, your long-term capital gains, and your effective tax rate. It’s very graphical; we can go through that together so that you are in “relationship” with your tax return. What I mean by that is you understand how your situation’s end result came about. This variable, this second variable, this third variable. Which are the ones that we have control over? Which are the ones that are having the most impact on you and your tax return?

As part of this video and this newsletter, I’ve included an example that comes with my software. These are not real clients, but you can see what it looks like. You can see there’s a tax pyramid so you can see which tax bracket you’re in. You can see whether you’re eligible for various phase-ins and phase-outs and that’s what we call in our industry and the tax industry all the different types of opportunities you have for various income levels. For some of them, it might be $100,000; for some, it might be $50,000. It phases out so that if you’re under, let’s say, $100,000, you’re eligible. Then it slowly goes away by the time you’re at $150,000 as an example. So, that would be a phase-out, so if you make $151,000, that’s no longer eligible for you. We can see which phase-ins and phase-outs are good for you that we should focus on, and other tax opportunities that, frankly, I might have forgotten to ask you and you might have forgotten to tell me, but it’s right there in the report that we received from your tax return.

Why would I do something like this?

It makes me a better financial planner for you. If I see the big picture that’s down on this piece of paper, it will help me do a better job for you.

I want you to share it with your CPA. I want to get to know your CPA so that he or she knows me and says, “Wow, this guy is complementing the work that I’m doing on behalf of my client, our mutual client,” which are you.

I’d love for that CPA to be impressed so that he or she says “Wow, Mike Brady is somebody that I should refer other clients to because I want to continue to grow my business.” If you’ve got friends and family and neighbors that you think would benefit, send them my way and we can talk about it. Maybe I can add value.

I’m in the wealth maximization business for clients, not the tax minimization. There are two different strategies. Wealth maximization means increasing your wealth, even if that means sometimes paying more taxes. I mean, tax minimization is you want it down to zero, which means the best way to do that is to lose money or to lose your job or to put all your investments in the mattress, not making any interest. I’d rather maximize the gain for you in your investments and your income, et cetera so that your taxes go up. But of course, your wealth goes up even faster than your taxes do. I’m in the wealth maximization business, and there might be strategies like a Roth conversion or a backdoor Roth or something else that we’ve missed that we haven’t talked about that will help you out as part of the total services that I am providing for you, the client. If you’re not a client, then prospective client.

What I am hoping that you take away from this video is that I want you to:

Send me your most recent tax return using the secure drop link that will be part of this newsletter. Secure Upload HERE

Talk with me about that. Once I do it, I’ll reach out to you, and I’ll either send it to you, and we can have a quick conversation about it, or I’ll explain what your tax return means and where you might be able to modify it to your advantage.

If you like it, pass it on to your CPA or other advisors like your estate planning attorney so that my centers of influence – my professional network — continue to grow because that helps me out as well.

When I help you out, and you say nice things about me, that helps me out, which then allows me to help more and more people out. One of the things that I like to say is that everyone who comes to me is helped, even if not everyone needs to be a client. That means that when you say nice things about me, I always take the time to help others out to increase your social capital so that you look like a hero, so it helps you out, it helps them out, it helps me out. It helps out our community. That’s really what being generous is all about and that’s why I created Generosity Wealth Management.

Mike Brady, Generosity Wealth Management. 303-747-6455. Have a wonderful day. Thanks.

“Play by the rules, but be ferocious.” – Phil Knight

As we welcome the start of another promising year, it’s not just about making resolutions but also about making wise decisions—especially when it comes to our finances. That’s why Generosity Wealth Management is stepping in to shed light on a crucial part of your financial journey: tax planning.

In our latest video, we invite you behind the scenes with Michael Brady as he guides you through the early stirrings of the tax season. Discover the critical steps you should take now to ensure a smoother, more beneficial tax return process. From understanding the significance of your 1099s to preparing your documentation, this video is your first step towards fiscal responsibility in 2024.

But that’s not all. Generosity Wealth Management goes the extra mile by offering an exclusive opportunity. Once your taxes are filed, we invite you to share your return with us. Utilizing advanced Optical Character Recognition technology, our team will meticulously analyze your documents, helping you strategize and make informed tax decisions for the upcoming year.

And if you’re not yet a client? Consider this your invitation. Share your completed tax return with us, and let’s explore how our savvy tax planning can set the stage for a prosperous year. Your financial well-being is our priority, and it starts with making smart moves today.

Dive into our video now and take the first step towards a financially secure future.

Transcript

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered here in Boulder, Colorado.

Today, I want to talk about taxes. First, I want to talk about the logistics of it before we talk strategy. The logistics, especially for my clients, are that the first 1099s will start going out around February 1. Whether you get them electronically or they mail them, the first ones go out around February 1, and then every two weeks, if you haven’t gotten it they send out another draft copy. If you’re confused by anything that I’ve said so far just send me an email. My email is up on the screen and Felicia and I will walk you through or even compile on your behalf what you need and send it to you or your CPA as a package. We want the tax document collection to be a stress free event. If you’ve got three, four, ten accounts with me it doesn’t matter with different registrations. We’ll tell you, Hey, I have these different ten accounts. You should be receiving three or four, and here they are. Or we might say you need three or four documents. Two of them are ready, and two of them are still waiting. Because of complex reporting requirements, some 1099s don’t go out to clients until February or March, which is kind of irritating because you want to get your packet together and get it into your CPA, but that’s the reality. Many 1099s are done right at the beginning of February, and then there are a few stragglers that for whatever reason sometimes clients haven’t received them going forward even into March. Be patient, don’t get frustrated. Give me an call or send me an email and Felicia and I will get you hooked up to tell you what the status is.

The second thing I wanted to talk about is this really cool report that I have and I’d love to offer it to all my clients as well as people who are not my clients but are watching this particular newsletter. Once you get your 2023 taxes done I will provide you with a link so that you can upload it to me and I will have this optical character recognition, or OCR, and it will convert that into my computer into this wonderful little spreadsheet. It will tell me everything about your tax returns and even some areas that we could have a conversation for tax planning within the year 2024. What I like at the end of that conversation is I’ll go over it with you once I have your tax return for 2023 and say hey listen, let’s understand what the present situation is and then we have two or three or four different avenues for looking at hey, maybe we can save some taxes here or we could do a conversion over here, et cetera. Just so we can have the conversation as 2024 unfolds. Please take me up on that. It is free and I’d love to talk with you, I’ll talk with your CPA, your tax preparer so that we’re all on the same page.

Most people’s single biggest expense is taxes, but they don’t understand their taxes. They don’t under what options they might have before them, and that’s what I want to do is help you so you can have that conversation with your CPA or we can loop in your CPA and have that conversation together.

That’s it for today’s video. I just wanted to let you know 1099s are coming down the pipeline. They’re going to arrive in February and March. If you have any questions send me an email or Felicia and we’ll get you hooked up. If you’ve got your 2022 we can do it immediately. We can look at what your 2022 taxes were, but definitely when you get your 2023 done send it to me so that we can have a really good conversation and do some tax planning.

Mike Brady, Generosity Wealth Management, 303-747-6455. Have a wonderful day. Thanks. Bye-bye.

I was recently asked by a news journalist my opinion on how to avoid penalties on your required minimum distributions.

Of course, my first answer was to make sure you actually take them and problem solved! I think she was looking for more…..so I did in fact answer more seriously.

Personally, I always watch over all my clients that are at least 70 years old (or have a beneficiary IRA) to calculate the requirement and ensure it’s taken care of. If you don’t adhere to the rules, the tax penalty is 50% of what you should have taken out, in addition to Federal and State taxes you’ll have on the actual withdrawal.

The link below references my response to the journalist on what to do if you make a mistake.

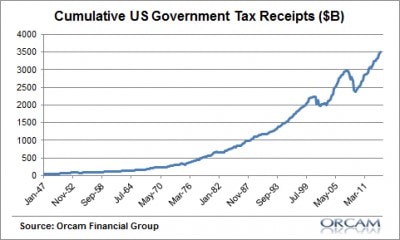

The deficit is the difference between tax receipts (inputs) and tax expenditures (outputs). The deficit has been declining over the past few years, but it’s not due to decreased expenditures, it’s due to increased revenues.

The private sector has been healing itself over the past 5 years, and it shows with the tax revenue.

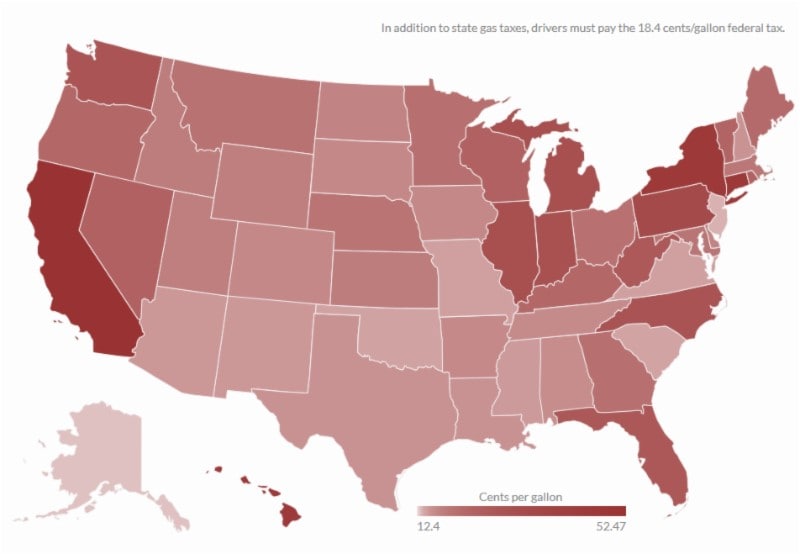

Summer is right around the corner, so I thought I’d share the really cool chart above (and link below for interactive) for the various state gas taxes across the country.

As a side note, I’m curious to see how gas taxes are addressed by states going forward. With higher fuel efficiency and hybrid technology, gas tax revenues are down since people are buying less gas.