“Set your course by the stars, not by the lights of every passing ship.” – Susan Blankston

The first quarter of 2023 has been marked by mixed financial market activity but has overall been a positive correction of the losses in 2022. The volatility and banking issues have further highlighted the importance of duration. Bad risk management on the bank’s part with incompatible duration led to issues as their long-term investments and short-term liabilities created a run on the bank. This serves as a good reminder to investors to assess their time-horizon and what the need for cash will be as they make decisions.

Let’s take a closer look at the first quarter of 2023 and what we’ve seen so far in relation to duration.

TRANSCRIPT

Mike Brady with Generosity Wealth Management, a comprehensive full service financial services firm headquartered here in Boulder, Colorado.

Before I jump into the first quarter review, many of you have asked how my knee surgery went. On March 1 I had a full knee replacement so good titanium in my knee now and it’s gone great. I have kind of a dull ache even a month later but I have to tell you that my flexibility is great, the pain never was very bad and if you’re ever looking for a great surgeon I love mine. It’s worked out well but I’m still in the rehab doing the PT and all of that. Thank you for all of your concern on my behalf.

Let’s talk about the first quarter. The first three quarters of 2022, a year ago, were absolutely horrible. The declines of 2022 really occurred in the first nine months of last year. The last quarter of last year when you look at the unmanaged stock and bond indexes was actually slightly positive. January of this year was highly positive which is great both for the unmanaged stock market indexes and for the bond indexes. February and March was really more static and sideways. We’ve got the fourth quarter of 2022 followed by the first quarter of 2023, both of them positive and starting to dig ourselves out of the horrible hole that the first three quarters of 2022 gave us.

I’m going to put up on the screen unmanaged bond indexes. You can see that last year was negative. So far this year it’s positive. When interest rates come down, bonds have a tendency to go up and the yields go down and stuff. I just want you to understand how that has an inverse relationship. What was so unique about 2022 is that not only did the unmanaged stock indexes go down, historically about one out of four years are negative, but bonds as well because of the incredibly quick rate with which the Fed increased the interest rates.

So far this year, 2023, things have eased up. The bond prices are increasing which is a good thing. I’m going to put this up on the screen and you can see how even the different durations from two years to 30 years, the prices have increased for this particular year, but they’re talking about slowing down the interest rates. The whole reason that the bonds took a huge hit last year, 2022, if it plays out in 2023 that actually will be to our advantage. Very unique last year both the unmanaged stocks and unmanaged bond indexes both went negative. So far they’re in recovery in 2023.

It’s important for us to remember that and I will also say that sentiment is not a very good indicator of what’s going to happen. When people are at their most positive, the next 12 months usually aren’t looking very good. When people are at their most negative and when they’re like well, I’ve just got wait for this to play out, is usually the next 12 months very, very positive.

I’m going to throw up a chart that shows something like that. Here we are and we’ve got two positive quarters in a row. I don’t know what the rest of the year is but I will tell you, I’m going to put up on the chart what they’re anticipating some of the interest rates amount to be from the Fed, and also some of the profitability going forward. It’s reasons to be positive, to dig ourselves out of it. Nobody knows what the future holds and that’s why duration – your time horizon is absolutely essential.

When we talk about the banks, some of the regional banks, let’s get the right lesson from them. They had bad risk management inside with incompatible durations. Investments were long term and their liabilities were short term and they had a run on the bank. It’s important for us as investors with our own portfolios to day hey, what’s my duration? What’s my need for cash? When will I need this? I might be in my 70s but hopefully I’m going to live another 20 years. So, making sure that the investments that I have are, of course, for the right duration for not running out of money for the rest of my life or moving towards retirement, whatever your specific goal might be.

Anyway, I’m always here to have these conversations with you and to ensure that what we’re doing on your behalf is consistent with what you want to do in your financial goals in your life.

Michael Brady, Generosity Wealth Management, 303-747-6455. Thank you.

“No one has ever become poor by giving.” — Anne Frank

2022 was a disaster. But January came in hot, making up a good chunk of any losses from the previous year in just one month. January was one of the best months in years for both the unmanaged stock market indexes and bond indexes. This is now the fourth month of a recovery. October, November, December and now January. The rest of the year is an unknown, only time will tell, but like we always say the best thing we can do is be patient.

Let’s take a closer look at what we’ve seen so far in our February 2023 financial market update.

Transcript

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered in Boulder, Colorado.

2022 was a disaster. Both stocks, the unmanaged stock market indexes, the unmanaged bond indexes down pretty sharply double digits, very unique that both of them went down at the same time. If you watch all my videos and newsletters from 2022, I deconstruct some of my thoughts about why that is with the supply chain issue which led to an interest rate issue with the reaction to that. We’ve got both fiscal, tons of money, money supply increasing so we’ve got some fiscal, we’ve got some monetary, we’ve got supply, all these things coming together.

I will tell you that January was one of the best months in years for both the unmanaged stock market indexes and bond indexes. As a matter of fact, you’re going to see this in a second. A good one-third to one-half of all that was lost in 2022 was made up in just one month which is January. I will tell you that this is now the fourth month of a recovery. October, November, December and now January. I don’t know what the rest of the year holds for us but I’m a broken record. I said three out of four years are negative. That means that sometimes there’s – sorry, three out of four years are positive, excuse me. Quite the opposite. Three out of four years are positive and one out of four are negative which means that we sometimes just have to be patient. The best thing that we can do is be patient.

Up on the screen there you’re going to see this is the unmanaged stock market index, the S&P 500 going back to 1980 and you’ll see that so far this year, this is the first week of February it is positive. You’ll see last year that arrow there that was last year. This next one up on the screen is the unmanaged bond index. Bonds went down last year in a reverse to the increasing interest rates and so far this year you can see that a good third of the decrease in the bonds has been made up already. You can see that right here. I’m going to put in a block there. Depending on the duration the length of a bond from short to long, you can see what the year-to-date return has been on a bond right there in that highlight.

This next screen I want to highlight the bottom right corner. Historical markets drawdown and the next 12 month rebound. You can see the tech bubble, the global financial in 2008, you’ve got COVID. After there’s been a decline, there’s been a great recovery in the next 12 months.

I don’t know if that’s what we’re in. I have no idea. The future is inherently unknown, but the way I like to think of it is you’ve got your Apple maps, you’ve got your Google or your Waze, whichever way that you get navigation to find someplace on your smart phone. You thought it was going to take you 30 minutes and you see that there’s an accident up ahead. It was unplanned, it’s unpleasant, you hate it. But you know what? The path that you’re on is still the right path. Doing anything else it’s so easy to want to get on a side road when really perhaps it’s really being sidetracked.

This next sheet up on the screen is showing – I’m going to put a circle around it which is inflation. Inflation in the last year or year-and-a-half was significant. It was the reaction to it that caused a lot of the bond decline over the last 12 to 18 months. What you’ll see is on this next chart that sharp increase all through the year of 2022 causes the bond market to go down. You’ll see the decrease that is expected from the Fed. We’re getting a handle on the inflation.

Let’s go back to that chart that I just showed, the previous one. You’ll see that on the right hand side inflation is starting to come down. It’s starting to creep back down which is wonderful. The reasons that bonds went down in 2022 and the last little bit of 2021 is the environment is reversing which is very, very good.

I could sit here and talk about other encouraging signs both from the economic forecasts and the stock market forecasts and the reaction to it, but I want to keep this one short. All I really have to say is the last month has started to negate some of the very long and painful quarter upon quarter, three quarters last year that were negative and one quarter that was positive. That one quarter that was positive was the last one and now going into this first quarter of 2023.

I’ll continue to do my newsletters and videos throughout the year. I’m going to try to do them a little bit more often as we really work to get to breakeven and then going back onto our original plan which, of course, is why would you have investments if you don’t believe that long term they’re going to be higher than they are today.

Mike Brady, Generosity Wealth Management, 303-747-6455. You have a great day. See you. Bye-bye.

Humility, like gratitude, is not so much a technique as it is a way of life.” – Ed Latimore

Tough 2022 Year,, which should remind us of the need for keeping the big picture in mind. While your goals may change, having a steady and reliable plan is crucial all year round.

In my latest video, I review the year in detail, and talk about what made 2022 such a horrible year. There is no sugar-coating it, practically every market sector lost money.

What does 2023 have in store for us? Is there anything to be optimistic about?

Watch the complete video to hear me talk about how one year does not a long-term plan make.

Transcript

Hi, there. Mike Brady with Generosity Wealth Management, a comprehensive full-service financial services firm headquartered right here in Boulder, Colorado.

Today is my 2022 Year-In-Review, and our 2023 Preview. I’m recording this on December 26. I want to do it even before the end of the year is over, because I want to get it out to you as quickly as possible.

What’s interesting about 2023 for me personally is this will be 32 years of doing wealth management, meeting with clients. There’s an old adage that says that history doesn’t repeat, but it certainly does rhyme. That’s one thing that I’ve noticed as I’m talking with people and watching TV is this inherent conflict between fear and greed.

As I mentioned, I’ve doing this for 32 years, so when I started it was the high-yield bonds were all the rage, and then from high-yield bonds it went into the mid-90s went to – well, gosh, you should be doing day trading yourself – it’s so easy and the tech bubble. That led to – after that, it was in the 2000s real estate and we had kind of the crisis in 2008. At that time, I remember a lot of people then ricocheting, you know, kind of going to the other extreme saying, no, gold is where things were in the 2010s, which then led to, well, no, I’ve now got to chase Cryptocurrency. “If you’re not doing Crypto, you’re kind of just old school.”

Well, you know what I’m hearing a lot on the news or as I’m talking with people is individual stocks. “No, we’ve got to do individual stocks or where we’re going to do these individual stock plays.” I stay firmly , even though the last year has been horrible. I do want to acknowledge; it has not been fun. I’m going to talk about that in just a few minutes, of having a broad-based, market-based investments that’s long term. And long term is multiple years, not one year. If you make long-term decisions based on short-term events, eventually that’s going to cause you to pinball from one investment strategy to another investment strategy and, unfortunately, there is no end to the number of people who will promise what you want to hear. I just don’t want to do that. I don’t think that you’re well served by trying to jump from strategy to strategy. I stick by the broad-based, market-based third-party management strategy because long term I believe that that’s been the best strategy for investors and best strategy for you as well.

Let’s talk about 2022.

Up on the screen, up on the left-hand side you’re going to see – on the bottom axis there, the X-axis is correlation to the Unmanaged Stock Market Index (S&P 500). The more to the left you are, the less correlated. That means that when it zigs, it zags, okay. If the – it actually does the opposite. So that’s why those U.S. Treasuries are there on the left-hand side over the last ten years. When the stock market’s gone up, it’s gone down. The other way around. There’s not much correlation to the Unmanaged Stock Market Index.

The same thing with Treasury Inflation-Protected Securities, which I’ve just circled. And U.S. Aggregates, which are bonds. So, bonds in general are a great thing to couple with some kind of an equity. This past year, that did not happen. We’re going to talk about it in just a second.

This next graph up on the screen is the last 30 years of the Unmanaged Stock Market Index (S&P 500). You’re going to see this year we gave away two years’ worth – about two years’ worth of growth. We’re back to where we were two years ago; it’s that simple. It’s not that you gave up ten years’ worth, or 20 years’ worth, no. We gave up a couple years’ worth. Not fun. Not trying to say that it’s good. We want to make money as many years as we can.

This next screen, I’ve just circled, kind of put a square around the box of last year. You’re going to see that whether it’s large-cap or small-cap, value or growth, it was negative almost double digits across the board. Very poor year for the Unmanaged Stock Market Indexes. When we look out to the box that I’ve now put to the left, over the last ten years, that’s the average rates of return. You can see that that’s why we have to look at the averages, the annualized numbers, not just one year. You cannot make decisions based on just one year. That is an amateurs way to go through your portfolio life.

On the next screen, you’re going to see 40 years. Forty years of the S&P 500. Three out of four years are positive, which are the numbers above the axis. One out of four are negative. I’ve just circled the ones in the last ten years; there were three negative years. This was the worst year of the last 12 years, since 2008. You’ll see that that’s not every year. You’ll also see that it has happened that there’s been three years negative before. That was 2000, 2001, and 2002. I certainly hope that’s not going to be the case this time, but it could be. But we’re going to talk about that in a second. Let’s not assume that every year is going to be negative. As a matter of fact, after those three years, significant number of positive years above the axis, even after those three negative years.

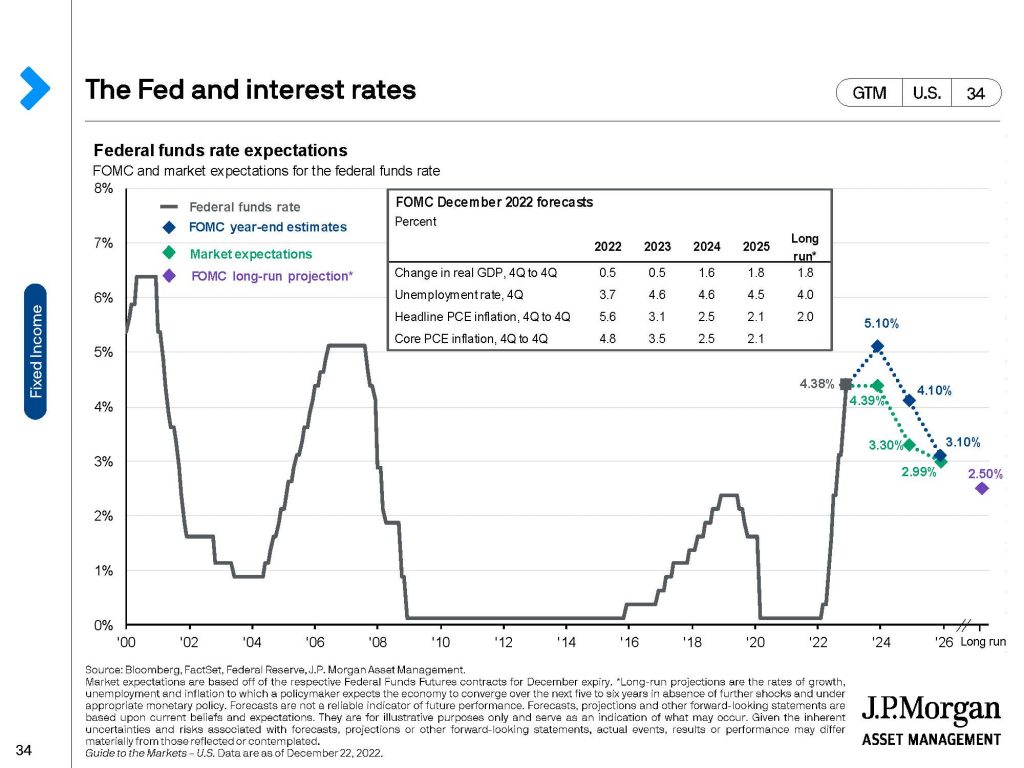

Why did some of this happen? This next chart shows the Federal Funds Rate, just what the Fed does. You’ll probably see this on TV, went from practically zero up to 4.38 percent. Significant. Look at how sharp it changed in one year. One year. That’s really dramatic.

As we go, and I’ve just circled it. Some projections going forward over the next year or two, projections that will maybe go a little bit higher, possible. It depends on how the economy plays out or stays and goes down negative. Alright. But a very sharp correction in 2022. One of the two or three main factors for the poor performance that we had in 2022 was the dramatic reaction by the Fed to some underlying fiscal policies, a significant amount of money that was thrown out into the world and supply problems.

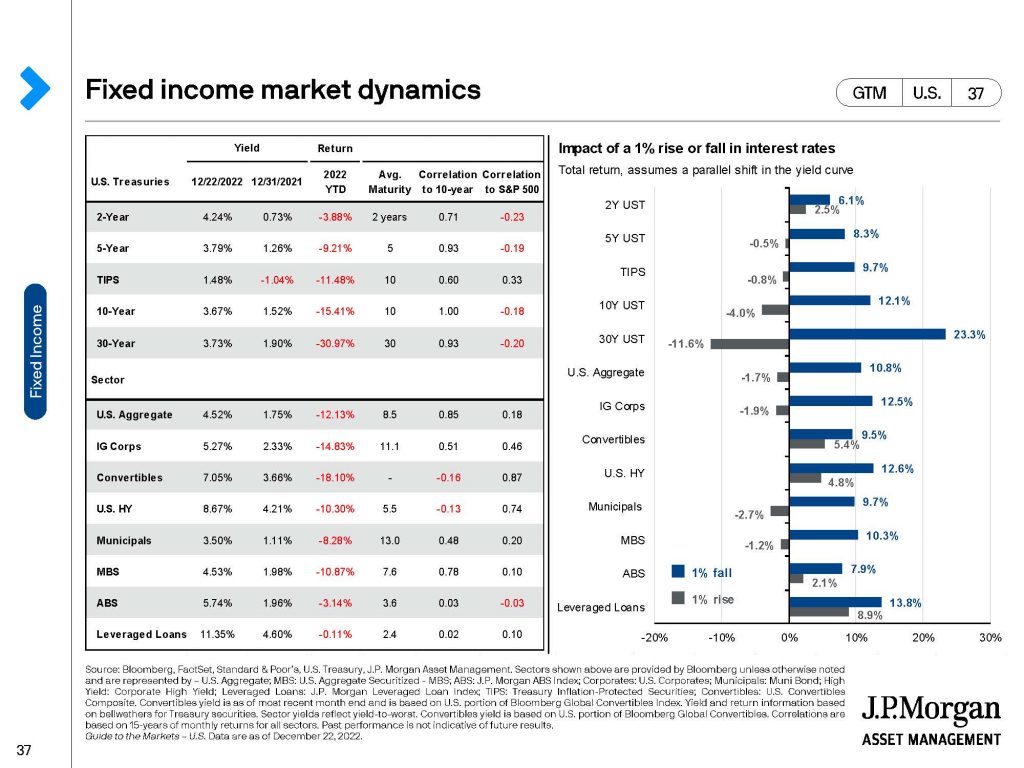

The next page, up on the screen, Fixed Income. These are bonds; these are Unmanaged Bond Indexes. You’re going to see this year, 2022, across the board, whether it was short, which is that top number there, all the way down to long-term bonds double digit declines. This is the first time in over 50 years where bonds and stocks have both gone down over ten percent. First time in 50 years.

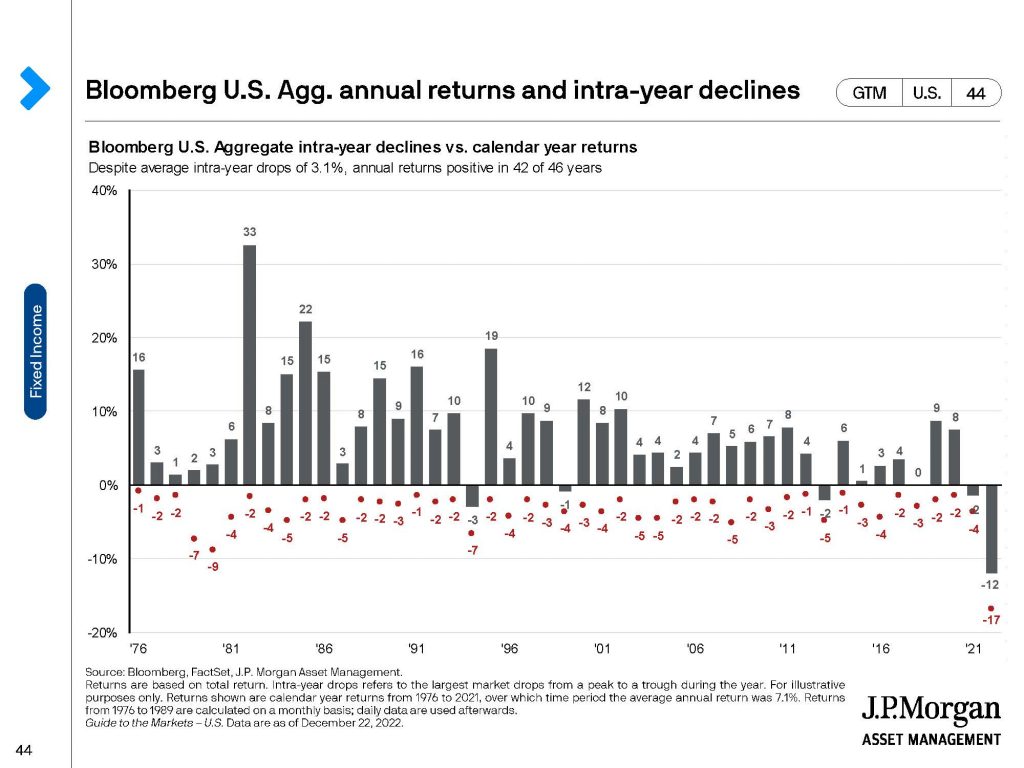

This is it for the last 30, 40 years. Forty years. You’re going to see that the vast majority of the year, above the X-axis for the Aggregate Bond Market, Unmanaged Bond Market is positive. This year it is not. That’s the exception, not the norm. We’re talking the late 70s as well. We’re talking years where inflation was significantly higher than even where it is right now.

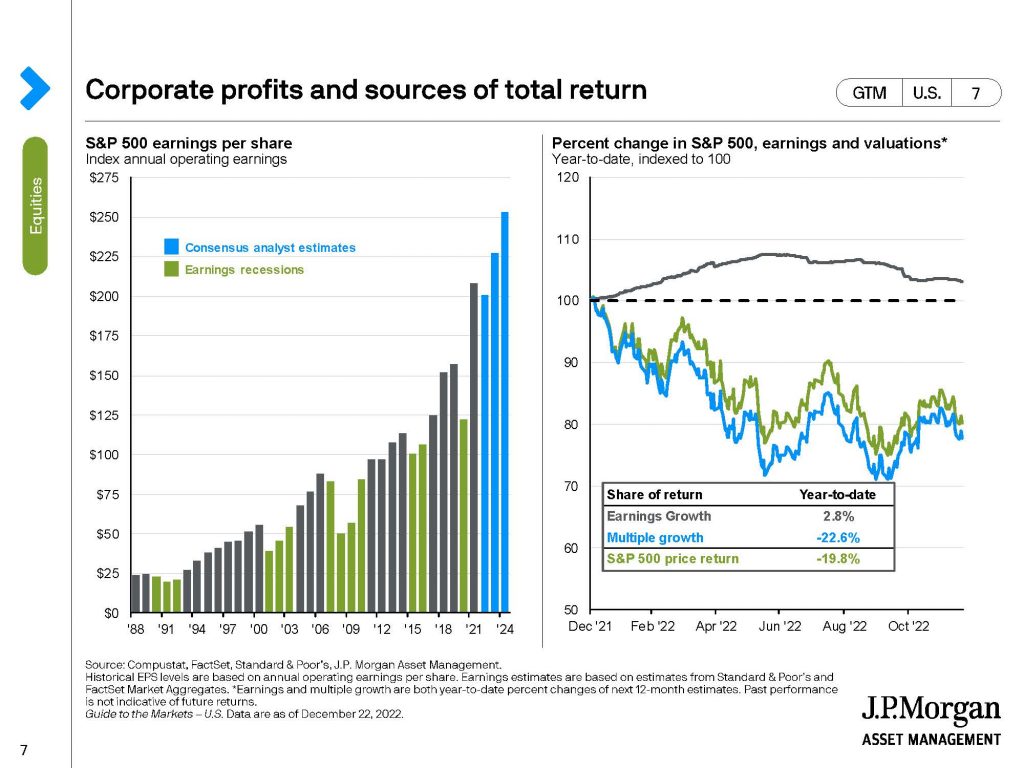

The next page, let’s talk a little bit about going forward. You’ve got the blue that I’ve just circled there is Consensus Analyst Estimates for Earnings Per Share (EPS). Yes, the S&P 500 Stocks on average in Aggregate have been beaten up. Some prices gone down, but the earnings are looking real good.

Right now, in the last two, three months, you’ve heard a significant amount of belt tightening with companies as they’re trying to be more efficient, trying to decide what the next year or two – a high probability that we might be in a recession, going forward for some time. But from a portfolio point of view, we want to be in a market that is perhaps underbought, oversold and that is still one of the things that we’re watching, that I’m watching.

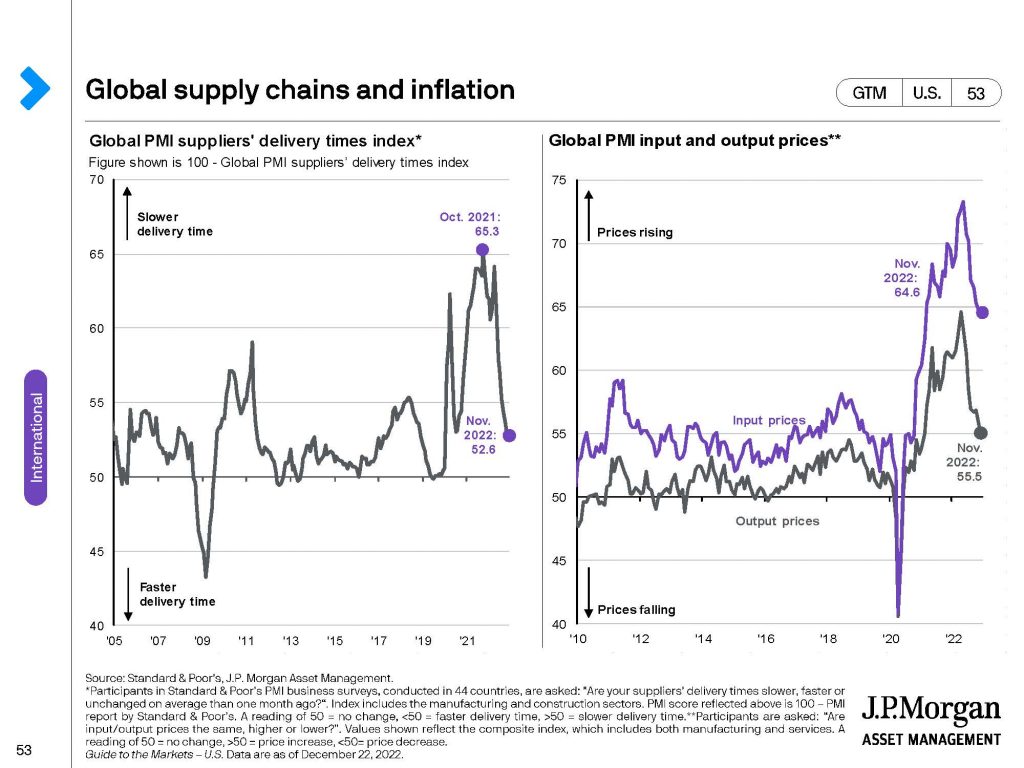

You’re going to see here on the next screen, Global Supply Chains. Great. We’ve gotten through. That’s good that it’s gone down; that’s the thing that I just circled. It has decreased the time to get supplies to us. Is China continuing to be a problem? Yes. That whole Zero-COVID measures, not very helpful. To them or to the global supply chain. As we’re re-entering kind of a new normalcy, as they have basically changed that policy, this is a good thing. The geopolitical going forward, our relationship with China, both the United States and the world will play out in a significant manner over the next couple of years.

Kind of a last thing that I want to talk about from a chart point of view is that far right-hand side CDs – 6-month CD rate still relatively low on average the 2020 so far. The inflation is much higher than that. So, just keeping your money in Money Markets and CDs just isn’t going to work, where you lose money and purchasing power.

So we’ve got to, from my point of view, still stay invested. We have to understand that 2020 was a very bad year, huge shocks to the system. Huge shocks in the system that we’re still trying to kind of unwind and I believe in 2023 we will unwind these things. Do I believe that 2023 is going to be as bad as 2020? No, I do not. Will it be positive? I hope it will. Statistically, it has been. If we’re going to look back historically and statistically it will be a better year. But I don’t know. It is inherently an unknown because it’s about the future.

What we do want to do is make sure that we’ve got the right timeframe for our investments. If you’re going to need the money in the next year or two, you should be very low risk, okay. If on the other hand, you’re investing the money for three, five, ten, 20 years, I believe that you should continue with a good mix of equities and bonds going forward. It has served us well historically; I think it’s going to serve us well going forward as well. Even if 2022 – I think I keep saying 2020. I mean, 2022. Even if historically 2022 has been the exception to that, but let’s not say that just because it’s exception that it is the new norm. I just don’t believe it.

Michael Brady, (303) 747-6455. My information’s – my email is up on the screen. Call, email me. We can have a conversation at any time. Thank you. Have a great 2023.

“Life can only be understood backwards; but it must be lived forwards.” ― Søren Kierkegaard

The financial market landscape has been more than rocky lately, but how did we get here? There are always reasons to be pessimistic, just the same as there are always reasons to be optimistic. Looking back a couple of years we are going to assess supply and demand, inflation, real estate investment, stocks, bonds and the overarching US fiscal policy. We will highlight the trends seen from some pretty historical moments experienced between 2019-2022. We don’t know what the future holds. Even the best data from the past cannot predict what is about to happen, so save any prognostication and stay focused on your horizon. The market will go up and down with current events, the best we can all do is stay focused on the big picture and our long-term goals to make the best decisions for ourselves.

Transcript

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered in Boulder, Colorado.

Today I want to talk a little bit more technical than usual. I want to talk about how did we get to where we are right now–the present. What’s happened over the last couple of years? What has transpired? In order to get us now to the present it’s so clear to us. That’s what it feels like. Hindsight is 20/20, but now what does this mean for us going forward, and there are reasons to be both optimistic and pessimistic. It could go either way so let’s figure out where we are and what led us to where we are now.

By the way, let me just tell you that it is complex. The United States is the largest economy in the world. About $22 trillion. The next closest to us is China which is in zero COVID tolerance. They’re closed down. And then after that it’s the eurozone and then everybody else is distant fourth, fifth and all the way down. The big behemoth is the United States and we are the reserve currency for the world because of our size. Many countries decide to peg many of their decisions to the U.S. currency but just by the fact that through the trade balance everyone’s got a lot of dollars. We’re buying things. And so we are the reserve currency. What we do matters in the world. But geopolitical issues are also important.

Let’s start talking about how some of these factors came together. About two years ago we’re starting to get out of COVID. We have supply chain issues, reduces of supply and demand. People are now getting out of their homes, they want to drive again, they want to go on vacation, they want to travel. Demand is high. So, right now we have an imbalance. We have high demand, we have low supply. That right there is a problem.

At the same time we’ve got some cash being thrown around. We’ve got some fiscal policy that over ten years the Congressional budget office has said that it will cost $4 trillion. It might have been well intentioned. It doesn’t matter. We’ve got lots of cash, lots of liquidity and people had saved a significant amount. When we look at the savings rates during COVID while everybody was stuck in their house, people now have cash. More and more people with more and more cash chasing less and less things. And, of course, if you want it then you bid up the price. That’s how inflation starts.

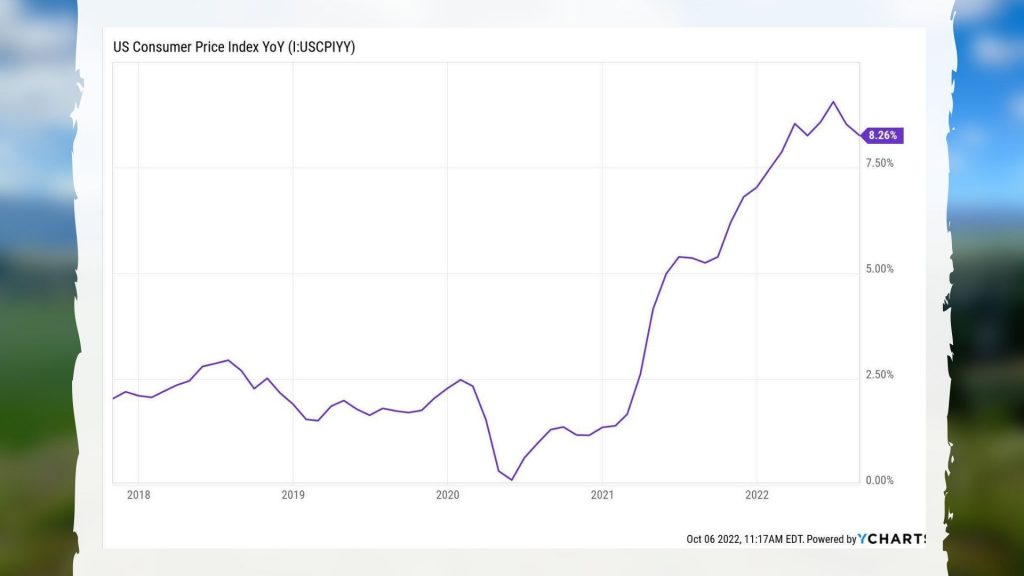

Inflation happened. I’m going to put up on the screen there and you’re going to see how it went from about 1% at the beginning of 2021 all the way up to almost 7.5% in one year. That is huge. During all that time we kept being told well, this is transitory and this is going to be temporary, et cetera. It continued up and up and up.

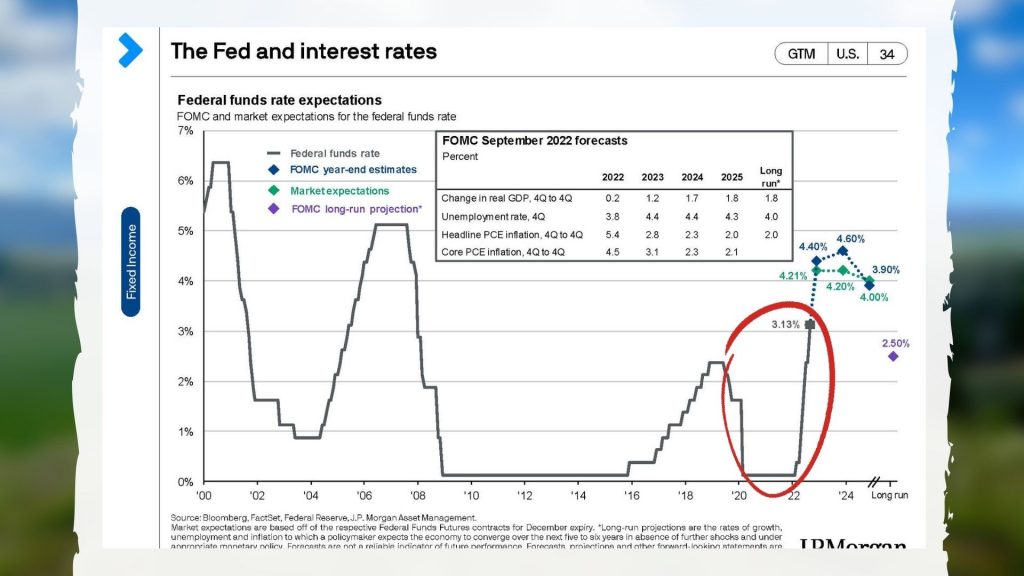

Now, one of the problems is as you can see here on the second sheet – and I’m going to circle when the Fed started to increase interest rates. Increasing interest rates slows down the economy. It starts to take money out of the money supply. They didn’t start until the beginning of 2022.

Let’s imagine that you have a picture up on the wall. You can take a hammer and you can real gently nudge it, nudge it, nudge it until it’s straight, or you can take a huge whack and things are going to break. Well, essentially for an entire year the Fed did nothing and now they’re trying to make up for it by whacking it. Not nudge, nudge, nudge. They’re whacking it and that’s what has happened in 2022.

What is interesting is 2021 the stock market and unmanaged stock market indexes continued to go up even though the inflation rate was going up as well. Anyone who says that they said they completely called it that it was going to go up as much as this is really fooling you. Yes, there were some indications it was going to go up, but almost every single expert was surprised by how much inflation has gone up. Now the Fed is trying to make up for it.

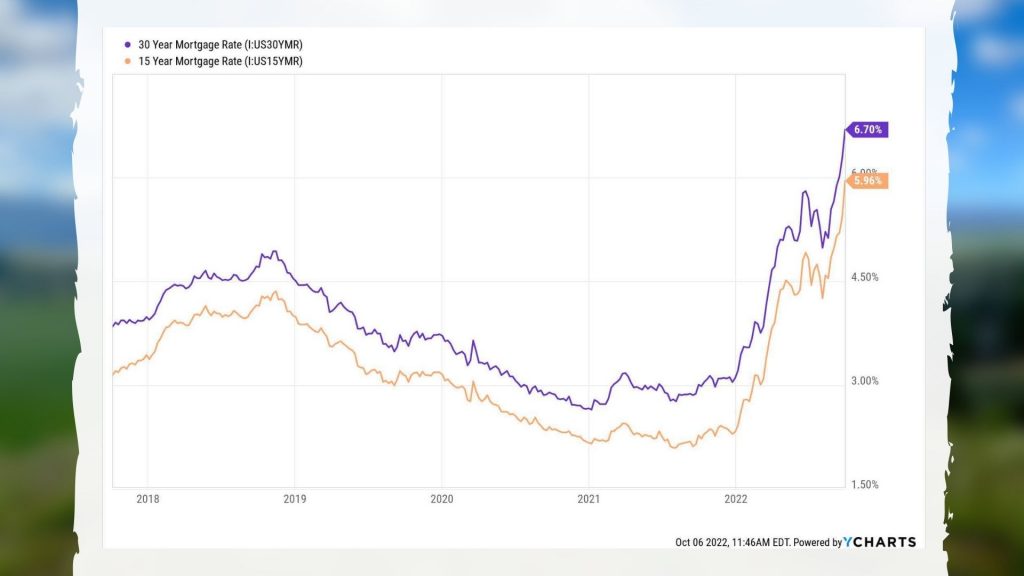

Now up on the screen I have put the huge increase in both – the top line is a 30 year mortgage which is now as of the beginning of October at 6.7% and almost 6% so 5.96% on the 15 year. That in my opinion puts a screeching halt on a lot of the transactions in the real estate market. We’ve had a huge increase in housing prices when interest rates get higher, when someone wants to buy a house they might second guess it. This is something that I think we need to really watch out for as the unprecedented, really unbelievably sharp increase by the Fed in their monetary policy is putting the brakes on the economy big time. The odds of a recession is going up very high.

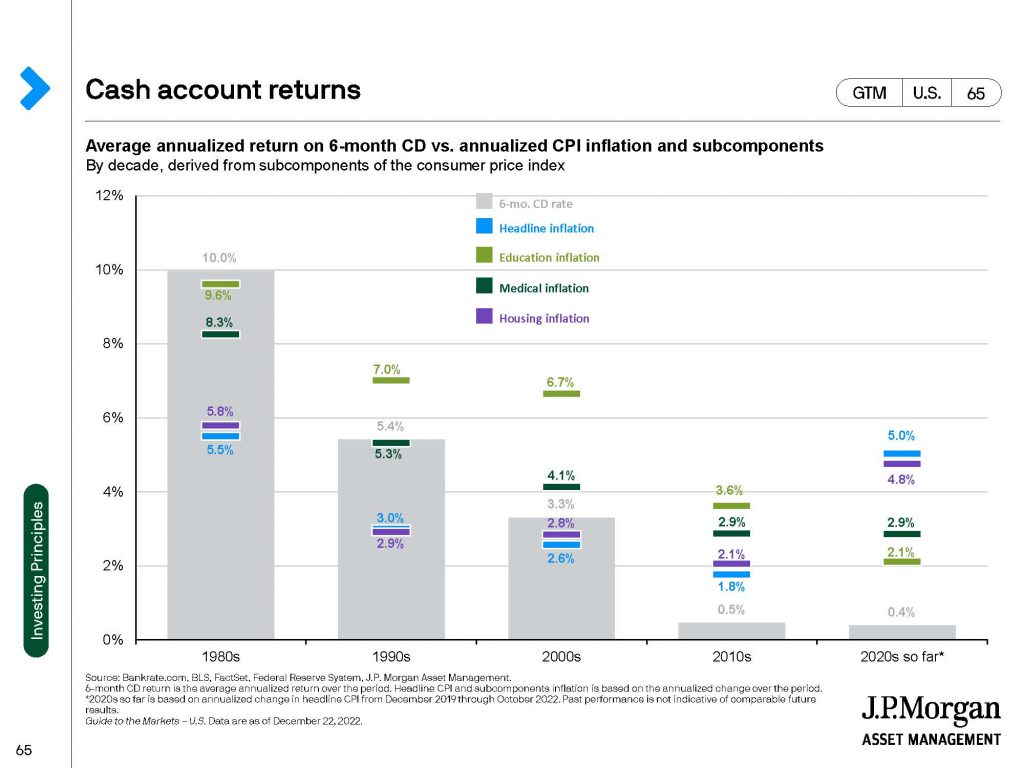

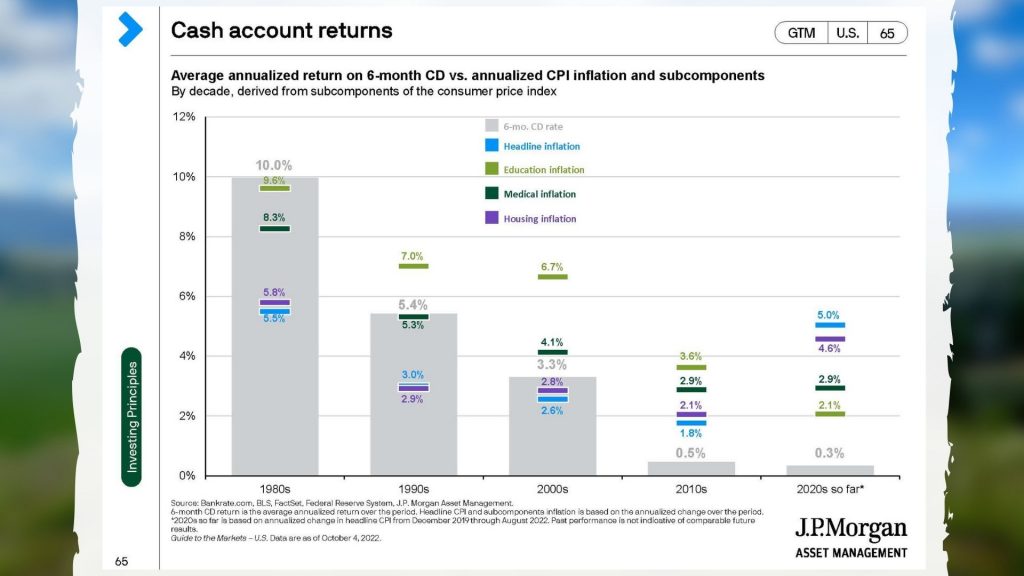

When we look at cash, look up here on the screen. There’s a lot going on here in this chart, but on the left hand side the CD rate for the average of the 1980s was 10%, but the inflation was about 5.5% on average. In the 2000s you had your CD rates of about 3.3% on average and inflation was less than that. The headline inflation was less than that. In the 2010s and in so far right now inflation is significantly higher than what you’re getting in CDs for a six month rate. Cash really is a great place not to lose money. It’s not really a great place to make money from a purchasing point of view. Bonds as well. It’s a complicated situation but bonds have had one of their worst years ever in decades this year because of the incredibly sharp increase in the Fed Fund Rate from the Fed.

Right here on this chart is the S&P 500 when we look at it standing back with multiple years. You’re going to see that in the last year or so we’ve given up a couple of years’ worth of growth. Very irritating, especially if you’re withdrawing money. That being said the upward trend has always been over many years upwardly mobile. You’ve heard me say this before in about three out of four years our positive one year is negative. This has a tendency to be the negative year and it’s an unpleasant. Every quarter this year has been negative.

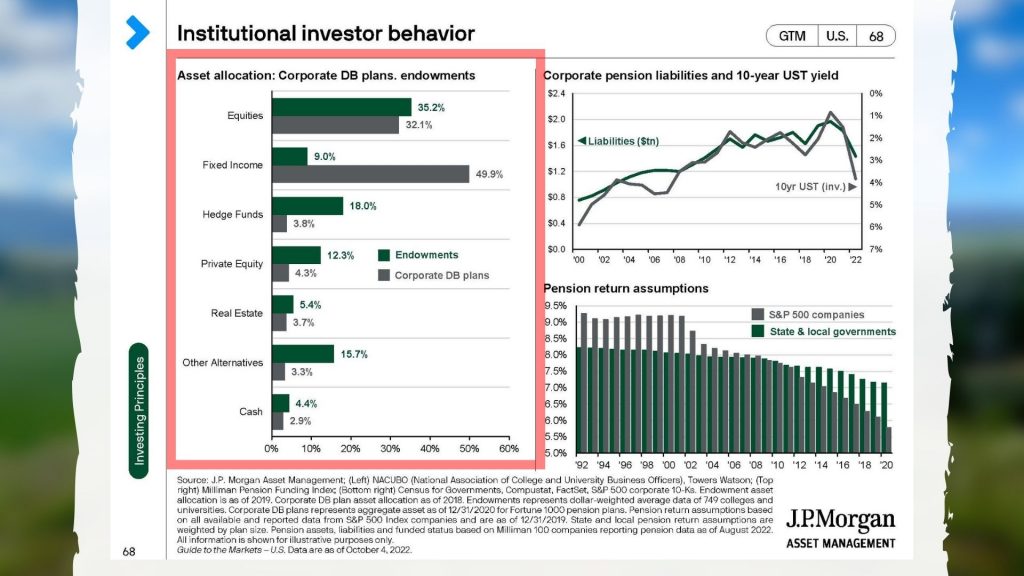

What are investors doing? I’m just going to put up here on the screen there corporate defined benefit plans, endowments, university endowments, et cetera. We have a tendency to put money into fixed income. They do equities, they do fixed incomes as well. A lot of private equity, some alternatives. What I recommend for clients in general is very similar to what some of the biggest endowments at colleges and at universities do in defined benefit plans.

Some reasons to be optimistic. The more things go down, the more they go up. That’s the thing. We could absolutely six months from now, a year from now be lower than what we are right now. We’re going to talk a little bit about the reasons why that might be. When we look out one year, two years, three years, five years the odds historically have always come in our favor that when things go down they come back up. When things go up, at some point they’re going to turn around and we always forget that. We have to understand that it’s both ups and downs.

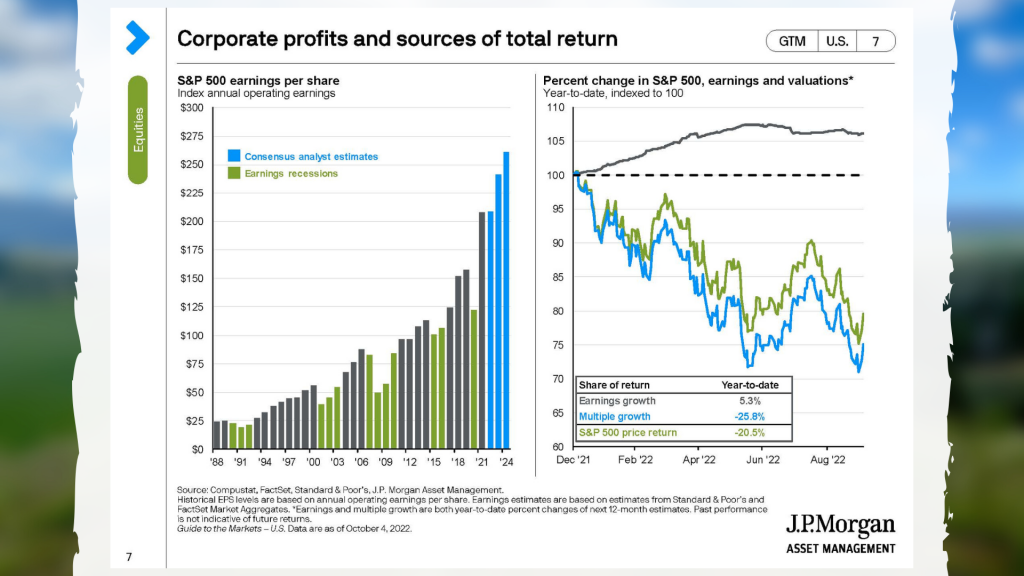

Up on the screen on the left hand side you’re going to see the consensus analyst estimates for S&P 500 earnings per share. The companies are still profitable. It’s that simple. Yes, some of them are laying off workers. We’ve had an unbelievably low unemployment rate and it’s been coming down over the last two years to historic lows again. As a matte of fact, we’ve been talking about the great resignation where people don’t want to go to work. Well, some of those people who have jobs are being let go in order to increase the earnings per share and they maintain it with some belt tightening. As an investor this is good for us. This is very good for us.

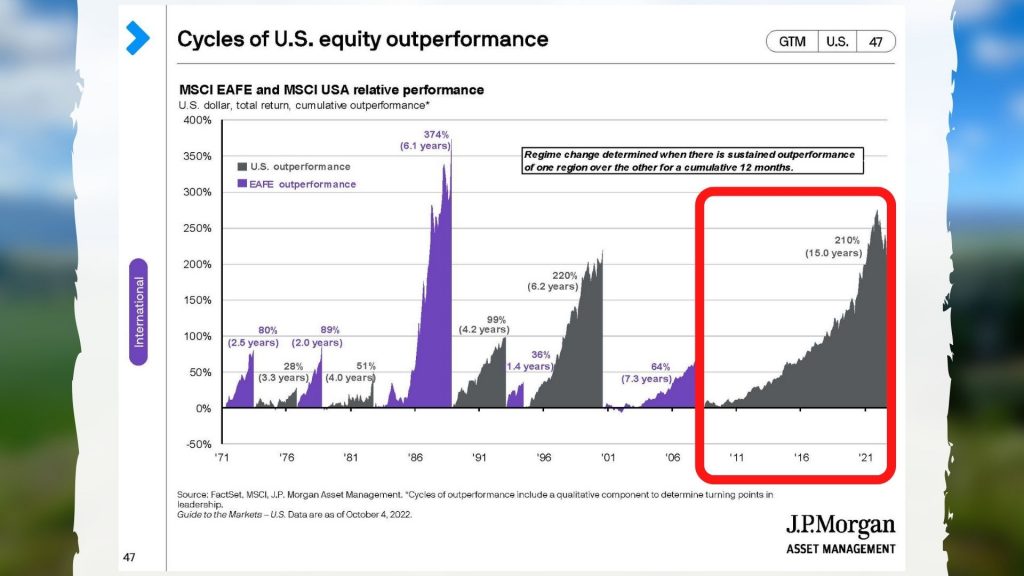

Here on the next screen you’re going to see the cycles of U.S. equity performance, and I’ve just circled right there. For the last 15 years the United States from an unmanaged stock market index has outperformed most of the world. There’s one index, the EAFE, and so we’ve outperformed that for the last 15 years. In my opinion that’s going to continue. When we look at all the different places that we can invest, the United States is the best horse in the glue factory here. Europe has made some unwise, in my opinion, decisions from a fiscal point of view. Germany in particular is in a world of hurt. Their whole business model is based on selling stuff to China with cheap energy and neither of them are really working. They’ve really got to rethink things in much of Europe. This is going to be a tough winter and the energy prices not only for the end consumer but also for all of their industrial base. They’re in a world of hurt.

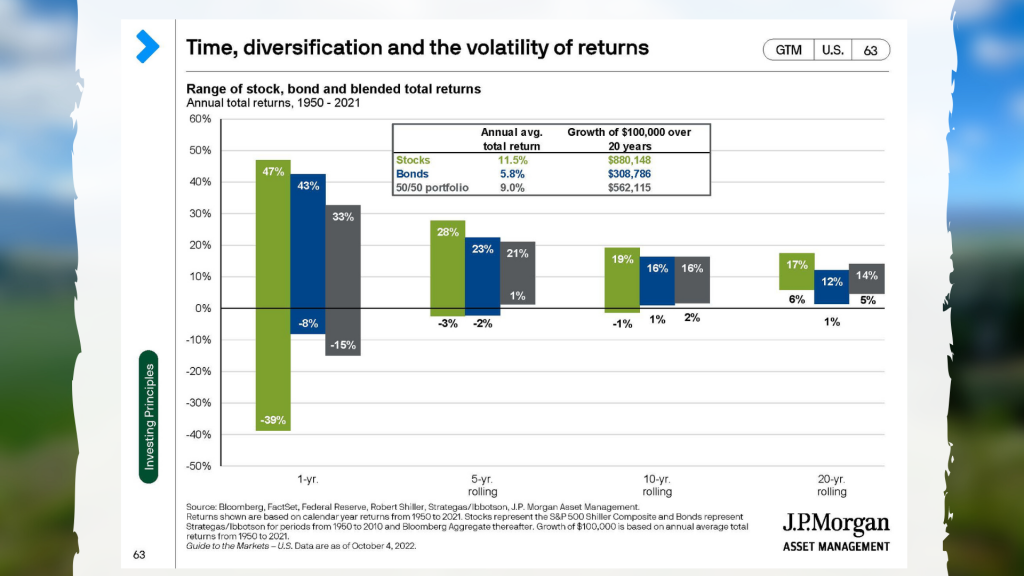

Let’s look up here on the screen. Let’s pretend like we don’t know what the future holds which, of course, we don’t. Historically going back 70 years there’s actually never been, the sixth bar over there, the one that says 21 and 1. Over a five year time horizon if you’ve got a diversified portfolio that includes some of the unmanaged bonds that we’re talking about right now, you actually never lost money over a five year time horizon and you’ve done as well as 21% per year. And so that’s the range when we look back over a 70 year time horizon.

You can see the first three bars on the left hand side, a huge range for the equity which is that left bar. A huge range for the bonds. You put them together and it’s a slightly lower range, but it really starts to play out – and this is the way we put portfolios together when we’re looking at 5, 10 and 20 years.

For people who are retired hey, let’s look at that five year. I’m hoping you’re not going to die in the next year or two. It could happen. We could die tomorrow. None of us know when we’re going to die, but we do want to keep the timeframe in consideration, and always know that that there’s good years and there are bad years. Good years are not necessarily followed by bad and bad is not necessarily followed by good. We’ve got a good, strong S&P earnings outlook. We have pessimism at an all time low frankly. I mean it’s very low. It hasn’t been this low since 2008, and 2008 was followed by an incredible rally that lasted many, many years. I happen to be a contrarian at heart. I believe that our emotions and our actions are messing with the portfolio has a tendency to do us more harm than good. You’ve heard me say many a time on these videos and in my newsletters that if you pick the aggressive level that you can stick with, but you don’t bail on. You might not be happy year to year, but over a five and ten year time horizon historically and what I believe your return is going to be that as volatility goes up and so does the return as time goes on. That’s why you create something and you sit back and you try not to tinker with it too much even though we’re always watching within the portfolio hey, maybe we need to increase our equity allocation, our bond allocation, our cash allocation, et cetera, within the portfolio. That’s one of the reasons why I believe in good, third-party management. We’ve got great people working really hard in a tough volatile situation.

That’s what’s led us to where we are. There have been some fiscal issues. There have been some major policy issues on the Fed side. They have said that they’re going to continue to increase rates. At some point that is going to stop and that’s going to be very good for the markets when they stop. And even when their expected increases have already been priced into the market is also good for the markets. And then we just have this supply chain problem which is getting better. It is actually getting better although it was very bad earlier in the year and at the end of 2021.

Those are some of my thoughts. Give me a call if you’d like to talk about them further. 303-747-6455. You have a wonderful day. Thanks. See you. Bye.

“A bend in the road is not the end of the road… unless you fail to make the turn.” – Helen Keller

There’s no way to sugar coat it- this has been a tough year. This quarter especially has not been good. July was positive but then what it gained in July, it gave up in August and September. These things happen sometimes.

Let’s take a look at what we’ve seen the past couple of months and what we can do to stay positive as we move through the end of the year.

Transcript

Hi, there. Mike Brady with Generosity Wealth Management, a comprehensive full service firm here in in Boulder, Colorado.

This has been a tough year. I’m not going to lie to you. This quarter has not been good. July was positive but then what it gained in July it gave up in August and September. I’m recording this on September 18 so I’m not quite sure what the last week-and-a-half to two weeks of September are going to bring, but it’s been a really tough quarter. It’s been a very tough year. These things happen sometimes.

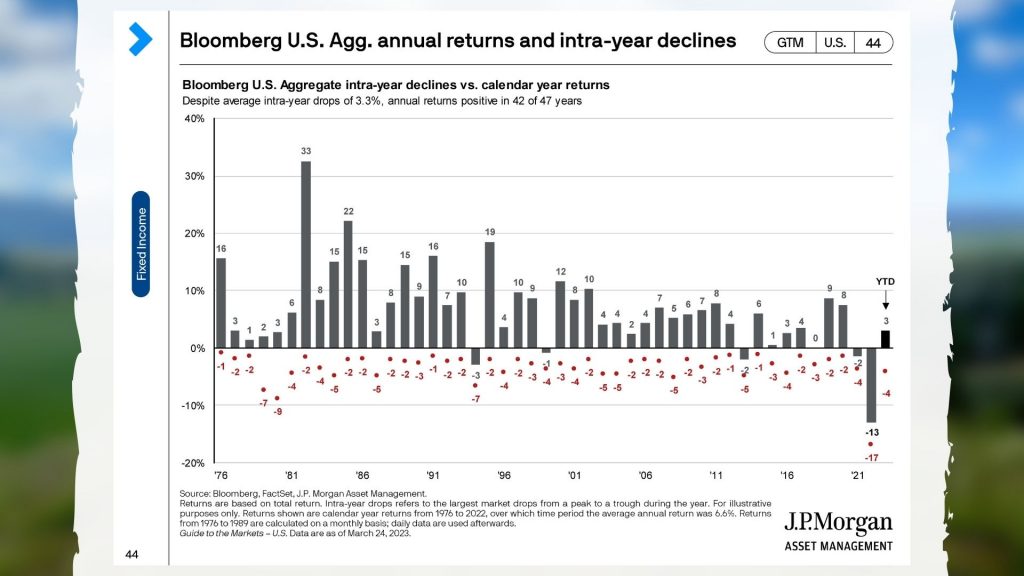

Up on the screen you’re going to see the multiple year graph and I have now circled the decline that we have seen this year where we have given up in the last nine months or so what we gained in a year-and-a-half. No, we didn’t give up the entire stock market. We gave up what we earned in the last year-and-a-half in general with the unmanaged stock market indexes. Sometimes that happens. It stinks absolutely every time. If you look up on the screen I’ve done another chart. Those that are on the bottom are the intra-year declines. The black numbers or the dark numbers are what the year ended. You’ll see that the last three years were positive even though they had during the year some negatives. This year it’s been negative. It was worse negative but now it is still negative. Three out of four years as we go back 30-40 years historically have been positive and one out of four is negative. Every single time it happens it stinks. It’s all right to have some emotion about it. The question which we’ll talk about here in a little bit is what you do with that emotion. Having the emotion is fine, doing something with it that is detrimental to your long term is quite another matter.

Up on the screen is another chart which shows even bonds this year are negative. I’m putting a little red box around that third column over. If you had 30 year guaranteed government bonds, you’re down almost 30% so far this year. You know that by the time they mature it will be back and it will recover all of that. But even bonds this year – stocks are down and bonds are down. If you just have your money in a money market, if you have it in your mattress, due to inflation you’re also losing money. Inflation is one of the big drivers which we’re gong to talk about here in just a second.

On this graph right here up on the screen on the left hand side you’re going to see what the stock market does, does not necessarily correlate directly with what the economy is doing. However, they definitely walk hand-in-hand even if it’s not perfectly. You’re going to see there on the left hand side that expansions in the economy average 47 months – 47 months. That’s about four years and recessions are about 14 months on average, so that’s about a year. Getting back to that whole discussion I had just a few minutes ago, three out of four are positive and one out of four is negative. Those are odds that I’m willing to go to invest in going forward. The future is always uncertain. However, we’re going back decades and decades in a diversified portfolio, especially of unmanaged stock market indexes.

I said I was going to talk about inflation. Look at that chart right there. I have now circled what has happened in the last year-and-a-half. Inflation is the big driver from my point of view. Now, why do we have some inflation? This is a tricky one. We’ve got a supply problem and we’ve got a monetary problem. Step back for just a second. When people talk about fiscal policy that’s what the U.S. government does. Monetary policy is what the Fed does. The supply is global, whether you’re able to get your circuit board or various materials that people want. If we just had a supply problem then if there was a finite, if there were ten widgets, ten things, and a lot of people wanted those ten things they would bid the price up. It was very important to complete your car or your particular manufactured goods. However, in this case we’ve thrown some gas onto the fire here. We have flooded through fiscal policy, eve if it was well intentioned, we have flooded the market with lots of cash at the same time we have restricted supply which is a problem. This then causes the Fed to want to take money out of the market and they do that by raising the interest rate.

You’ve got all these competing forces. It’s going to take a little while for it to settle down. This has been a huge shock to the system over the last couple of years. This is pretty unique. It’s not pleasant. In my opinion there were some things that we could have done differently. Maybe that’s in hindsight given the benefit of the doubt, but there have been some missteps here and now we are correcting that.

When we look back at various crises in the past and various declines there’s usually some reason. It seems only so obvious after the fact whether it’s the tech bubble, whether or not it’s a housing crises which I would argue was really a cash and a credit crunch back there in 2008. Right now we have a money supply issue and a global supply mess getting materials to the proper manufacturers. Having unpleasant emotions around it is normal. We are human beings for goodness sake. The question is do you do something short term when you really have long term plans? The answer should be no. We have long term plans and so we can’t let short term data dictate those long term plans.

It’s interesting that the market went sharply down but came back relatively quickly. That’s like ripping the bandaid off very quickly – boom. However, this is a ripping off of the bandaid very slowly. It is being dragged out over months, over some quarters. All I can really say is that 100 percent of the time going back 100 years, it has recovered if you are in a diversified portfolio. I expect this to be the same so I’m not worried except to the degree that I want it back as quickly as possible. Let’s not kid each other. That’s more fun. When it is down, everything is down, pretty much everything is down both in the U.S., internationally, stocks, bonds. We’ve got to figure out this mess. The best thing for us to do is always keep our eye on that long term and stay cool as cucumbers.

Mike Brady, 303-747-6455. Have a great day. Let’s hope that this next quarter is a good quarter and that we end up the year a little bit better than we are right now. Have a great day. Bye-bye.

“Last week I found myself wondering why I don’t buy more piñatas, because right now I’d love to beat the holy crap out of something and then sit in the grass and eat candy.”- Susan Blankston

When you listen to newscasters talk about the financial markets, volatility is often explained away in a very linear and simplistic manner. Even if their explanation contradicts itself from one day to the next, they do what they can to pinpoint one reason for the ups and downs. What’s often left out is the range of emotions that have also come into play – hopes, fears, greed, and more that also get mixed into the elements.

Over the last couple of years we have seen an off kilter supply and demand – with demand greatly outweighing supply in many areas. We’ve seen shock waves of disruption as the markets responded to Covid, the war in Ukraine, and more. As the gap narrows a bit now, let’s take a closer look at what we’re seeing and what it means for investors.

Transcript

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive, full-service firm here in Boulder, Colorado.

Today I wanted to talk a little bit about the volatility in the market. You might read or watch on TV that it’s up one day because of X and it’s down the next day because of Y, and the journalists seem to be very confident that the reason that they’ve given for a complex question is absolutely right despite the fact that the day before might have been contradictory. They’re optimistic on day one and pessimistic on day two and then optimistic and renewed on day three. It really doesn’t make a lot of sense many times.

When I was in college we learned about this thing called CAPM which is the capital asset pricing model. A guy by the name of Markowitz came up with that, a brilliant economist. He actually received a Nobel Prize in economics in the early 1990s because of it. His work was followed up by the work from a guy by the name of Kahneman and work by the name of Thaler, T-H-A-L-E-R, Thaler. They received Nobel Prizes 20 years ago and another one about five years ago. What they determined is that unlike what I learned in college and what Markowitz had said is it’s not all about math. The reason why the value of an asset – in this case it could be the stock market, the bond market – it’s not all mathematics. It’s not just a stream of income payments in the future and the entire formula. It’s an efficient market meaning everyone’s got the available information and not everyone, though, is logical. That’s really the biggest work that came out of the last 20 to 25 years is that go figure, people sometimes are emotional and are illogical.

So, I take that into consideration when I look at what’s happening right now. A lot of it has to do with some of the emotions that we have, some of our predictions, some of our fears, some of our hopes, some of our greed, some of our real fear. And that all boils together in a pot to get what we see on a daily basis and then is in the news.

Over the last two-and-a-half years we’ve had on the demand side. It’s a demand and supply, but on the demand side we’ve had $7 trillion helping to support the demand for goods. Whereas, on the flip side the supply has been restricted. We’ve had supply chain issues. You have lots of demand, lots of money with lower supply. It hasn’t been transitory. The impact of that is being inflation and it’s been exacerbated by various shocks to the system. COVID waves that have led to one right after another. Then we’ve got Ukraine being invaded by Russia. There’s a reason why it’s been this inequality of demand and supply and out of whack has been extended longer than what is frankly comfortable.

What we’ve seen recently is we have the supply chain, there’s an agreed upon consensus throughout the world that we need to focus on getting that fluid again. On the flip side, demand is coming down mainly because of the inflation, the reaction to it. What I would say is the overreaction. The oversold we talked about. So, interest rates are coming down because the real estate, really with mortgage rates dramatically increasing to 40 year highs for mortgage rates, people are buying less houses and so the demand throughout the entire economy has reduced due to some of the inflationary pressures that we’ve seen. But at the same time we’re seeing the supplies go up and so they’re going to be back. Hopefully we’ve got some demand and supply coming back into equilibrium which is what we want to see and that’s good for us. Good for us as investors. Of course good for us as long-term investors as well as things start to settle down.

I always hate it when there’s a volatility. I never mind it on the upside. You get two or three days of an upside and you’re like, “Yeah, right. Things are back.” And then we have a day or two of downs. The important thing is as we stream them together that there are more ups than downs and that starts to happen when things go back into equilibrium. It takes a while for it to happen. I would say that it took a while for it to come to this situation. It’s possible – sorry guys, that’s my dog right here underneath the table – it takes a little while for it to work itself out as well. The risk to us is if there is a shock, especially to the supply side. On the demand side printing more money doesn’t seem politically feasible at this point in time. However, from a supply side if we have a major shock to the supply side that won’t be good. That will derail us from coming back into equilibrium which is what we want for that demand and supply side.

Anyway, Mike Brady, Generosity Wealth Management, 303-747-6455. You have a wonderful day. Thank you.