Market headlines can feel overwhelming—especially during periods of volatility. But not all market movement is cause for concern.

In this latest quarterly update, Michael Brady shares a grounded perspective on what’s happening in today’s market, what a “correction” actually means, and why long-term investors are better served by focusing on what they can control rather than reacting to short-term noise.

If you’ve been feeling uncertain about recent market activity, this is a helpful reminder of what truly matters—and what doesn’t.

Transcript

Hi there. Mike Brady with Generosity Wealth Management, where we align wealth with purpose and possibility. I’m here with my first quarter review, the rest of the year preview video, and newsletter.

I’m asked every once in a while why I don’t get more technical. I touch upon technical topics in my videos, but I don’t go very deep, to be honest. One reason is that when I started 35 years ago, having a technical advantage was the big thing. Now there’s so much information on the internet, on TV, on the radio, discerning what’s important and what isn’t is more difficult.

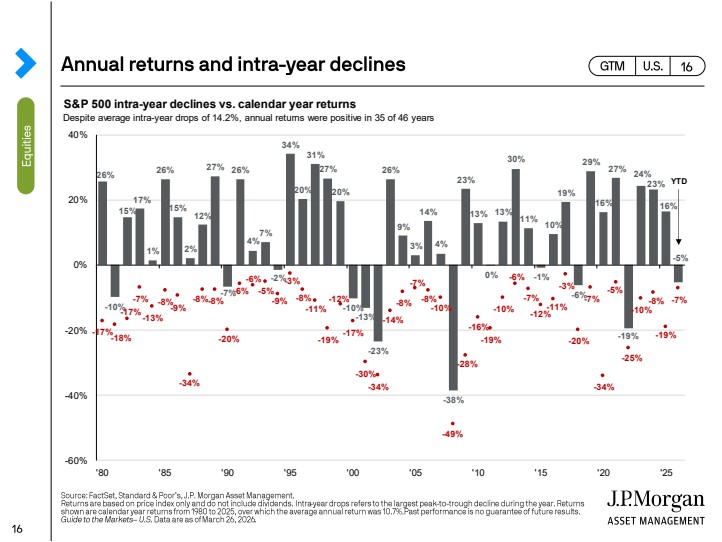

As I view the world now, we are close to a correction at the time I am recording this video. A correction is a 10% drop from the most recent high. It doesn’t mean a 10% loss for the year. It doesn’t mean 10% like you’re never going to get it back. It’s a 10% drop in an unmanaged stock market index. As of this moment, the S&P 500 and the Dow are flirting around with it: 8%, 9%, 10% depending on the day. Most corrections, when you look back over a long period of time, last between three and eight months before they recover. It’s not three to eight years. It’s three to eight months. They’re usually relatively short in duration.

On the screen, you’ve seen me show this before. It is normal for most years, as seen in the red numbers below the x-axis, for there to be corrections of double digits or more during the year. The numbers on the top of the x-axis are what the year ended at, and it does not mean that it ends the year negative. I like to get back to the basics, which is our attitude, whether we’re paying attention to the right thing, and what our particular biases are.

I like to think of the difference between complicated and complex. Complicated is a rocket to go to the moon: A plus B plus C. It has a million different parts, and if you follow the directions, you can duplicate these rockets and build ten of them one after another. Complex is raising a child. You think you do A, and they come back with B because that’s what they did the last ten times. But sometimes they come back with C or D or something else. They come back with an answer you weren’t expecting, and then you respond in a different way, and so on. That’s complex. Human relationships are complex. If I do a certain thing all the time, someone else may respond in a certain way, but then my reaction to their reaction is different, and it continues. That’s complex. It’s not necessarily complicated.

I bring this up because I get tired of the news saying the market went up because of A, or down because of B, as if that’s the whole reason. It’s not that simple. We need to look at it not as static but as dynamic. If I do something, someone else changes their behavior. If I’m selling hamburgers for $10 and I want to increase my profit, I don’t just double the price, because people will buy fewer hamburgers. So when I impose something on the consumer, they react accordingly. The markets are quite complex, and I believe a diversified portfolio is incredibly important. I don’t believe in individual-issue risk, such as focusing on a single stock or bond. I don’t believe that’s the best way for an investor or client to reach their financial goals over the long term.

I also believe that matching the diversified portfolio with the duration or time frame of your goals is crucial. The money you need in three months is different from the money you need in 30 years. If you’re 60 years old, I hope you know that you have a 30-year time horizon. We have to think about that. If you’re in your 50s, 60s, or 70s, you still have many five- and ten-year time horizons, while you might also have short-term needs, like your monthly income.

For today’s review, it’s been volatile in the first quarter, and that’s unpleasant. Nobody likes it when it goes down. We have risk aversion, meaning we feel more pain with a 5% loss than happiness with a 5% gain. That’s human nature. We have to acknowledge that risk aversion. We have to stay calm, rational, and in control of our emotions. Looking at the rest of the year, I don’t know what will happen. My crystal ball isn’t perfect. But if we have a good diversified portfolio, I think it’s the best way to live in an uncertain world, because the future isn’t always known. It’s always uncertain, even if we don’t always notice it.

Let’s keep the buckets in mind: things we can control, things we have some control over, and things we have no control over. Let’s not spend all our time on the things we can’t control. Let’s spend the majority of our time on the things we can control, like how much we save, when we retire, how much we retire on, and some elements of our portfolio and financial goals. That’s my first quarter newsletter and video. I’m always here if you need anything, even if I’m traveling or in Boulder or heading up to Wyoming for the summer. I can run the business from up there, near Yellowstone in Dubois, Wyoming. My number is 303-747-6455.

Mike Brady. I’m always happy you’re my client. If you’re not my client, consider becoming one. Thank you.