“There is nothing either good or bad, but thinking makes it so.”- Shakespeare

Don’t let your long-term financial investment strategy be distracted by short-term events like the debt ceiling debacle. Is it annoying? Yes. Do we know what the ramifications will be? Not exactly. So, the best bet in this scenario is to look at that focal point on the horizon and ride it out. Don’t do anything.

Here’s why:

Transcript

**Recorded May 25, 2023**

Mike Brady, Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered here in Boulder, Colorado. Although I’m talking to you from Generosity Wealth North Headquarters which is in Dubois, Wyoming. I come up here every summer. It is wonderful to get away and get my mind in gear. Where are things going and look at the big picture without having to get so much into the details. I’m available via phone and Zoom and email. Of course, I go down to Boulder for things that have to be handled in person. I am here recording this video and writing this newsletter from my cabin in Dubois.

I would love to talk about investments or this company or that company, this bond, whatever it might be about their future earnings and whether we should invest in it. That’s what I’d love to talk to you about. Or I would love to talk to you about all the other variables in your financial equation that could help you reach your financial goals. Isn’t that a great productive way of using our time?

But instead I’m talking about an irritating government potential shutdown due to the debt ceiling. I don’t venture into politics hardly at all. Why? Because I want to serve both sides of the aisle. I want to have people feel comfortable sharing with me their fears, and I have found that people have different fears depending on how you view the world. I’m here to help people reach their goals no matter what. I’m also not interested in only working with people who might think just like me. I’m a better person when I interact with all types of people.

This is manufactured drama that just absolutely irritates me.

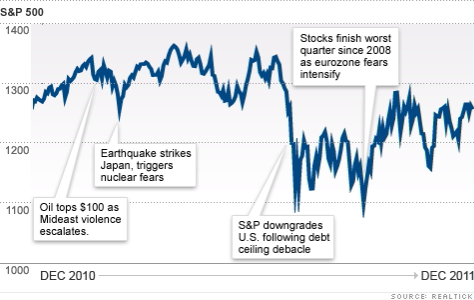

The last time that this happened in any substantive way was in 2011. Do you remember what happened in 2011? Let’s go back and talk about that. There was a lot going on in 2011. We had all of the European debt crises. Remember Portugal and Italy and Greece and Spain. They weren’t able to make their debt payments. I mean in 2008 they took on a lot of debts and now they weren’t able to do it. That was the underlying backdrop to which the summer of 2011 had where the debt ceiling was finally resolved around August 2. They actually kicked the can down the road and they said it’s good for right now if we do this thing in the next year or two which fell apart. But that’s beside the point.

August 2011 the market had been up for the year and then it went down about 19 percent. The S&P and Moody’s and the rating agencies had downgraded the U.S. Government from the highest rating to the second highest. Now, the fourth quarter of that year it recovered. What a lot of people don’t remember is that the unmanaged stock market indexes were basically flat for 2011 or positive depending on which one you want to look at. It wasn’t some huge decline for the entire year although it did give up some of the gain that had been acquired the first half of 2011.

So all 2012, 2013, 2014 all positive years. In a long term multiple year strategy, 2011 – especially the third quarter of 2011 was not attractive, wasn’t fun whatsoever. But when we look at the bigger picture, it was just a blip.

I have no idea what’s going to happen with the debt ceiling conversations that are happening right now. I do know that if you’re looking for something to be negative about, this is a great thing to be negative about. It’s just so irritating if we had a corporation with a board of directors and a CEO that ran its company like this country is being run, at least the federal government is being run, we would have a real problem and we would say that’s malfeasance and it’s really quite frustrating. It’s kind of a Rorschach test. Depending on what side of the aisle is who you blame. I don’t want to really get into that. I don’t know if it’s Congress’s fault of if it’s the President’s fault. It doesn’t really matter. It is here and it’s what we have to deal with.

I have to say that a frustrating thing and I have to admit I don’t really have a solution to is just how much the government and the federal reserve is having on our investments. I mean you’ve heard me already say that it’s in my opinion that much of 2022 was a correction of 2020 and 2021 when the markets went up and they shouldn’t have. We closed the world economy and we dump a lot of money in which is basically borrow from the future in order to prop up companies and the stock market and it goes up 2020 and 2021 of which we gave it all up in 2022. It certainly from my point if view it would have been better if we’d been zero percent and zero percent and zero percent instead of up, up and then give it all up in last year, the third year.

So far this year we’ve had a positive in the unmanaged stock market indexes. I don’t know how the end of the year is going to unfold, but companies when you look at their profitability, when you’re looking at the efficiency that they’re having, absent government influence, absent the emotions that come with the federal government having their particular issues there’s a lot to be positive about, especially when we look at where it came from which was seven-eight months ago.

I mean when we look at October, remember how I keep saying that we had a fourth quarter of last year was positive. The first quarter of this year was positive. I don’t know about the second quarter. I mean we’re going to see. But what we don’t want to do is have a long-term strategy dictated by short-term events and those short-term events are what the federal government is going to do. Just give me something that I absolutely can’t guess at.

It does have a huge impact. I don’t want to minimize that, but I want to go forward with those things that I do know, that I can control – the variables in my life. Do I have the right allocation? Am I saving enough money? Do I have proper insurance if unforeseen things happen like the death of a spouse or loss of the ability to work or have to go into a nursing home. Those are things that I can control, and I can have the investments with a long-term strategy in order to overcome the speed bumps that will always happen. It will always, always happen. Every year there is something that is big and it feels catastrophic and somehow and magically the stock market and the bond market, especially when you mix them together, perseveres over a number of years.

So, don’t do anything. We have a long-term strategy. That’s what I talk with clients about all the time, and I don’t want to be distracted even if there’s something really big like now, it’s a big distraction by the short-term events. I certainly hope that we don’t have a decline and we give up what we earned so far this year. I want 2023 to be the year where we really start to make big inroads into that which was lost in 2022. And when you consider that 2020, 2021 and 2022 and really add all those things together, it’s about flat. I want to start moving forward to where we were back in 2019. We had some great years leading up to 2020, but really up until the last two-three years when we had positive year, positive year, negative year.

I don’t think there’s anything that we should do or could do or plan to do for this thing that is unfolding, this latest drama. We’ve got to keep our eyes on the big picture and that is having great investments, having a great allocation in the country that I still believe is the greatest country out there, especially from an investment point of view when we look at all of the others that are out there. Absolutely not perfect. I hope you’re never hearing that from me, but this is where the wealth, the innovation, all the creativity happens and I’m happy to be a part of that.

Mike Brady, Generosity Wealth Management, 303-747-6455. Thank you.

generosity starts with Your mindset live generously Generosity is the most natural outward expression of an inner attitude of compassion and loving-kindness. – Dalai Lama Living generously isn’t just about giving money away – it’s about using...

“Set your course by the stars, not by the lights of every passing ship.” – Susan Blankston

The first quarter of 2023 has been marked by mixed financial market activity but has overall been a positive correction of the losses in 2022. The volatility and banking issues have further highlighted the importance of duration. Bad risk management on the bank’s part with incompatible duration led to issues as their long-term investments and short-term liabilities created a run on the bank. This serves as a good reminder to investors to assess their time-horizon and what the need for cash will be as they make decisions.

Let’s take a closer look at the first quarter of 2023 and what we’ve seen so far in relation to duration.

TRANSCRIPT

Mike Brady with Generosity Wealth Management, a comprehensive full service financial services firm headquartered here in Boulder, Colorado.

Before I jump into the first quarter review, many of you have asked how my knee surgery went. On March 1 I had a full knee replacement so good titanium in my knee now and it’s gone great. I have kind of a dull ache even a month later but I have to tell you that my flexibility is great, the pain never was very bad and if you’re ever looking for a great surgeon I love mine. It’s worked out well but I’m still in the rehab doing the PT and all of that. Thank you for all of your concern on my behalf.

Let’s talk about the first quarter. The first three quarters of 2022, a year ago, were absolutely horrible. The declines of 2022 really occurred in the first nine months of last year. The last quarter of last year when you look at the unmanaged stock and bond indexes was actually slightly positive. January of this year was highly positive which is great both for the unmanaged stock market indexes and for the bond indexes. February and March was really more static and sideways. We’ve got the fourth quarter of 2022 followed by the first quarter of 2023, both of them positive and starting to dig ourselves out of the horrible hole that the first three quarters of 2022 gave us.

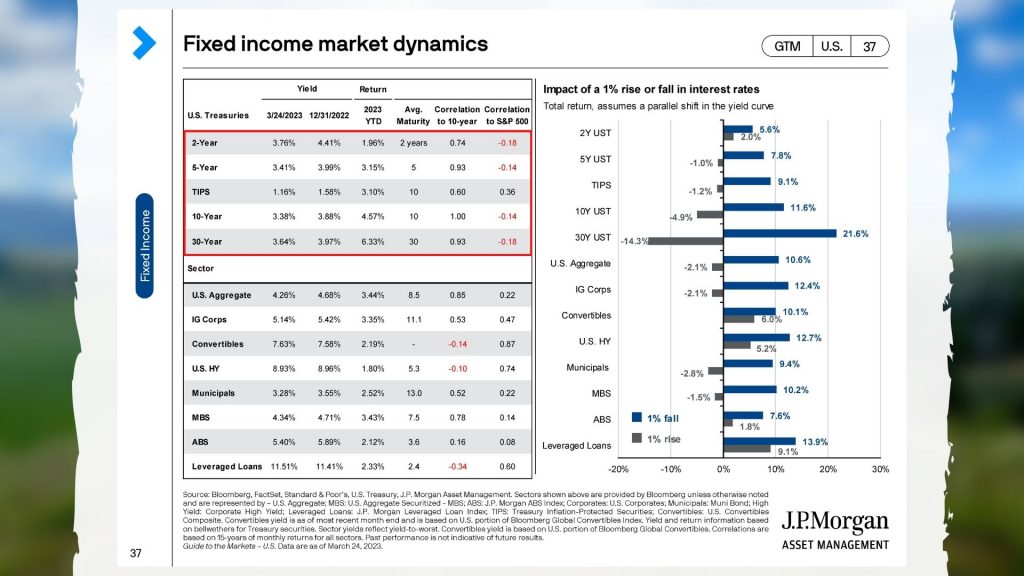

I’m going to put up on the screen unmanaged bond indexes. You can see that last year was negative. So far this year it’s positive. When interest rates come down, bonds have a tendency to go up and the yields go down and stuff. I just want you to understand how that has an inverse relationship. What was so unique about 2022 is that not only did the unmanaged stock indexes go down, historically about one out of four years are negative, but bonds as well because of the incredibly quick rate with which the Fed increased the interest rates.

So far this year, 2023, things have eased up. The bond prices are increasing which is a good thing. I’m going to put this up on the screen and you can see how even the different durations from two years to 30 years, the prices have increased for this particular year, but they’re talking about slowing down the interest rates. The whole reason that the bonds took a huge hit last year, 2022, if it plays out in 2023 that actually will be to our advantage. Very unique last year both the unmanaged stocks and unmanaged bond indexes both went negative. So far they’re in recovery in 2023.

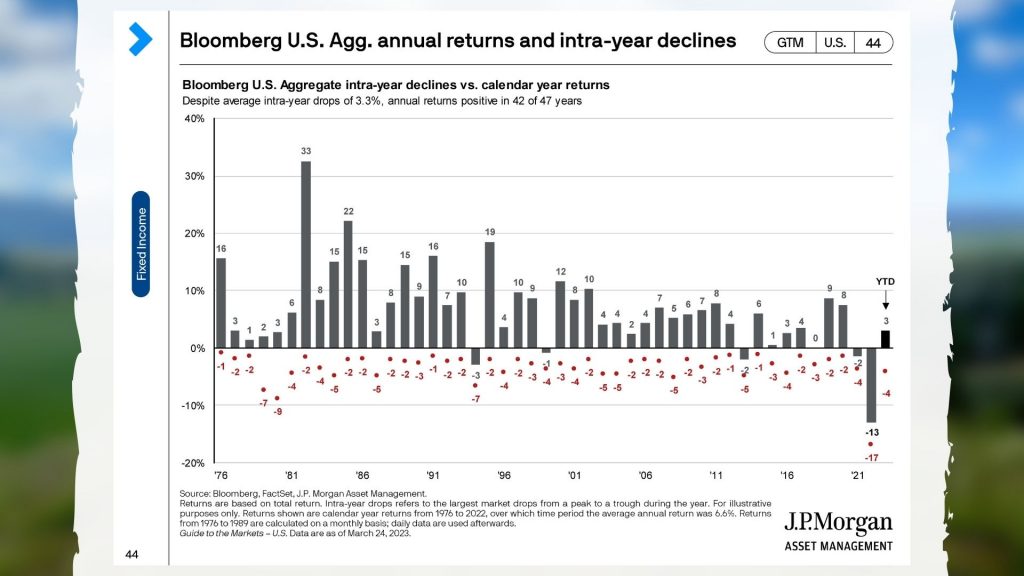

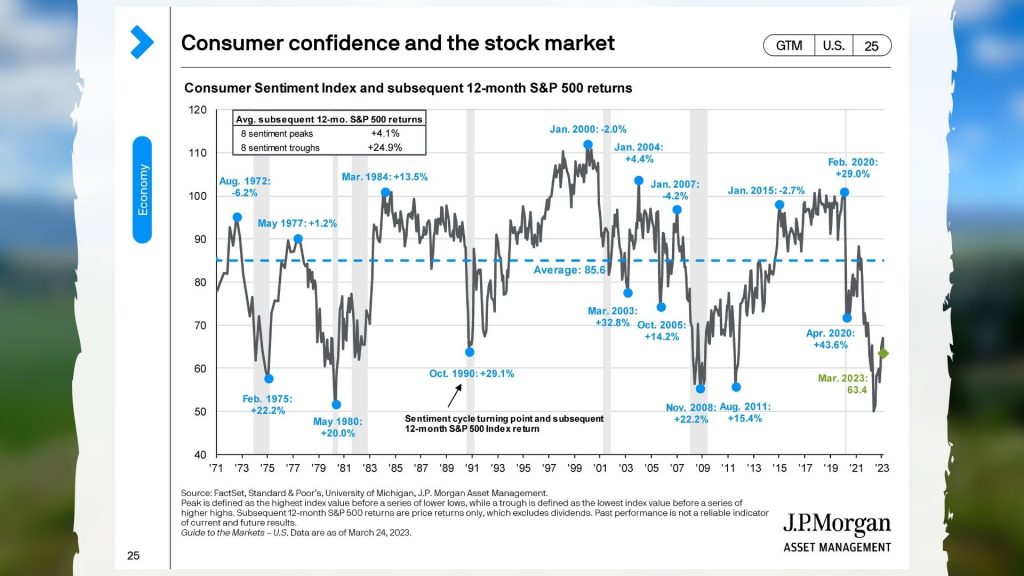

It’s important for us to remember that and I will also say that sentiment is not a very good indicator of what’s going to happen. When people are at their most positive, the next 12 months usually aren’t looking very good. When people are at their most negative and when they’re like well, I’ve just got wait for this to play out, is usually the next 12 months very, very positive.

I’m going to throw up a chart that shows something like that. Here we are and we’ve got two positive quarters in a row. I don’t know what the rest of the year is but I will tell you, I’m going to put up on the chart what they’re anticipating some of the interest rates amount to be from the Fed, and also some of the profitability going forward. It’s reasons to be positive, to dig ourselves out of it. Nobody knows what the future holds and that’s why duration – your time horizon is absolutely essential.

When we talk about the banks, some of the regional banks, let’s get the right lesson from them. They had bad risk management inside with incompatible durations. Investments were long term and their liabilities were short term and they had a run on the bank. It’s important for us as investors with our own portfolios to day hey, what’s my duration? What’s my need for cash? When will I need this? I might be in my 70s but hopefully I’m going to live another 20 years. So, making sure that the investments that I have are, of course, for the right duration for not running out of money for the rest of my life or moving towards retirement, whatever your specific goal might be.

Anyway, I’m always here to have these conversations with you and to ensure that what we’re doing on your behalf is consistent with what you want to do in your financial goals in your life.

Michael Brady, Generosity Wealth Management, 303-747-6455. Thank you.

“No one has ever become poor by giving.” — Anne Frank

2022 was a disaster. But January came in hot, making up a good chunk of any losses from the previous year in just one month. January was one of the best months in years for both the unmanaged stock market indexes and bond indexes. This is now the fourth month of a recovery. October, November, December and now January. The rest of the year is an unknown, only time will tell, but like we always say the best thing we can do is be patient.

Let’s take a closer look at what we’ve seen so far in our February 2023 financial market update.

Transcript

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered in Boulder, Colorado.

2022 was a disaster. Both stocks, the unmanaged stock market indexes, the unmanaged bond indexes down pretty sharply double digits, very unique that both of them went down at the same time. If you watch all my videos and newsletters from 2022, I deconstruct some of my thoughts about why that is with the supply chain issue which led to an interest rate issue with the reaction to that. We’ve got both fiscal, tons of money, money supply increasing so we’ve got some fiscal, we’ve got some monetary, we’ve got supply, all these things coming together.

I will tell you that January was one of the best months in years for both the unmanaged stock market indexes and bond indexes. As a matter of fact, you’re going to see this in a second. A good one-third to one-half of all that was lost in 2022 was made up in just one month which is January. I will tell you that this is now the fourth month of a recovery. October, November, December and now January. I don’t know what the rest of the year holds for us but I’m a broken record. I said three out of four years are negative. That means that sometimes there’s – sorry, three out of four years are positive, excuse me. Quite the opposite. Three out of four years are positive and one out of four are negative which means that we sometimes just have to be patient. The best thing that we can do is be patient.

Up on the screen there you’re going to see this is the unmanaged stock market index, the S&P 500 going back to 1980 and you’ll see that so far this year, this is the first week of February it is positive. You’ll see last year that arrow there that was last year. This next one up on the screen is the unmanaged bond index. Bonds went down last year in a reverse to the increasing interest rates and so far this year you can see that a good third of the decrease in the bonds has been made up already. You can see that right here. I’m going to put in a block there. Depending on the duration the length of a bond from short to long, you can see what the year-to-date return has been on a bond right there in that highlight.

This next screen I want to highlight the bottom right corner. Historical markets drawdown and the next 12 month rebound. You can see the tech bubble, the global financial in 2008, you’ve got COVID. After there’s been a decline, there’s been a great recovery in the next 12 months.

I don’t know if that’s what we’re in. I have no idea. The future is inherently unknown, but the way I like to think of it is you’ve got your Apple maps, you’ve got your Google or your Waze, whichever way that you get navigation to find someplace on your smart phone. You thought it was going to take you 30 minutes and you see that there’s an accident up ahead. It was unplanned, it’s unpleasant, you hate it. But you know what? The path that you’re on is still the right path. Doing anything else it’s so easy to want to get on a side road when really perhaps it’s really being sidetracked.

This next sheet up on the screen is showing – I’m going to put a circle around it which is inflation. Inflation in the last year or year-and-a-half was significant. It was the reaction to it that caused a lot of the bond decline over the last 12 to 18 months. What you’ll see is on this next chart that sharp increase all through the year of 2022 causes the bond market to go down. You’ll see the decrease that is expected from the Fed. We’re getting a handle on the inflation.

Let’s go back to that chart that I just showed, the previous one. You’ll see that on the right hand side inflation is starting to come down. It’s starting to creep back down which is wonderful. The reasons that bonds went down in 2022 and the last little bit of 2021 is the environment is reversing which is very, very good.

I could sit here and talk about other encouraging signs both from the economic forecasts and the stock market forecasts and the reaction to it, but I want to keep this one short. All I really have to say is the last month has started to negate some of the very long and painful quarter upon quarter, three quarters last year that were negative and one quarter that was positive. That one quarter that was positive was the last one and now going into this first quarter of 2023.

I’ll continue to do my newsletters and videos throughout the year. I’m going to try to do them a little bit more often as we really work to get to breakeven and then going back onto our original plan which, of course, is why would you have investments if you don’t believe that long term they’re going to be higher than they are today.

Mike Brady, Generosity Wealth Management, 303-747-6455. You have a great day. See you. Bye-bye.

Humility, like gratitude, is not so much a technique as it is a way of life.” – Ed Latimore

Tough 2022 Year,, which should remind us of the need for keeping the big picture in mind. While your goals may change, having a steady and reliable plan is crucial all year round.

In my latest video, I review the year in detail, and talk about what made 2022 such a horrible year. There is no sugar-coating it, practically every market sector lost money.

What does 2023 have in store for us? Is there anything to be optimistic about?

Watch the complete video to hear me talk about how one year does not a long-term plan make.

Transcript

Hi, there. Mike Brady with Generosity Wealth Management, a comprehensive full-service financial services firm headquartered right here in Boulder, Colorado.

Today is my 2022 Year-In-Review, and our 2023 Preview. I’m recording this on December 26. I want to do it even before the end of the year is over, because I want to get it out to you as quickly as possible.

What’s interesting about 2023 for me personally is this will be 32 years of doing wealth management, meeting with clients. There’s an old adage that says that history doesn’t repeat, but it certainly does rhyme. That’s one thing that I’ve noticed as I’m talking with people and watching TV is this inherent conflict between fear and greed.

As I mentioned, I’ve doing this for 32 years, so when I started it was the high-yield bonds were all the rage, and then from high-yield bonds it went into the mid-90s went to – well, gosh, you should be doing day trading yourself – it’s so easy and the tech bubble. That led to – after that, it was in the 2000s real estate and we had kind of the crisis in 2008. At that time, I remember a lot of people then ricocheting, you know, kind of going to the other extreme saying, no, gold is where things were in the 2010s, which then led to, well, no, I’ve now got to chase Cryptocurrency. “If you’re not doing Crypto, you’re kind of just old school.”

Well, you know what I’m hearing a lot on the news or as I’m talking with people is individual stocks. “No, we’ve got to do individual stocks or where we’re going to do these individual stock plays.” I stay firmly , even though the last year has been horrible. I do want to acknowledge; it has not been fun. I’m going to talk about that in just a few minutes, of having a broad-based, market-based investments that’s long term. And long term is multiple years, not one year. If you make long-term decisions based on short-term events, eventually that’s going to cause you to pinball from one investment strategy to another investment strategy and, unfortunately, there is no end to the number of people who will promise what you want to hear. I just don’t want to do that. I don’t think that you’re well served by trying to jump from strategy to strategy. I stick by the broad-based, market-based third-party management strategy because long term I believe that that’s been the best strategy for investors and best strategy for you as well.

Let’s talk about 2022.

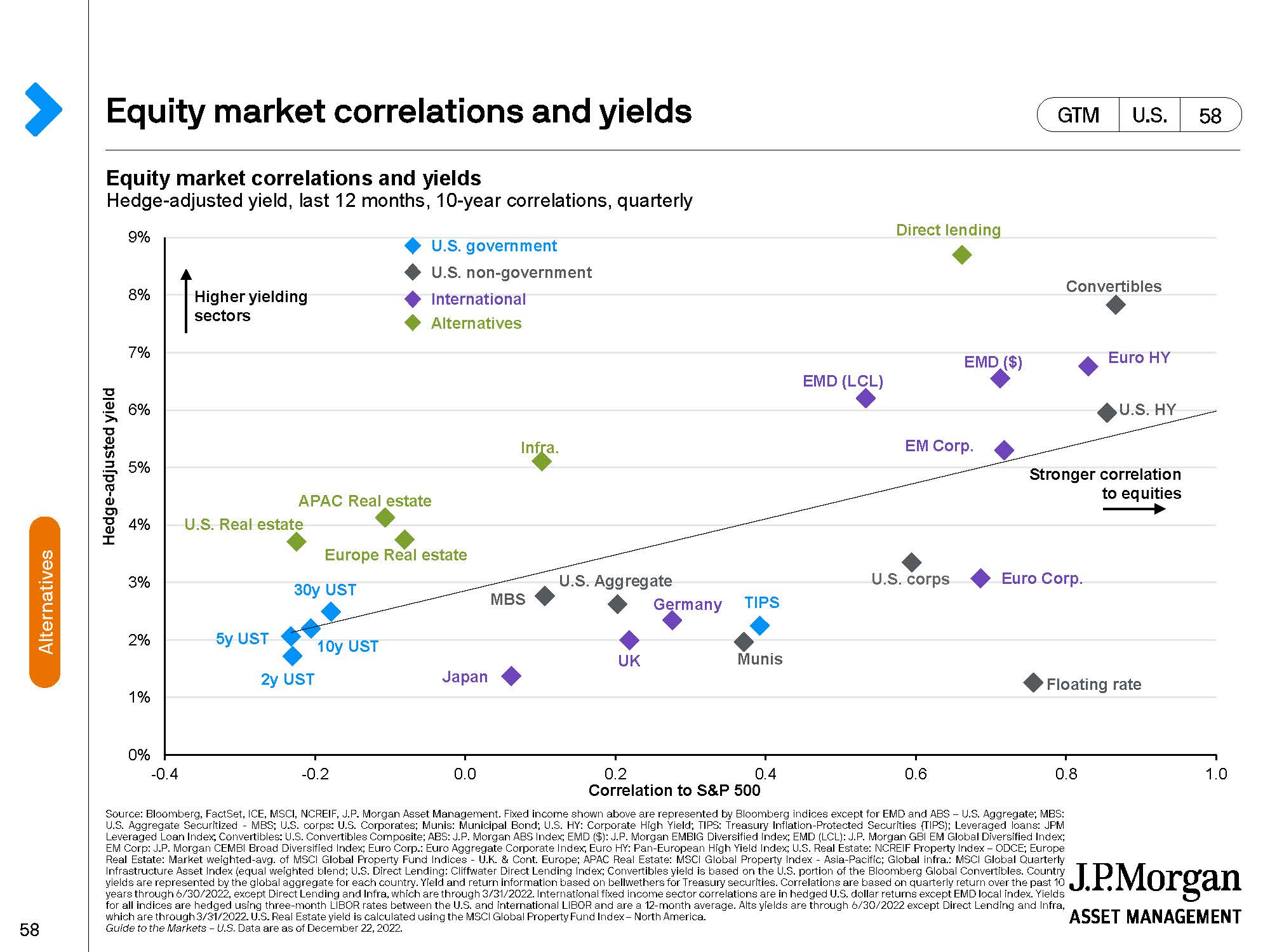

Up on the screen, up on the left-hand side you’re going to see – on the bottom axis there, the X-axis is correlation to the Unmanaged Stock Market Index (S&P 500). The more to the left you are, the less correlated. That means that when it zigs, it zags, okay. If the – it actually does the opposite. So that’s why those U.S. Treasuries are there on the left-hand side over the last ten years. When the stock market’s gone up, it’s gone down. The other way around. There’s not much correlation to the Unmanaged Stock Market Index.

The same thing with Treasury Inflation-Protected Securities, which I’ve just circled. And U.S. Aggregates, which are bonds. So, bonds in general are a great thing to couple with some kind of an equity. This past year, that did not happen. We’re going to talk about it in just a second.

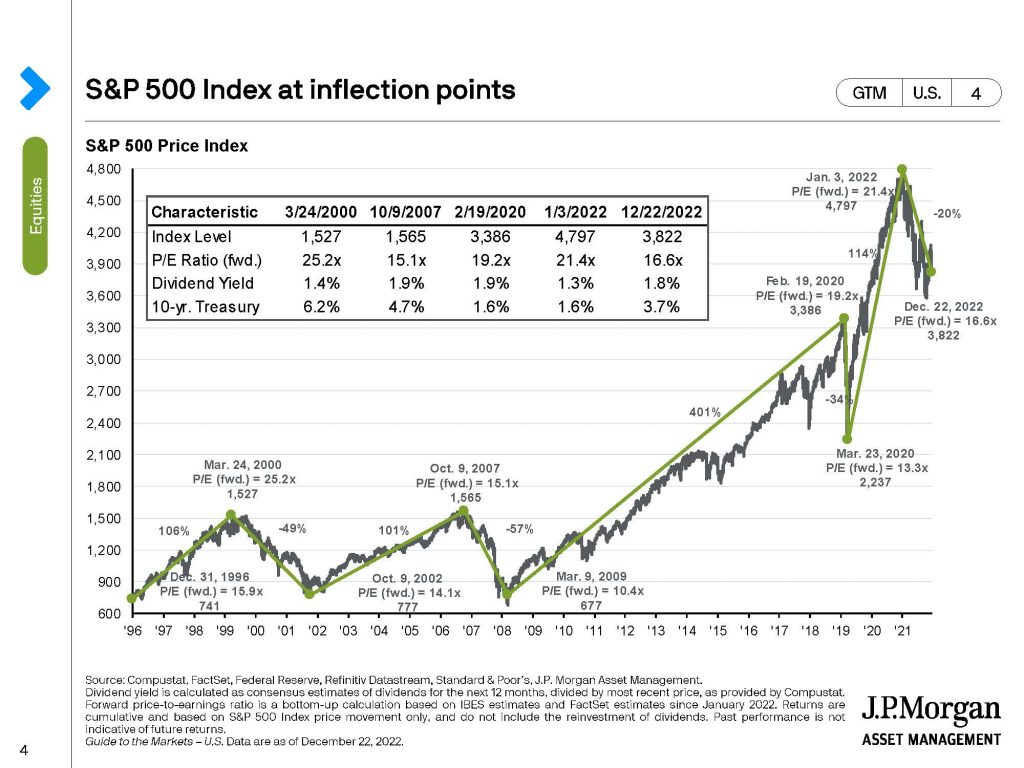

This next graph up on the screen is the last 30 years of the Unmanaged Stock Market Index (S&P 500). You’re going to see this year we gave away two years’ worth – about two years’ worth of growth. We’re back to where we were two years ago; it’s that simple. It’s not that you gave up ten years’ worth, or 20 years’ worth, no. We gave up a couple years’ worth. Not fun. Not trying to say that it’s good. We want to make money as many years as we can.

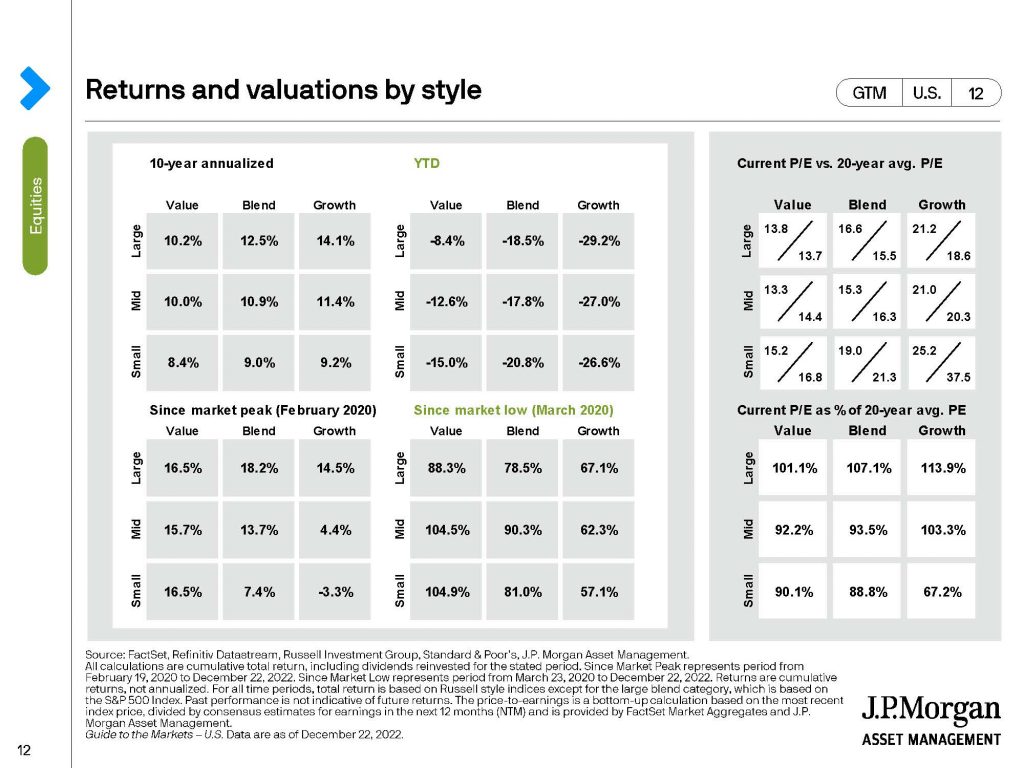

This next screen, I’ve just circled, kind of put a square around the box of last year. You’re going to see that whether it’s large-cap or small-cap, value or growth, it was negative almost double digits across the board. Very poor year for the Unmanaged Stock Market Indexes. When we look out to the box that I’ve now put to the left, over the last ten years, that’s the average rates of return. You can see that that’s why we have to look at the averages, the annualized numbers, not just one year. You cannot make decisions based on just one year. That is an amateurs way to go through your portfolio life.

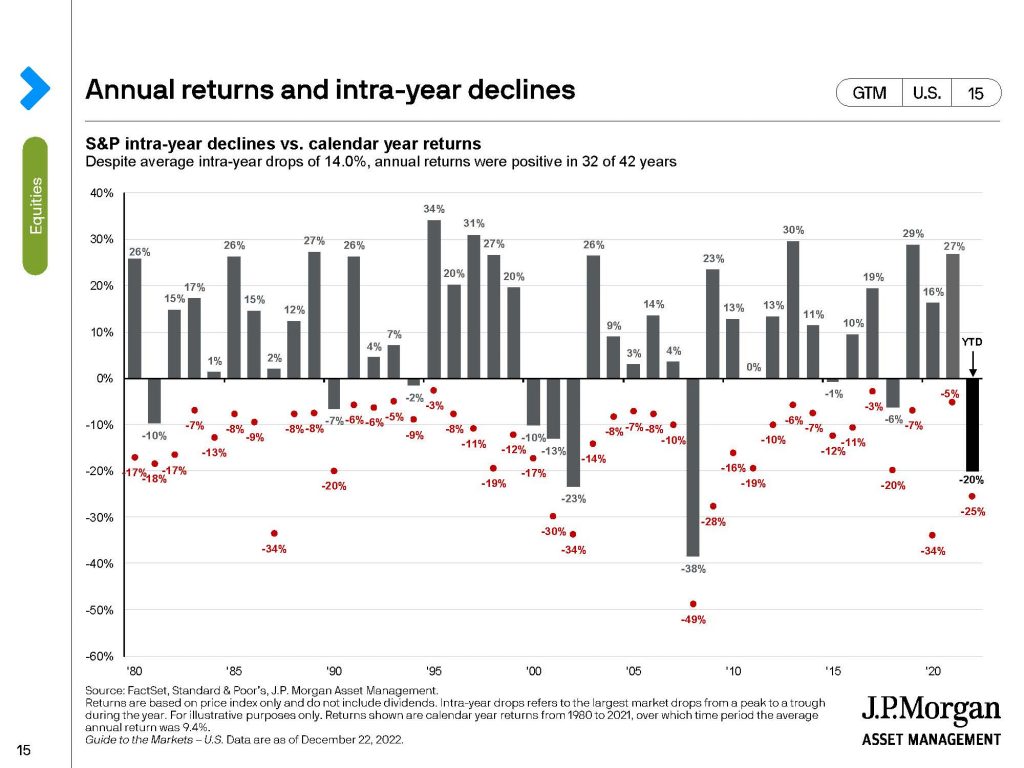

On the next screen, you’re going to see 40 years. Forty years of the S&P 500. Three out of four years are positive, which are the numbers above the axis. One out of four are negative. I’ve just circled the ones in the last ten years; there were three negative years. This was the worst year of the last 12 years, since 2008. You’ll see that that’s not every year. You’ll also see that it has happened that there’s been three years negative before. That was 2000, 2001, and 2002. I certainly hope that’s not going to be the case this time, but it could be. But we’re going to talk about that in a second. Let’s not assume that every year is going to be negative. As a matter of fact, after those three years, significant number of positive years above the axis, even after those three negative years.

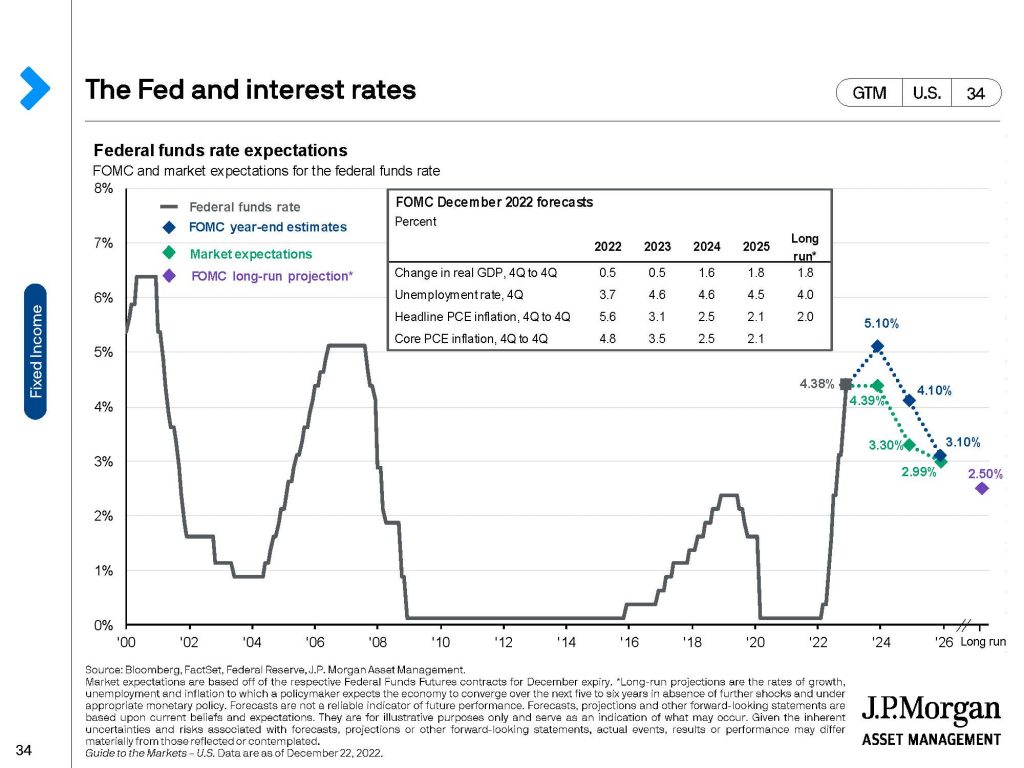

Why did some of this happen? This next chart shows the Federal Funds Rate, just what the Fed does. You’ll probably see this on TV, went from practically zero up to 4.38 percent. Significant. Look at how sharp it changed in one year. One year. That’s really dramatic.

As we go, and I’ve just circled it. Some projections going forward over the next year or two, projections that will maybe go a little bit higher, possible. It depends on how the economy plays out or stays and goes down negative. Alright. But a very sharp correction in 2022. One of the two or three main factors for the poor performance that we had in 2022 was the dramatic reaction by the Fed to some underlying fiscal policies, a significant amount of money that was thrown out into the world and supply problems.

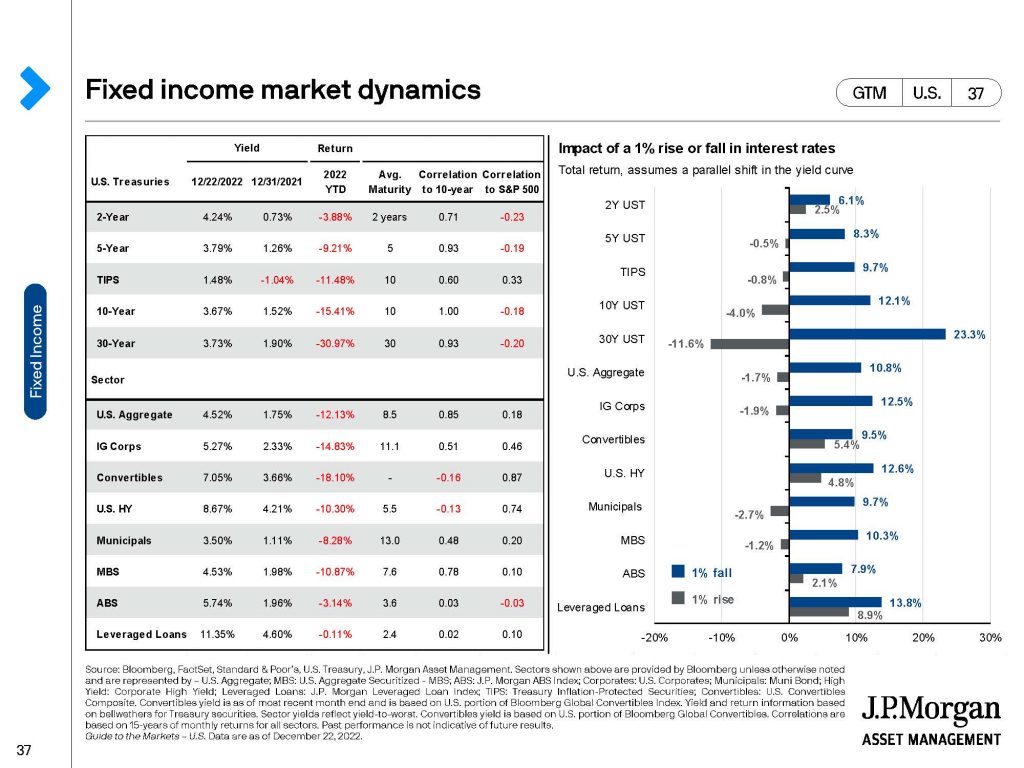

The next page, up on the screen, Fixed Income. These are bonds; these are Unmanaged Bond Indexes. You’re going to see this year, 2022, across the board, whether it was short, which is that top number there, all the way down to long-term bonds double digit declines. This is the first time in over 50 years where bonds and stocks have both gone down over ten percent. First time in 50 years.

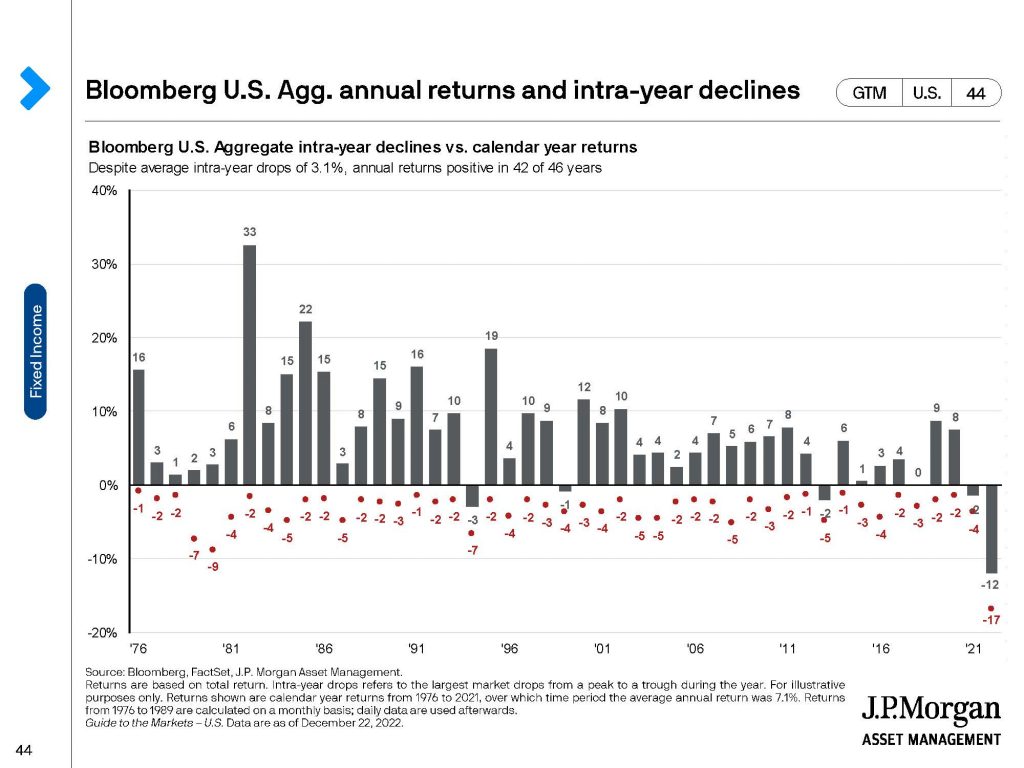

This is it for the last 30, 40 years. Forty years. You’re going to see that the vast majority of the year, above the X-axis for the Aggregate Bond Market, Unmanaged Bond Market is positive. This year it is not. That’s the exception, not the norm. We’re talking the late 70s as well. We’re talking years where inflation was significantly higher than even where it is right now.

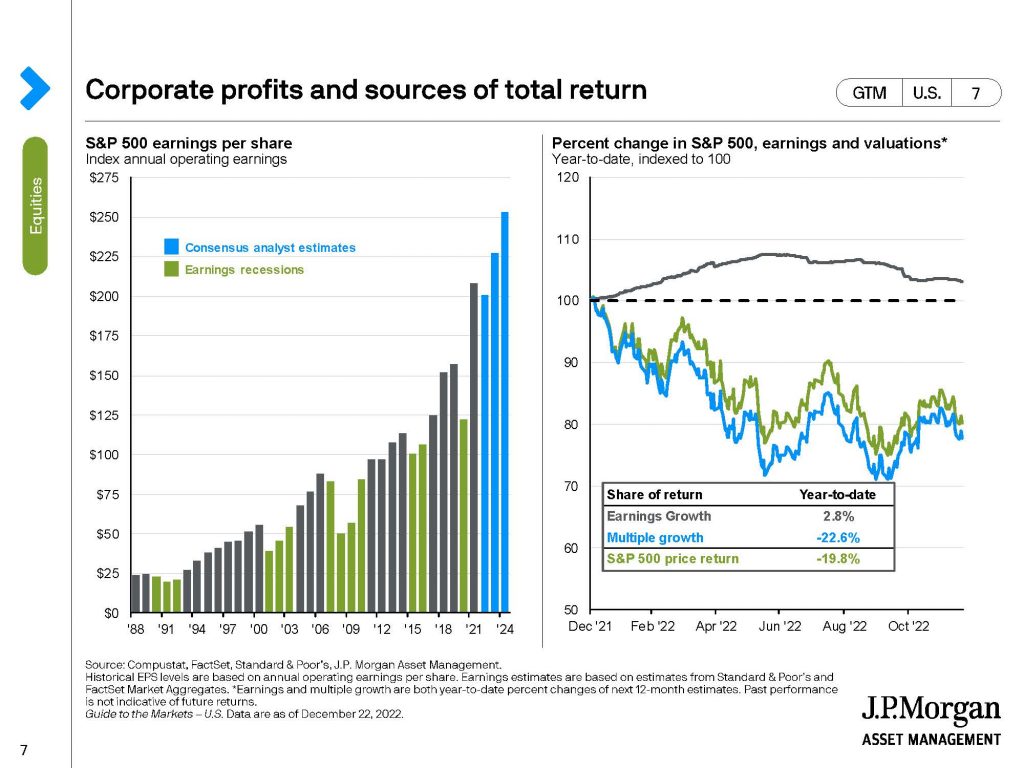

The next page, let’s talk a little bit about going forward. You’ve got the blue that I’ve just circled there is Consensus Analyst Estimates for Earnings Per Share (EPS). Yes, the S&P 500 Stocks on average in Aggregate have been beaten up. Some prices gone down, but the earnings are looking real good.

Right now, in the last two, three months, you’ve heard a significant amount of belt tightening with companies as they’re trying to be more efficient, trying to decide what the next year or two – a high probability that we might be in a recession, going forward for some time. But from a portfolio point of view, we want to be in a market that is perhaps underbought, oversold and that is still one of the things that we’re watching, that I’m watching.

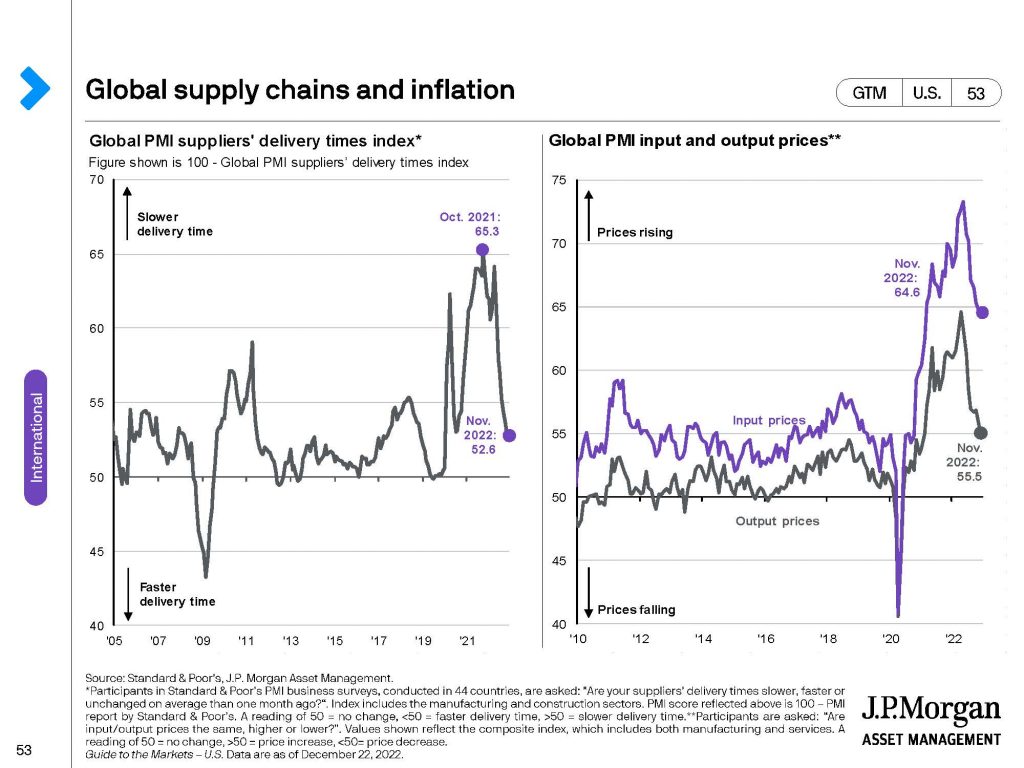

You’re going to see here on the next screen, Global Supply Chains. Great. We’ve gotten through. That’s good that it’s gone down; that’s the thing that I just circled. It has decreased the time to get supplies to us. Is China continuing to be a problem? Yes. That whole Zero-COVID measures, not very helpful. To them or to the global supply chain. As we’re re-entering kind of a new normalcy, as they have basically changed that policy, this is a good thing. The geopolitical going forward, our relationship with China, both the United States and the world will play out in a significant manner over the next couple of years.

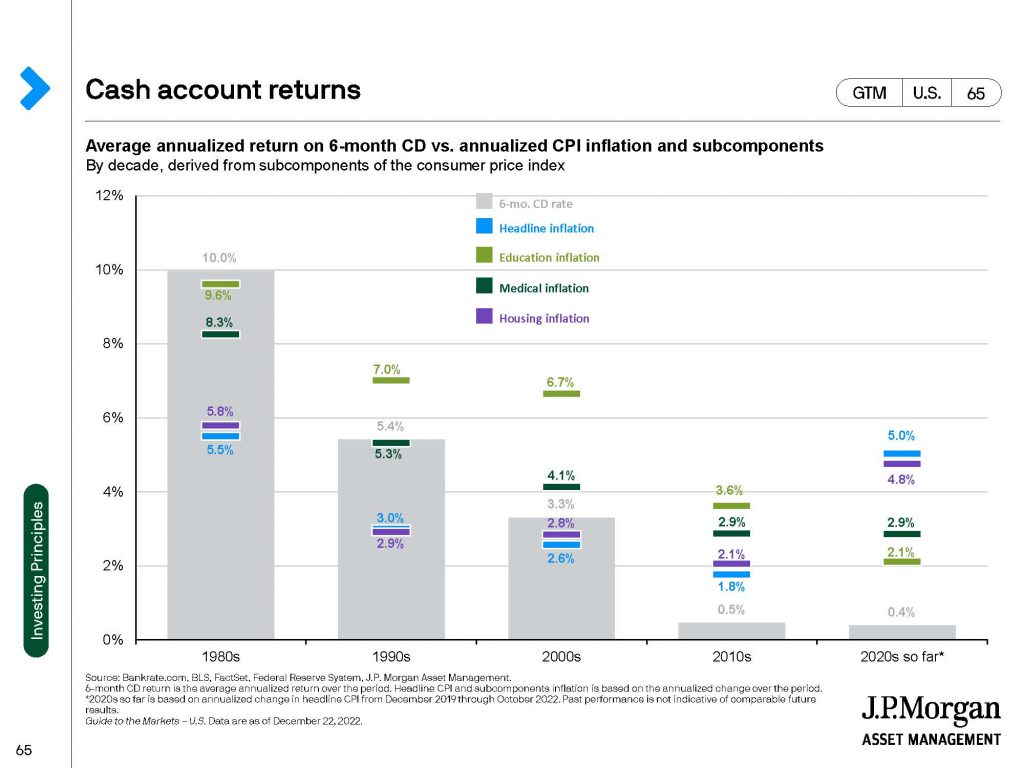

Kind of a last thing that I want to talk about from a chart point of view is that far right-hand side CDs – 6-month CD rate still relatively low on average the 2020 so far. The inflation is much higher than that. So, just keeping your money in Money Markets and CDs just isn’t going to work, where you lose money and purchasing power.

So we’ve got to, from my point of view, still stay invested. We have to understand that 2020 was a very bad year, huge shocks to the system. Huge shocks in the system that we’re still trying to kind of unwind and I believe in 2023 we will unwind these things. Do I believe that 2023 is going to be as bad as 2020? No, I do not. Will it be positive? I hope it will. Statistically, it has been. If we’re going to look back historically and statistically it will be a better year. But I don’t know. It is inherently an unknown because it’s about the future.

What we do want to do is make sure that we’ve got the right timeframe for our investments. If you’re going to need the money in the next year or two, you should be very low risk, okay. If on the other hand, you’re investing the money for three, five, ten, 20 years, I believe that you should continue with a good mix of equities and bonds going forward. It has served us well historically; I think it’s going to serve us well going forward as well. Even if 2022 – I think I keep saying 2020. I mean, 2022. Even if historically 2022 has been the exception to that, but let’s not say that just because it’s exception that it is the new norm. I just don’t believe it.

Michael Brady, (303) 747-6455. My information’s – my email is up on the screen. Call, email me. We can have a conversation at any time. Thank you. Have a great 2023.