“Worry does not empty tomorrow of its sorrow, it empties today of its strength.” – Corrie Ten Boom

There’s an old adage that says that the market takes the stairs up and the elevator down. And what that means is that there are sometimes in history spectacular events that have become noticeable that become memorable like this past week or so when we’ve seen some double digit declines. But stay calm, your long-term investment strategy should remain unshakeable.

Hi there. Mike Brady with Generosity Wealth Management; a comprehensive full service financial services firm headquartered right here in Boulder Colorado. I’m recording this Friday afternoon after a pretty eventful week. A very interesting week hence the reason why I’m doing this video. If you look at the background it’s not my normal one, I happen to be at a conference so this is my hotel room, but it was so important I felt to get to you as quickly as possible that I decided to do it right here in my hotel room. Fortunately, the way I look at it I’m never working and I’m always working. When you love what you do you never work a day so I love what I do.

So, there’s an old adage that says that the market takes the stairs up and the elevator down. And what that means is that there are sometimes in history spectacular events that have become noticeable that become memorable like this past week or so. The market has pretty much every day this week had very memorable, you know, the Dow, which is an unmanaged stock market index, decline of the hundreds if not even over a thousand points. And what that has done is brought us back to where we were eight months ago. I mean let’s remember that this doesn’t mean you lose all your money that you can market has gone down to nothing, this is back to the beginning of June.

I’m going to put a chart up on the screen. One of the reasons why I continually talk, both in these videos and with my one on one client meetings, is that if your time horizon is six months, 18 months you should have nothing in the market. One of the problems with big events like this is it really brings people’s attention to it and they start to question in a one week’s time what a two, five, 20, 30 year goal is, which makes no sense to me. The reasons why you have investments is because you don’t need it in the short-term after a one week, one month, 18 months, two years, et cetera. And even when we look at, I’m going to put a chart up on the screen in just a second, even when we look at the absolute worst time on most of our lives history back to 2008 your breakeven point was depending on whether you were 40 percent stock and 60 percent bond, indexes, that would have been a two-year breakeven or three years if you were 60 percent stock index and 40 percent bond index you would be three years or 100 percent in the stocks your breakeven is five years. Now, that doesn’t mean that the five years is necessarily pleasant or the two years or the three depending on what the mix is, but we can have investments that are short-term. I mean just like when we look back to where we were about eight months ago most of us were feeling great we’re like oh my gosh this is wonderful the market I even heard some people say it must be at a top, it must be at a top, whereas here we are eight months later saying oh my God it’s Armageddon. And neither of them are true, they are both points in time along the path of the multiple year strategy.

If someone is only now paying attention that’s less helpful. There’s another adage that says that worry doesn’t change the future and worries the present and so that’s not very helpful. The reason why we continually talk about in our professional meetings and conversations hopefully if we’re talking to ourselves as investors is hey I’ve got this point in the future that I need to go to and that I want to get to for my financial goals and it’s not next week, it’s not hopefully today. If so you’ve certainly shouldn’t of had any money in the market.

So, the question is how do short-term events impact long-term strategy? And the answer should be not at all. That’s why you do it in advance. That’s why my example of perhaps a fire in a house that’s why you have fire drills in a school, in a house, in a building beforehand because if fire is actually happening it’s too late. And so, we hit certain themes, we being financial advisers, me as your financial advisor, the professionals who was doing this for years and for decades of experiences of seeing this we say this is going to happen.

I’m going to put a chart up on the screen.What you’re going to see is those numbers, double-digit declines, are the normal. The actual unique event is that we haven’t really had many of them in the last two, three, four years. Now, it usually doesn’t happen in one week. That’s interesting. That’s a very newsworthy event, but that’s actually the normal is for there to be double-digit declines intra-year within the year. So, what we’re seeing here I don’t know what next week will bring, but I do know that the strategies that were sound two weeks ago are still ones that are sound today. And so, rest easy knowing that we’re here on this path of two steps forward maybe one step back, but we don’t have the two step forward without periodically having the steps back as well.

Mike Brady; Generosity Wealth Management; 303-747-6455. Have a great weekend. Bye bye.

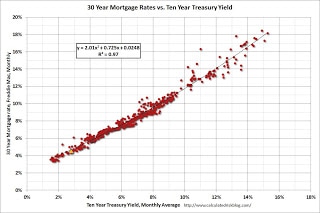

According to Lou Barnes, a local mortgage broker who is frequently quoted in the national press, when the 10 year treasury yield hits about 3.33%, we’ll be back to 5% 30 year mortgages.

Right now, the 10 year treasury is around 2.775%, up about 1.1% in just a few months. However, it has stabilized.

The big question those in the investing world are asking is whether the yield will continue up, or go back down.

If you watch my video, you’ll see that I believe the yield will go back down.

But, as Lou points out, the correlation between the 10 year yield and 30 year mortgages is very clear.

Good morning. Mike Brady with Generosity Wealth Management, a comprehensive full service wealth management firm here in Boulder, Colorado, and I am so pleased to talk with you this morning because we’re going to talk a little bit about the first quarter of 2013. We’re going to talk about the rest of the year. We’re also going to talk about unintended consequences, and I’ll talk about what I mean by unintended consequences in just a little bit.

First quarter of 2013, very good quarter, particularly if you’re 100% invested in the S&P 500 (which you probably shouldn’t be), and very disappointing for you if you’re 100% invested in wheat futures (which you probably shouldn’t be). Realistically you hopefully have a well diversified portfolio of stocks and bonds and cash in US and international, something that fits well with you with your risk tolerance level. If you’re my client, of course I’ve talked with you about that. If you’re not my client, well gosh darnit, you should call me so I can work with you on that.

I’m going to put up on the chart there something that might be a little difficult so I’m going to put a link to it so you can grab the high definition JPEG of it, but you’re going to see across the gamut there, from on the left you’re going to see the S&P 500 all the way to the wheat futures there on the right, all kinds of ranges from – from very good double digits in the positive to for the unmanaged stock impact indexes to double digit negatives for those – those evil wheat futures.

I’m always reminded that like predicting the weather, predicting the economy and predicting the markets, et cetera, is a very complicated proposal. No one is absolutely right, and there’s many different variables that go into it. The older I get, the more humble I become, and at the beginning of the year I said that I thought that this was going to be an up and down couple of years, that it’s going to be a trading range, and I was asked by a client last week if I was surprised by the first quarter strength and the answer is I was surprised but one quarter does not a year make. One quarter does not a two-year time frame make, and I hold to that.

I think that going forward there are so many pieces of data that are negative, there are so many pieces of data that are positive, and that’s normal. When someone says to you, if you see some kind of a TV pundit or an analyst that, well, all these, we have conflicting data. Well, there’s always conflicting data. There’s never 100% way or the other. We have to become comfortable with that type of chaos, and we I think have to take all the data in and say, okay, what does it really mean? And for me it means that it’s going to continue to be that muddle through.

One thing that does concern me from an economy point of view is it feels like a very sluggish economy. The participation rate from an employee point of view, I’m going to throw a chart up there, continues to discourage employees. That being said, I don’t take the complete pessimist view, because we knew this going back that there’s going to be so many baby boomers exiting the work force, so we knew this. Remember that book back in the early 2000s, The Roaring 2000s by Harry Dent, he talked about how around this time frame there are going to be a lot of people exiting the work force and starting to withdraw money from the market. That being said, I think that if you talk with some of your friends and family members, you probably know people who have tried to get a full time job that have decided to go back to school or decided to take something that is less than full employment or what they’re looking for, so it’s a combination of those two, and at various points in time we have a major shift change, and I think that we’re going through that right now and have been for the last two, three, four years, of what does it really mean to be fully employed? What skill levels are we as a society needing in some of those high tech and creative positions? And so that’s what we’re seeing right now. It’s always painful when we go through it, but I’m ultimately an optimist on the US and how we solve things and our ability to weather many things.

Now, I want to talk about unintended consequences. The unintended consequence from August of 2011, remember what we were talking at that point about the down grade of the US from triple A down to double A, and everyone said oh, my gosh, no one’s going to want our treasuries. Well, the exact opposite happened and people basically looked at, investors looked at all of their options and said, you know, this can have a huge impact on some of these other asset classes. I actually want the treasuries which look the best horse in the glue factory, and so that’s exactly what happened. There was a huge rally in the treasuries. I think about, and this is a slight tangent, but I think about Kenya about four or five years ago. I think many of you know that I go to East Africa for two to three weeks a year and do some charity work there, and in Kenya they had a riot after one of the elections and it cut off the whole, you know, Rwanda and Uganda from the ability to get fuel and to get other goods and services because they were coming through Kenya. Well, what was the unintended consequence of that? Now there’s a huge pipeline and rail that’s going through Tanzania that completely bypassed – they’re going to completely bypass and have as a secondary something that’s not Kenyan. That’s really going to long term hurt Kenya, who had a monopoly on getting goods and services in there.

The reason why I bring that up is let’s look at what happened with Cyprus and the European monetary union. Essentially the Cyprus banks decided to treat their depositors as investors in the bank, saying, well we’ve lost all this other money, we can’t – we’re having real difficulty, and the European monetary – European Union is basically saying well, you got us tickets to those uninsured depositors. Now, if you were a depositor of a large amount, you think that’s not going to cause some concern down the road? I mean, I think this is probably the end of the Cyprus banks there, and it also had an unintended consequence of everyone else who is looking at the investing, not investing but depositing banks and European banks is that the European Union said, you know what? This country, the next time Italy comes around, the next time Portugal or Spain comes around, or Ireland, you know, you’re on your own. It’s up to the country. We’re not unified as a European monetary union, unlike what we have here in the United States.

So I think that the unintended consequence of that is a further segregation of the banking system and financial system in Europe that’s just going to speed along what we’ve been talking about for two to three years. Whether all that money that was part there now comes towards the US banks is still to be seen. That being said, I actually think the US financial system is still sick, I mean there seemed to be no consequences for bad action and bad investments even here in the United States, and this is something that we’re going to have to pay at some point as a society and as tax payers, and I don’t know when that’s going to be, whether it’s one quarter, two quarters, two years, or within ten years, but that is something that is going to have to be addressed at some point.

What does this mean for 2013/2014? I continue to believe in the trading range and that we need to be prepared for some up and down movement in the next year and a half, year to year and a half to two years. If you’re my client, of course I’ve talked with you about it. I met with pretty much all the clients in the first quarter and I tried to recommend managers and third party managers that I believe do well in that type of market.

I’m going to put up there on the chart a long term 110-year, 113-year view of the market, and the longer the time horizon that you have as an investor, the happier you’re going to be. If you’re a minute by minute, if you’re an hour, a day, a week, a month, those are hugely short times frames, and what we want to do is have investments that do well on the yearly, the two, the five, and the ten-year time horizon, and if we can have decade time horizon, you’re going to be a very happy, happy camper.

Before I end here, I’m going to throw a couple more charts up to show you what Europe looked like in the first quarter. You’re going to see that Europe was definitely trailing the S&P 500. You’re going to see that the financials trailed all the European stock market indexes, the unmanaged stock market indexes even more, and going forward I think that we need to be prepared for some volatility. We have to remain diversified, and we have to remain consistent with the risk level that we need for the plan that you hopefully have in place. The reason why I say the plan that you hopefully have in place is you’ve got to know where you’re going, you’ve got to have that nice retirement analysis and plan, and what risk level do you need? Because if you only need 2 to 3% a year and you’re taking risks that can get you 10 or 12% in a good year but also lose it in another, why are you taking all of that risk? And so I think that that’s something that you need to keep in mind.

I’m going to wrap up now, because it feels like I’ve been talking for awhile. I’m going to be a little bit more consistent with my videos going forward because gosh darnit, this first quarter was so busy for me as I was meeting with my existing clients and meeting with new people, that I didn’t have – I felt like I was communicating one on one all the time but I wasn’t doing as good of a job with my newsletters and my videos, and I’m going to get back to that, so you’ll see an awful lot going forward.

I am taking new clients. I would love for you to give my name out to your friends and colleagues and family members, et cetera, have them give me a call. We’ll have a conversation whether or not it makes sense for us to sit down and whether I’m the right guy to help them out. What people want, I can’t help everyone, so what they might need might not be what I do, and I’ll be very blunt about that and then very timely of course, but I’ll try to point them in the right direction.

Mike Brady, Generosity Wealth Management, 303-747-6455. You have a wonderful week, wonderful quarter. Thanks, good-bye.

August 20th is a pivotal date when 3.8 billion Euros are due from Greece to the European Central Bank.

The IMF is saying that if this isn’t paid, they’ll stop loaning money to Greece.

Once the IMF is done with Greece, will the European Monetary Union be far behind?

In my opinion, Greece will exit the Euro sooner rather than later, and this is good for the long term strength of the Euro.

How will this affect our US markets? Always the big question. More stability and stronger private balance sheets makes the US a better investment I believe.