Twelve months ago, the 5 year return for the S&P would have covered 2008 – 2012, for a +1.66% annual return (including reinvested dividends). Today and one year later, because a bad year dropped off (2008) and is replaced by a good year (2013), the 5 year annualized return jumps up to +17.94%.

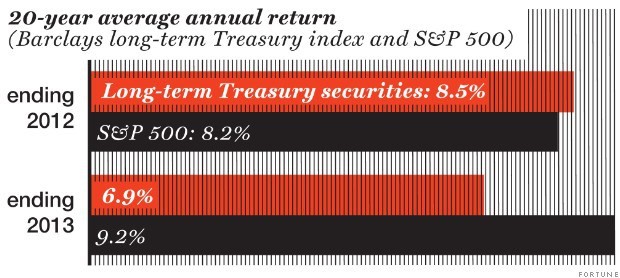

Let’s look at another longer term statistic. A year ago, the 20 year annualized S&P 500 return was +8.22% a year vs. +8.50% a year for long term Treasuries. Makes the argument that you should put all your money in long term treasuries, right? I mean, the annualized 5 year return for the S&P 500 was just +1.66% and it underperformed the 20 year annualized Treasury return.

Had you done so, you would have lost -12.7% last year (as measured by Barclays index of long-term Treasuries), and missed out on 2013’s 32.4% gain for the S&P 500. The 20 year track record in one year has changed the 20 year average to +9.22% for stocks vs. +6.92% for Treasuries.

One of the most important lessons investors need to keep in mind is the “non-linear” nature of investments. Just because a particular investment (whether it is stocks, bonds, or some sector) has done well in the past does not mean it will do well in the future. And, the opposite is true as well.

When I give advice to clients, it’s taking the past into consideration, but it’s present and future focused.

In my video today, I discuss what I’m hoping people don’t take away from 2013.

Diversification? What that?

For a full discussion of this, listen to my video.

Transcript:

Hi there, Michael Brady with Generosity Wealth Management, a comprehensive full-service wealth management firm headquartered right here in Boulder, Colorado.

Today, I want to talk to about the lessons of 2013. I know it is only mid-December but we’ve got 11 1/2 months and I think it’s close enough. More than anything, I want to talk about the lessons I’m hoping investors don’t take away from 2013.

Before I get started, let me just say you’ve heard me for a long, long, time talk about diversified portfolios. A diversified portfolio does not guarantee that in a generally trending down market, that you will not lose money. It’s going to be stocks and bonds and cash. However, a diversified portfolio is still absolutely essential.

This past year 2013, the best thing you could have done was have 100% of your money in the US stocks, either stock index or a preponderance of individual US stocks in general. Why have any of those international stocks? Or avoid bonds. In general, bonds, ETFs, or bond mutual funds in general are down single digits or maybe even double digits if you’ve got some long term treasuries. If you’ve got a real estate investment trust, maybe you’ll break even for the year. If am an unsophisticated investor, I might say, “Gosh, this whole diversification things, ah that’s crazy. We should just look at the US stock market the past year and so for 2014, I should just have 100% of my money in the US stock market.”

My answer is that is the wrong lesson. I happen to be bullish. You’ve heard me considering the last two, three, four months, that because of the quantitative easing and the amount of money that’s out there, et cetera, and some other factors, I happen to be more optimistic for 2014 than I otherwise would be. I think at least for the next couple of years, things might be okay but of course that could change. As data changes, maybe my opinion changes. However, the reason why, I’m going to throw a chart up on the screen there and I’m going to highlight the purple ones. You probably can’t see it because it’s kind of small but that happens to be one unmanaged stock market index and you’ll see that in some years, 2003, 2004, 2005, 2006, near the top there, it is one of the best performers. All the way up until 2007 and then it’s the worst performer losing well over half of its value, 53%.

Then in 2009 it’s the best and then it’s okay for a couple years and then it’s absolutely the worst in 2011. Then it’s the best in 2012 and in this past year it’s down near the bottom again. That is all over the place but right there in the middle you’re going to see that the diversified portfolio, the asset allocation thing there is sort in the middle. It is never the highest, it is never really the lowest and that is one of the things that diversification has to do. If going forward into 2014 we know which asset class was going to be the best one to be in, of course we would move 100% of our assets. Unfortunately, we never know that going forward because we can only look in the rearview mirror and say this is the one that I wished that I had. Beating yourself up over it doesn’t help and then taking that and assuming and extrapolating that into the next year just rarely works.

I am going to throw another chart up onto the screen there and what you’re going to see is that over the last 62 years. This is all the way from 1950, that green bar there on the left hand side is the range in one year that some stocks in one of those years, it took two years when the stock market index went 51%. But also one year, it lost 37%. If it was bonds, the very best was that 53, the very worst was 8, but a combination of the two is that last one of 32 to 15. As we go out five years, what you’ll see is you’re starting to normalize your returns and start to get low or high but also higher lows, which is usually what people are looking for. Of course, if we can have our cake and have all of the high highs and of course the highest of lows, that would be a perfect world but when we go out 10 years and then 20 years, what you’ll see is a diversified portfolio starts to get rid of that uncomfortableness of the huge year by year fluctuation because when you have that huge decline on a one year, most people take that the next year will also be a huge decline.

When we look back to the beginning of 2009, March of 2009, that was kind of a low for the market after that huge horrible fourth quarter of 2008 and the first couple months of 2009, most people were not thinking wow the US stock market is what I want to buy into. That is not what most people were thinking but that is actually in hindsight the best time to buy. What I’m hoping that people will not take away from 2013 is that diversification has no value and that is a big joke. That is not the case. A portfolio of stocks and bonds and cash and then of course other types of asset classes that surround it, historically have had the effect of reducing some of the volatility in the high highs and the low lows over time and it creates in my opinion a better portfolio.

One of the concerns that I have is that so many unsophisticated investors will only look at 2013 and dump all of this money in 2014 into just that one asset class which is the US stock market or the unmanaged US stock market index either through an ETF or a mutual fund or an indexed fund or something like that for the wrong reasons. Not because they’d really thought it out but they’re going to have unrealistic expectations and that is unfortunately probably going to come back and bite them. Maybe not in 2014, maybe not in 2015, but if they come with these unrealistic expectations without a diversified portfolio—if I’m wrong, they’ll have nothing to stand on from a diversification point of view to offset what that wrong analysis was. That’s it.

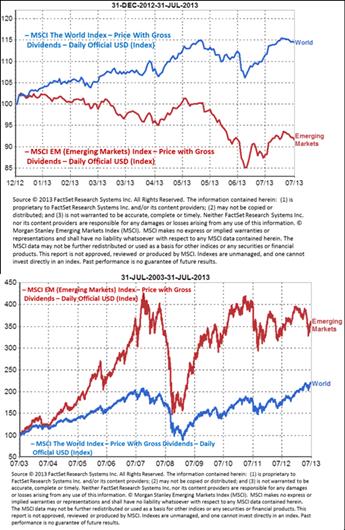

I think highly of Mark Mobius, and he makes a strong argument that emerging markets, while they’ve had some correction this year, is still a great place to invest.

I happen to agree with him.

It’s a great article, so be sure to click and read.

The second quarter was a tough quarter, particularly at the end. Continued emphasis on government fiscal and monetary policies, both here and abroad, played havoc with bond, stock, and precious metal investors. It’s enough to make my hair turn white!

Click on my video to get my thoughts on the past quarter (over-reaction) and the upcoming one. The year is not over!

Hello, Mike Brady here with Generosity Wealth Management, a comprehensive full service wealth management firm headquartered right here in Boulder, Colorado. I’m here for my second quarter review and my third quarter preview.

I wish I could sit here in July 2013 and say that my analysis and the reason for markets going up or going down is because of the profitability of this company or that company or this sector or that sector, but really the big news both this quarter and even as we go back to the beginning of the year with the fiscal cliff and other big topics at the time, has been the intervention and the discussion of the fiscal and monetary policy of the government. In this past quarter it has also been some news out of China that really rattled things, and then of course the continuation there in Europe.

In the middle to kind of late June, Ben Bernanke, the chairman of the Federal Reserve, gave an indication that the quantitative easing would start to drop because the Fed believed that the economy is doing much better, so therefore it’s not needed the easy money that we’ve seen in the last four to five years. What happened is, the bond market really reacted, in my opinion, overreacted, and so the prices went down on bonds, which means that the yields go up. I believe that’s going to settle… there was a lot of outflows from bond funds and bond ETF or the selling of it. I think that once people kind of step back and realize that wow – I’m not going to get any yield in a money market or a CD, etc., they’re going to reengage those particular funds and ETF. So I think that it’s really an overreaction.

At the same time, the kind of equivalent to the Fed over in China, their central bank, also there was a perception that they might have policies that would lead to a credit crunch. The Chinese market went way down as well and I think that was an overreaction. While it’s painful when that stuff happened, I’m not overly concerned as we’re going forward into the third quarter.

Europe continues to be a mess. Look at my videos going back for two years. I’m just going to sound like I’m saying the same thing over and over every quarter. Europe I think is going to continue to be a real problem. This past quarter, those areas that had problems were dividend paying stocks, bonds as I already talked about, and gold. Gold and silver has lost its luster. I think that it’s overreacted on a down side, but hopefully, if you’ve been watching my videos and listening to me, you really shouldn’t have more than, if at all, each client is different – you really shouldn’t have more than 4% or 5% anyway. If it goes down a significant amount, I think it was 23% down just in this last quarter after a huge run up for a number of years, that’s going to majorly impact what you’re doing. I think that the best thing to do is to keep the big picture in mind.

I’m going to throw up on the chart there inflection points for the last 15 years. You’re going to see that where we are, the little arrow that’s pointing there. I don’t believe that we’re at the top of a crevasse waiting to go all the way and straight down. If I were to show you a graph on back all the way to 1900, you would see that these things are normal, these variations like what you’ve seen and a tough quarter that we had, the second quarter, which really took away some of the gain from the first quarter. The reason why I’m not showing you that chart is most people’s time horizon is not another 112 years, so I’m really kind of showing the last 15 years, and hopefully your time horizon is long, even if you’ve just retired, I hope you’re going to live a very long time. I think that some of the overreaction is because the concern about the Fed, but I think the Fed, they have a rosier picture than what I’ve really seen. I think some of their inflation numbers are wrong as well.

I’m going to throw another chart up there. We’re going to see historical returns by holding period. What this shows is going back to 1950, 62 years, that the longer you hold historically, the range of your return in the various sector has a tendency to start to normalize out. Diversification, I think is really key in certain quarters and years, as I talked about gold already, that really help you. This past quarter it hurt you, so therefore, hopefully you didn’t have 100% of all of your assets in gold. That’s the purpose for diversification. It’s not a panacea in that in a generally trending down market, diversified portfolio may be down as well. However, I do think that that’s a wise approach as a tactic and a technique in order to reach your particular strategy. I keep stressing that you have to know where you’re going and have a plan, etc.

A little summary here. For the second quarter gold and dividend paying stocks, the Chinese market in general, and bonds were down, but I think that it was an overreaction. I am optimistic in that regard for the third quarter. I don’t believe, as I see things right now, that the third quarter will bring forth some huge decline and we all run for the door. I do think that we’re going to continue to be in a trading range, both this year and next year. That’s why having good managers that can take advantage of that is important. I’m a little disappointed that in June, some of those managers might not have foreseen that quick or abruptly as they could, but I think it’s an overreaction. It think it’s just a blip at this particular point.

Mike Brady, Generosity Wealth Management, (303) 747-6455.

By the way, I’m having a seminar on the 16th. Give Cassidy a call at my office if you would like to attend. It’s one hour. I’m a straight to the point, this is what I think and why I think it… My attention span is not greater than an hour so I certainly can’t expect anybody else listening to me to have an attention span greater than an hour. I’ll be very sensitive to the time. (303) 747-6455. You have a wonderful day. Thanks. Bye bye.