“Being rich is having money; being wealthy is having time.” –Margaret Bonnano

It is important to take a macro versus micro approach to investments, meaning we have to take a very big, long-term view in order to start to make some sense of the stock market. There are many variables in this equation that we call the market and only by looking at it as we would approach a mosaic by looking back months and even multiple years does it start to make sense.

Listen for more on how to keep perspective when looking at the market.

Watch my short video or read the transcript below.

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered right here in Boulder, Colorado.

Today I want to talk about making sense of things. I was meeting with a client a week or two ago and he said Mike, it doesn’t make any sense in the stock market. It’s something that I don’t understand. It goes up high one day and down the next day for a reason that I can’t understand. And my answer to him was stop trying to understand it. Stop trying to understand it on a daily basis, a weekly basis, even a monthly basis because I don’t know the future, you don’t know the future and for us to try to guess the emotions, the intents, the actions of millions of other people is very difficult.

We have to take a very big, long-term view in order to start to make some sense of the stock market. If we’re looking at it from a daily basis, one day if you listen to the newscasters or read some article they always have some reason why it went up like they know definitively what millions of people are thinking. The next day it might completely reverse and then they give a different answer that might be very similar. No, not that many people change from day to day. There are many variables in this equation that we call the market and only by looking at it as we would approach a mosaic by looking back months and even multiple years does it start to make sense.

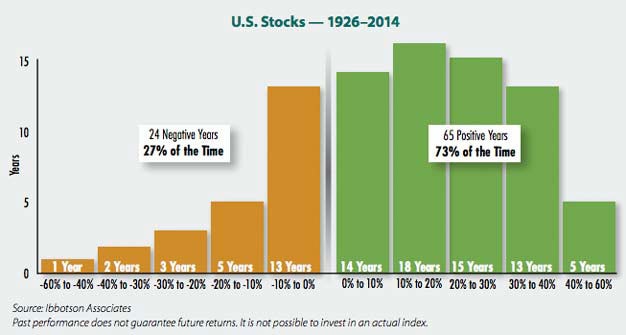

So you have to look at yourself and your own emotions and say wow, am I going to allow myself to be whipsawed from day to day, from week to week, or am I going to take the long-term view. And your bias is very important to know. If you’re a naturally optimistic person I would argue that history has shown you to be a winner in this because three out of four years going back to 1929 the market has been positive. One out of four years have been negative. That doesn’t mean the future is going to be that way. All I can really say is that historically that has been the average when we look at many multiple years, many five-year, ten-year and twenty-year time horizons. Those that are pessimistic and are trying to time the market are worse off than those that say hey listen, I’m going to take a long-term view. On average I am going to be the winner. Sort of like going to a casino and you get to be the house. You don’t get to win every single hand but over time you certainly are the winners.

And so the future is never certain. It could be different in the future but this is what I think would be a better approach for most people.

Mike Brady, Generosity Wealth Management, 303-747-6455. I’m always here if you want to talk. Thank you. Bye bye.

Wealth is the ability to fully experience life. –Henry David Thoreau

2018 is but a distant memory as 2019 has come in fast and furious! In a very short amount of time we wiped away all of 2018’s losses in the unmanaged stock market indexes. This is a quarter that investors and financial advisors dream of, however now more than ever it is time to keep a level head. You hear me say the same thing over and over, and for good reason. Investing is a commitment and in this commitment you need to stay calm.

In the video I discuss humility and bias. Why? Because none of us can predict the future, we do our best to try by watching the news and this forecast and that one, however these media reports consistently report to stretch either negativity or positivity. Middle of the road, even newscasts don’t make headlines, so it’s our job to take everything with a grain of salt.

Watch my short video or read the transcript below and I give a quick breakdown of what we’ve seen so far in 2019.

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive financial services firm headquartered right here in Boulder, Colorado.

First quarter is over of 2019 and it was a banner year. These are the types of quarters that investors and financial advisors, frankly, live for. In a very short amount of time we wiped away all of 2018’s losses in the unmanaged stock market indexes.

Today I want to talk about humility and bias because I think that they’re very important. I mean just three, four, five months ago there was so much things are horrible and the stock market has continued to go down. A lot of pessimism. And then there was lots of optimism in January and February followed by, just three or four weeks ago I was reading an awful lot of pessimism. And the reason why I bring this up is humility. I don’t know the future any more than you know the future and definitely not any more than those that you see on TV or writing those newsletters or those magazine articles. I mean just take it with a grain of salt, okay, because I think that it’s important for us to have a long-term plan, stick with it and not get too deviated by their particular biases.

And so now I want to kind of shift into bias. The bias of those in the media is not to be even-keeled. It is to be sensational either to pump things on the upside and be overly enthusiastic or to be very negative. Just to say oh my god, the world is about to end. Because both of them get headlines. Both of them run the viewership up into record digits. Saying “oh, everything’s all fine. Let’s just do the middle way” doesn’t really fly. And so you’ve got to read or listen to your news that way with that particular filter. I would actually argue that’s a good way to go through life because what is your personal bias? Is your personal bias to be optimistic or to be pessimistic? Right now I’m just telling you that going back to 1929, three out of four years is positive. One out of four has been negative in the unmanaged stock market indexes. So that means if you’re pessimistic you’re really only right one out of four times. Being pessimistic might serve you well if you are in a bad neighborhood, to keep your guard up, to be fearful. But it doesn’t really serve you very well, frankly, in your investments.

So think about it even from a relationship point of view. If you are afraid of being disappointed in friendships is the answer to have no friends? No. The answer is why don’t I look at myself and see if I can moderate my reaction to my disappointments when a friend might disappoint me. That’s the more logical way I would argue in your relationship or friend relationships but also as it relates to investments. Is the better way to be overly optimistic, overly pessimistic or to take your news with a filter but look for the even way? To understand that hey, my bias might be pessimistic but wait a second, is this the real truth?

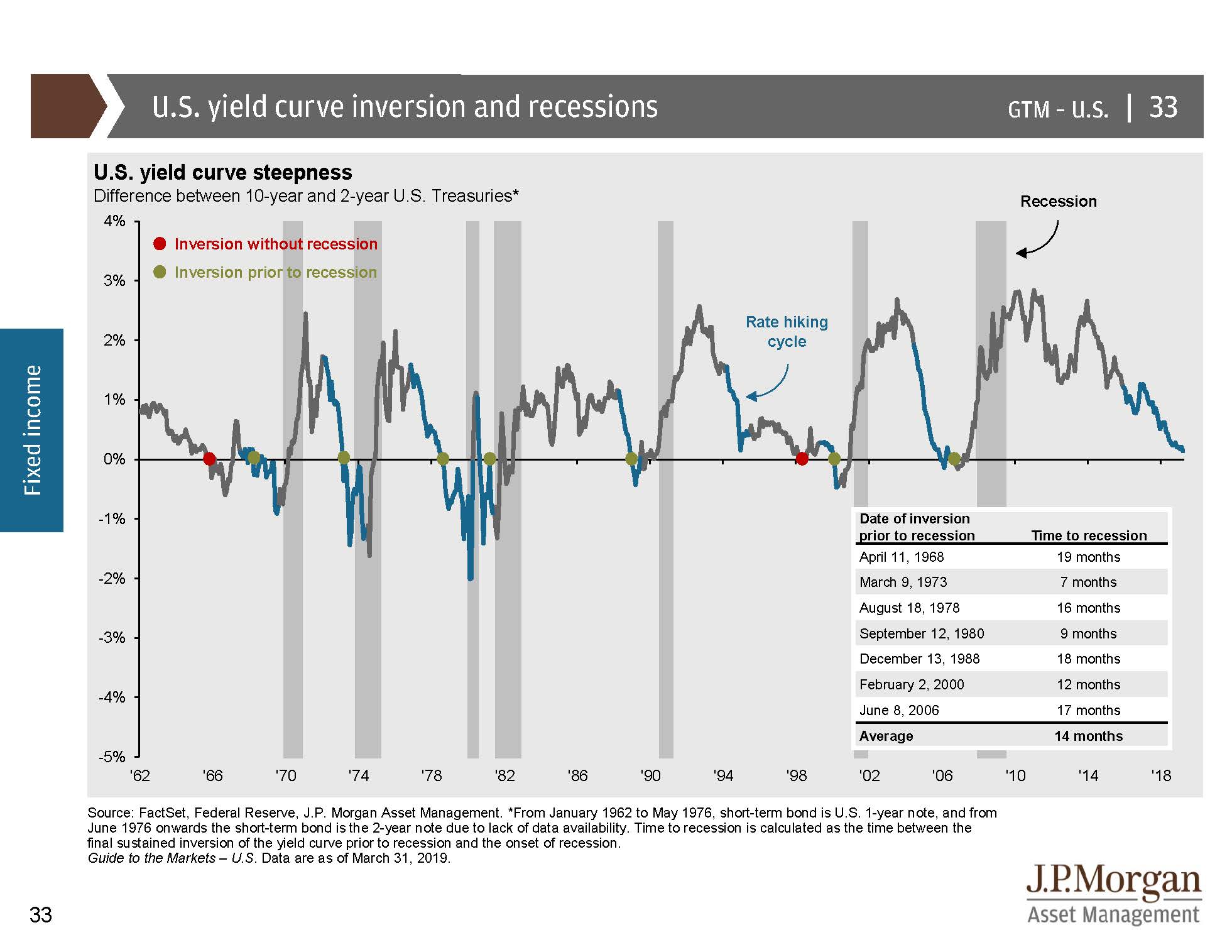

Recently and before I end today’s newsletter there’s been a lot of talk about the inverted yield curve and I wanted to talk about that for a second. The economy is not the stock market. That’s very important to make that differentiation. The inverted yield curve and we can talk about the difference between the ten year and the two year (maybe I’ll do that in an instructional video next month), but when you see that yes, that has led eventually or at least predicted most of the time to a recession. But it’s been a huge differential between seven months and nineteen months. And during that time as I look back over the last – I’m going to put a graph up there on the screen – there’s been some nice stock markets during that timeframe and some nice times to be invested.

I would argue that since there’s a huge variance there of delay and some false positives that it’s not as good of an indicator as you would be led to believe. But even then it’s an indicator of the economy. The economy is not the stock market. It’s very important to remember that. If you look back at the early 90’s there was an indicator of a recession which did happen. However, does that mean that you shouldn’t have investments? No way. The 90’s were one of the best ten year timeframes ever and I certainly wouldn’t take that as an indicator. The last ten years has been a relatively moderate recovery from the Great Recession when you look at all the underlying GDP numbers versus the averages. However, this last ten years I’m certainly proud that many people invested in the markets and kept their investments over the last ten years. The unmanaged stock market indexes have been very favorable even if the economy was not as ripping and roaring as they have in prior decades.

Anyway, Mike Brady, Generosity Wealth Management, 303-747-6455. Give me a call at any time. Have a wonderful day. Thank you. Bye bye.

“It’s the steady, quiet, plodding ones who win in the lifelong race.” – Robert W. Service

The year 2018 is over, and what is most interesting is how different it was from the previous year 2017. This is a good reminder that every year is different, and 2019 will not necessarily follow the negative and volatile 2018.

When I write or say something like that, I inevitably hear from someone who says “yeah, but it’s different this time. Everything has changed because of X, Y, and Z”. In my almost 28 years working with clients, the fundamentals of diversification,time horizon, and complementary financial decisions around your portfolio have remained the same. And no, it’s not different this time. I’ve been hearing that for 28 years.

Watch my video and/or read the transcript. It’s less than 10 minutes, and will give you a good big picture perspective on how I see things.

Hi There. Mike Brady with Generosity Wealth Management; a comprehensive financial services firm headquartered right here in Boulder Colorado. 2018 is behind us. Thank goodness. Forget about it. 2019 let’s hope for a very happy and profitable one. I’m going to put up on the screen the unmanaged stock market index the Dow Jones industrial average, the one that you hear about the most on TV. What you’re going to see is the first quarter was negative, the second and third quarters were positive and that’s where we wished that the year has ended. But then we had the fourth quarter and it took it all away. In particular December very volatile and very negative month right there month of December.

Depending on what stock market index you want to look at you’re looking at the negative five, negative six percent for the year. When you get a little bit more non-common ones like the SMP mid cap, the small cap and you’re looking at the Russell 2000’s you’re looking at the negative double digits, the negative teens, the negative 12, negative14, 15, 16. And when you look at the international markets, whether it’s Europe, whether it’s pacific they were negative double digits as well, the negative teens depending on what particular country and what particular index. Very few places to hide in 2018. When we look over at the bonds the unmanaged bond indexes you’re looking at negative as well, negative single digit, negative one and negative six depending the percent that you’re looking at for that particular area and that’s kind of a unique situation, but with rising interest rates that’s just what happened for 2018.

Let’s think about it though for 2017, 2017 I sat here 12 months ago and talked with you about 2017. At that point what I said is wow this was an incredibly nonvolatile year, I mean pretty much every week every month was positive and it was a banner year, yay 2017, but it’s not real. Go back 12 months ago and watch that video and that’s what I said I’m like this isn’t reality guys, this is a unique situation that very low volatile no volatile year practically was then followed by an extremely volatile year, which is 2018. So we have these two contrasts two extremes right next to each other, which should remind us that every year is different. Every year is different and in 2019 it could be someplace in between. So let’s not extrapolate out and say wow 2018 was negative and really volatile so therefore 2019 is going to be negative and really volatile. It just doesn’t work that way.

There are many variables in the equation that go towards an economy, currency markets, stock markets, bond markets, et cetera, and anyone on TV or who is filling a headline in the newspaper or magazine that says this is the reason why the number one reason or this is the sole reason is fooling themselves and they’re fooling you and don’t listen to it. There are a number of factors in a multiple trillion-dollar economy and world market and it’s simply not as simple as this is the reason. When we are creating a portfolio, when you as an investor are trying to reach your financial goals it is important that we stack the odds in our favor to the degree that we can. Absolutely nothing is guaranteed in this world. I just want to say that. But what we can do is look at history and say how can we stack things in our favor knowing that the future might be different? And I’m going to say that there’s three things that we can do: number one, stay diversified, have the right timeframe and then look at all the things that are around it surrounding all those decisions. Let me break each one of them apart.

Number one, stack in our favor with the timeframes. Talk about that first. On a daily basis the market is going to be up or it’s going to be down. That’s it. That’s a very short timeframe and I don’t know on a day-to-day basis anymore than you do whether the market is going to be up or it’s going to be down. When we look out to a year we zoom out like a mosaic we kind of get a little bit more perspective, we step back from the wall and we look at a year we say okay going back to 60, 70, 80 years of market data three out of four were positive, one out of four were negative and sometimes those negative years were strung together. I mean I remember in my career 2000, 2001 and 2002 were three negative years right next to each other. Now I will tell you that 2004 and 2005 were good years. I know because I was there. But 2000, 2001, 2002 were negative years, but three out of four are positives. So when we look at on a yearly basis we’re starting to stack things in our favor if what has happened historically was to continue in the future.

When we look at five years has there ever been a time horizon were a diversified portfolio, 50 percent of an unmanaged bond index, 50 percent of an unmanaged stock index together has lost money? The answer is no. I’m going to put that chart up on the screen. When we look out five years, ten years, 20 years now historically the odds have been in our favor when we can hit our particular mark. So it’s important for us to remember that the future could be different, I just want to let you know that. Having a diversified portfolio does not guarantee market losses in a declining market. I just want to say that. But we’re looking at the right time horizon for what you’re looking at from a client point of view.

Diversification, I said that that was very important. That is important. When you see on TV people who have lost everything that makes great news; oh my gosh little older lady lost all her money in this particular stock or this particular shopping mall or scheme, et cetera. That’s why it’s important to not invest in one individual stock or just a few stocks or a shopping mall or whatever it might be, they make great spectacular horrible stories that’s why you avoided them. A diversified market, diversified portfolio, even when we look back at 2008 the recovery period was two to three years. That was the absolute worst that we keep talking about the great recession was two to three years. And when I explained just a minute or two ago about the five-year and the ten-year time horizons that’s important to remember. Even in the worst situation when we kept our eye on the big picture reaching our financial goals that’s how we were successful.

The third thing is what are all the decisions around it? It doesn’t matter if the market is up if you haven’t save enough money. It’s that simple. It doesn’t matter if the market is up if you’re withdrawing too much money. It’s that simple. So you’ve got to know what your withdrawal rate is and what your deposits rate is depending on which cycle of life you are in. If you are older 60, 70, 80, listen I’m hoping you still have a long time horizon. Hopefully you have a time horizon of five, ten, 20 years, maybe longer depending on what your age is. Perhaps you’re investing the money for not just yourself but for your heirs, that’s important to remember that the time horizon then becomes a longer time.

So every year is different. I’m not going to sit here and tell you that 2019 is going to be positive or it’s going to be negative, I don’t know. But what I do know is that I’m a believer in the economy, I’m a believer in the United States for one thing, and I’m also a believer in a diversified portfolio for the long-term is going to be a wonderful thing for the vast majority of people, but only you can really decide whether the time horizon that you have and a portfolio that we’ve crafted together or that you’ve crafted with your financial advisor, if you’re not a client of mine you should give me a call, is appropriate because volatility and risk in my mind are two different things. The risk of you not having enough money, you not saving enough or you withdrawing money or not reaching your goals those are risks. A subset of that risk is volatility and volatility is always going to be there, particularly when we’re looking at things from a short-term. Short-term means days, weeks, even months, but when we start to look at longer multiple year strings together, string the years together, the volatility starts to tamper down because then we can get some perspective of how it fits towards the end goal.

Mike Brady; Generosity Wealth Management; 303-747-6455. Give me a call at anytime. Bye bye.

“I have a lot of things to prove to myself. One is that I can live my life fearlessly.” – Oprah Winfrey

There has been a lot of volatility this year, and in the past few months, almost all of it down.

While I routinely send out a quarterly newsletter and video, due to the extent of the news and conditions right now, I’ve been sending more frequent updates with my current thoughts and advice.

I highly encourage you to listen to my most recent newsletter video (it’s a little over 5 minutes).

Hi there, Mike Brady with Generosity Wealth Management; a comprehensive financial firm right here in Boulder Colorado. So I’m recording this on the morning of December 24, Christmas Eve. I want to talk about what happened last week the week before Christmas and frankly this entire year because this is going to be a trifecta when we look at negative stock market probably for 2018, unless there’s some miracle in the next couple of days with the unmanaged stock market indexes. Same thing with the indexes for the bond markets and for the international markets in general, kind of your developed market international. It’s kind of a trifecta everywhere things were negative for 2018.

I think it’s very natural for people to say why, why did this happen? And just like 2017, which was a very, very good year, people assume that it will continue. Many people thought okay great, 2018 is going to continue just like 2017. That was wrong. 2018 does not mean that 2019 will be negative, it just doesn’t work that way. As a matter of fact going back historically one out of every four years is negative and yes sometimes when the stock market is down the bond market is down as well. That does happen. But the way I like to think of it, and I did this great video, which I might provide a link to, where I say that life is more like poker than it is chess, you’ve got to make sure you get the right lessons from it. Chess is completely strategic, you know, X leads to Y I mean that just is it. At the end of the day the better player will always win at the conclusion of a chess game. Poker is not that way there’s an element of things outside of our control.

The reason why I bring that up is we’ve got to have the right lesson. Just because things are negative doesn’t mean that there was either a mistake or that we should change our particular strategy. If you go through a red light and you’re not hit by another car that doesn’t mean that going through red lights is good. Or if you go through a green light and you are hit doesn’t mean that going through green lights is bad. It just doesn’t work that way. And so when we look at the long-term we have to make sure that we don’t make short-term decisions based on long-term goals. That’s very, very keen. As a matter of fact that’s one of the mistakes that investors have a tendency to make is they let their emotions, I’ve already acknowledged that being scared and disappointed is a very natural thing; we’re emotional human beings. The question is what do we do with it from there? Do we act on those things or do we say I created a plan that allows me to stick with it knowing that there will be highs and that there will be lows. And I believe that there will be more highs than there will be lows and over time historically diversified portfolios. Not those in just one sector like technology, not those just in emerging markets or some place very non-diversified, but in a diversified market historically that has been the case.

When we look back at diversified portfolio going all the way back to 1950 of 50 percent stock market index 50 percent bonds, there’s actually never been a five-year time horizon where we haven’t at least broken even or made just a little bit of money. I’m going to put that chart up there on the screen so that you can see it for yourself. Have there been one, two and three years? Absolutely. As a matter of fact just in the last 15 years we’ve had a couple of those, we’ve had 2000, 2001 and 2002; those years were negative for the stock market followed by a very nice 2004, ‘05, ’06. And then in 2008 it went down again. Very painful. If you had a diversified portfolio your break even was two to three years. These things do happen. These things are things that are hard to see and people who say well I saw it and it was so obvious and maybe even they say I moved to cash because I knew it was going to happen, my experience over the last 27 almost 28 years is those people who say that probably moved out a little too early and they don’t get back in. Yes they might feel all good and all happy with themselves that they moved out, but the better strategy, as I see it, is to stick with the strategy that you have, which was for a long-term. If you need the money next month that’s a problem, you shouldn’t have investments to begin with. However, we look at our life like a business and we have to make decisions, not emotionally, as it relates to things as well.

I’m always here. Mike Brady; Generositywealth.com. Please go and watch some of my other videos. I’m going to provide some links to them as well, but Generositywealth.com; Mike Brady; 303-747-6455. Hope you had a wonderful Christmas. You’re probably receiving this after Christmas to a happy new year. Thank you. Bye bye.

“The big picture doesn’t just come from distance; it also comes from time.” – Simon Sinek

When we look at the news, when we look at the markets we might get all worked up. We might have the same perception that everything is going down the tube, particularly when it might happen to us, but I’m here to remind you to stay calm and remember the big picture.

—————————————————————————————————————————————–

Transcript

Hi There. Mike Brady with Generosity Wealth Management; a comprehensive full service financial services firm headquarters right here in Boulder Colorado. So I want to talk a little bit about non-market stuff first, but it is relevant and I think you’ll find it interesting. With all the news about handgun violence in Chicago or mass shootings, if you were to ask most people are we in a more violent America today than we were 25 or 30 years ago? I’m going to make a statement that most people would say yes. But the reality is that’s just not true.

I’m going to put a chart up there and you’re going to see that one of the biggest successes that we’ve had over the last 20 or 30 years is our decrease in violent crime. And, of course, we want it down to zero don’t get me wrong, but that is one of the trends that has been kind of missed when you’re watching news on a daily basis. What about property crime? Are you more susceptible to property crime? Actually no. I’m going to put a chart up there on the screen and you’re going to see that same kind of a trend, we actually are living in a less violent America than we were 25 years ago than we are today, even though you might not feel it. Property crime is the same type of thing, you’re actually safer and your valuables, et cetera, than you were 25 or 30 years ago, even though you might not feel it. And I would say when it happens to you it certainly becomes personal and it certainly doesn’t feel like when I throw a chart up there you’re like wait a second, but I was impacted dramatically by it on a personal basis.

The reason why I bring this up is when we look at the news, when we look at the markets we might get all worked up, we might have the same perception that everything is going down the tube, particularly when it might happen to us, we’re like oh my gosh I used to have X amount and now I have a little bit less from whatever point that you particularly pick. And many times I would say that you pick a point that’s pretty short. You have long-term goals yet you pick a point, a high point, that’s short-term, which in my mind makes no sense.

Remember 2017? It was just a year ago. Market went up pretty much, the unmanaged stock market indexes went up almost every week and pretty much every single month and if you were invested in that most people saw a portfolio that went up that way as well. If you look back at my videos 10/11 months ago I would say that’s real unique. That’s the exception, not the norm. So you might say wow the market has gone down spectacularly in the last couple of weeks. It’s been very volatile this year. My answer would be yes it has. Yes that’s true and if you need the money next month that might be a problem. Of course right now as I’m recording this on a Monday morning we’re right back, at least from a Dow, the unmanaged stock market index, is back to where it was maybe 12 months ago. Definitely up for where it was two years ago, definitely up from where it was five and ten years ago. The future could be different. I think that’s what people are always worried about they’re like wait a second is this a new trend? It’s different this time. I don’t know how many times in the last 27 years I’ve heard that it’s different this time and every reason for why it’s different seems to be different. That’s the only thing that changes, and then it’s not.

So what I would say is when the market goes up, an unmanaged stock market index just for illustrative purposes, 100 points over four days or over two weeks let’s say and then gives up 300 or 400 in one day, only one of them gets the news. So far this year we are negative 2018 and I don’t know where the year is going to end. That’s actually kind of the big mystery for this year, what’s going to happen between today and the end of the year? But the end of the year is just one point, I mean that’s the one interesting point is that if decisions are made based on an arbitrary date on a long-term vision that you have for yourself that makes absolutely no sense to me.

Three out of four years historically have been positive, which means one out of four have been a negative. And being a few percent negative causes someone to change a long-term strategy, you’re going to be worse off for it. That would be my opinion going forward. You don’t know the future and I don’t know the future. The only thing that really changes when the market goes real volatile or goes down is that everybody seems to know on the news exactly what’s going to happen. All of a sudden the confidence level that everything is horrible and crappy just went up by two or maybe three. And of course, the people coming out saying I knew it all along comes out as well, which of course is ridiculous. I’m sorry that’s the reason why I personally don’t watch CNBC or some of the other news programs because when have you ever turned on the news, the local news and said everything is okay, everything is great. Wow, things are going just fine. That just doesn’t work that way. In order to be successful you have to understand that long-term the market has gone up, long-term diversified portfolios have gone up even though the future could be different. If you’re not willing to take some risk in a down year, in this year if it’s going to be down a few percent that’s part of the game. We’ve talked about this if you go back every year I’ve been doing videos for ten years now, almost 200 of them, it’s always the three steps forward two steps back and if you focus on the two steps back then you’re never going to have the three steps forward. That’s just the way investing works.

Am I rattled by all this? No. Should a strategy change the market – I’m going to move this over just a little bit because the sun is hitting my eyes. When the market first hit 24,000 and it went up to 26 and now it’s back down to 24,000 the unmanaged stock market index, did you change your strategy? No. Did you change it when it first hit 24? No. What I have seen over the last couple of years, my goodness why am I saying that, over the last 27 years, when the market hit 20,000 people were like well it’s obviously at a top. And then it went up to 22 and people were like well it’s obviously pretty toppy, pretty much at a high, that’s obvious. That was a year and a half ago. Then it went up to 23, 24, 25, 26, 26 and a half and now it’s back at 24, now it’s in the 23 for the unmanaged stock market indexes.

If you bought at 26, great, that’s not so great. But the reason why you bought it is you assume, and history has shown, that in the long-term it’s higher, the long-term being three, four, five, six years. However, if you bought it at 20, 15, 16, you know what, that’s why you have long-term. And long-term where was it? It was just a few years ago; we’re not talking decades ago. So you’ve got to keep the big picture in mind, particularly when you’re looking. I’m going to throw up on the chart there what it looks like. That’s what its looked like over a one, a two, a five and a ten-year time horizon. If you only focus on the short-term like a mosaic real close to your face, you’re never going to see the big picture. It does become personal. It does become personal when it’s your portfolio, that’s why you have to perhaps be even more cool and listen to maybe someone like me who is saying don’t listen to the guy on the news because he’s going to try to get you excitable. Is it exciting to go to the barbecue and have everyone say yeah everything’s great? No. People are either fearful or they’re greedy. When the market is going up all they want to do is talk about their winners. When it’s going down it’s oh my God everything is horrible. Who can I blame for this horribleness? Don’t fall into that trap. That’s all I have to say.

I’m always here if you need to talk with me. 303–747–6455; Mike Brady; Generosity Wealth Management. Bye bye.