Twelve months ago, the 5 year return for the S&P would have covered 2008 – 2012, for a +1.66% annual return (including reinvested dividends). Today and one year later, because a bad year dropped off (2008) and is replaced by a good year (2013), the 5 year annualized return jumps up to +17.94%.

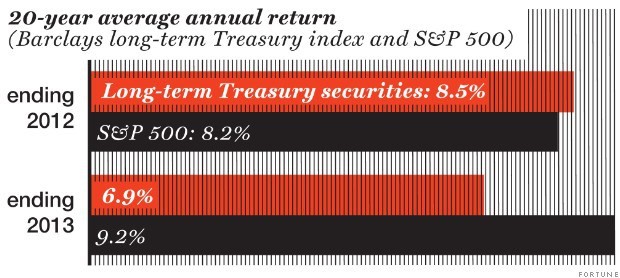

Let’s look at another longer term statistic. A year ago, the 20 year annualized S&P 500 return was +8.22% a year vs. +8.50% a year for long term Treasuries. Makes the argument that you should put all your money in long term treasuries, right? I mean, the annualized 5 year return for the S&P 500 was just +1.66% and it underperformed the 20 year annualized Treasury return.

Had you done so, you would have lost -12.7% last year (as measured by Barclays index of long-term Treasuries), and missed out on 2013’s 32.4% gain for the S&P 500. The 20 year track record in one year has changed the 20 year average to +9.22% for stocks vs. +6.92% for Treasuries.

One of the most important lessons investors need to keep in mind is the “non-linear” nature of investments. Just because a particular investment (whether it is stocks, bonds, or some sector) has done well in the past does not mean it will do well in the future. And, the opposite is true as well.

When I give advice to clients, it’s taking the past into consideration, but it’s present and future focused.

2013 was a great year for stocks/equities in general, and pretty bad for bonds. If only we could rewind the year and go 100% in stocks.

But would that be wise? Sure, in hindsight and only since we know how it turns out. But investing doesn’t work that way. We work in the unknown, crafting a disciplined investment strategy that helps a person reach their goals.

I have a full 2013 recap and 2014 thoughts in my video, so I highly recommend you watch it.

Hi there, Mike Brady with Generosity Wealth Management, the comprehensive full-service wealth management firm headquartered right here in Boulder, Colorado. Today I want to talk about 2013 and 2014. We’re going to go over some graphs and charts together. I’m going to walk you through it. I also first want to talk about the big picture. Now, I’m going to use an analogy here if somebody wants to be healthy in their body and maybe lose some weight and just generally better fit. You might go to a nutritionist and set up a goal by how much they want to lose by a certain point in time. My experience has been that those people who lose that weight, consistently meet their healthy goal are sometimes the most disciplined individuals. They know where they’re going, they make tweaks and adjustments along the way no questions about it, but they are very very disciplined. The reason why I bring that up is it’s the same way in the financial world in my experience.

Twenty years ago I did financial plans for people and some people, now that we fast forward today, some people have met their goals and some people have not. It’s those that did not meet their goals usually not because they bought a mutual fund A and mutual fund B or they bought the wrong investment. It usually was because they weren’t quite as disciplined as the person who has now met their financial goal. The person who has met their goal knew where they were going, they had that financial plan, they stuck to it, and they didn’t get too side tracked by the bright shiny objects. Sort of like with that health person somebody that knows what they’re doing and sticks to it, but they’re not going through the popcorn diet one week or the pumpkin diet the next or maybe even the grapefruit diet, whatever the National Enquirer diet of the week was. The financial world is very similar in that they absolutely made tweaks along the way, they make some adjustments, but they’re also quite disciplined and understand that they’re trying to get to a goal with the least amount of disruption along the way.

The reason why I bring that up is 2013 was a year where if we could rewind it 12 months ago you would say let’s go 100% into the unmanaged stock market indexes of some type because they did very well in 2013. The Dow to the S&P with joint managed stock market indexes between 26% and almost 30%. One of the tendencies is I think for people to say wow I’ve got to have all this equity exposure going into 2014 or 2015, and the disciplined enough need to say that is not the reason why you do it because why you would go into a higher equity position for 2014 and 2015. It also was not very helpful to say oh gosh I should have had it and I meant to do it and I knew it was going to be a good year, we don’t know that, that is all mental head garbage about what was known at that particular point 12 months ago. In the construction of a portfolio let’s keep in mind that each client and you are one of those people who are trying to get to a certain point in the future and we need to keep disciplined as we’re going towards them.

This past year you’ve got stocks and bonds and you usually mesh them together like this, you might have other kind of satellites around there whether or not it’s real estate or gold or other types of maybe satellite investments from your core investment and sometimes the stocks bring up the whole portfolio. Sometimes the stocks bring the whole portfolio down. This year the stocks brought it up, the bonds kind of brought it down, and depending on your percentage allocation between stocks and bonds because each investment is different with their particular goals and objectives, things of that nature, depends on what your rate of return was for 2013. Bonds did not do well last year. Last year was one of the worst years for bonds in a very long time and so in hindsight you wish you had zero bonds, but no it still makes sense for you to have an allocation of both stocks and bonds and it’s my belief that bonds were actually oversold and it still has a great place in your portfolio.

I’m going to throw a chart up on the screen there and what you’re going to see is for 2013, that green right up there junk bonds did really well. It also correlates very highly with the stock market. Beyond that pretty much all the bond indexes were negative, whether or not that was muni, whether or not that was a treasury; pretty much all the bonds were negative for last year. Why did 2013 turn out to be so good for the equity markets? As we look back at it what you’re going to see is there are some hurdles that were removed. You’ve heard me for a long time talking about the continent of Europe and all the issues that are there, but the European Central Bank made some overtures that they’re going to help backdrop some of the government problems. It hasn’t come through yet, but they have said that and the European markets last year did very very well, in the 20% in general. Even though the economy is growing very slowly, so there is a disconnect between what the economy is doing, but also what the stock market had done and that’s a real key thing that you’re going to hear me say a couple times here in this video is what the economy is doing does not necessarily equate to the performance of the stock market, either good or bad.

We also had a lot of fiscal cliff issues the past year, but they really had a minor impact. I mean 10 out of 12 months last year were positive for the stock market, so that tail wind is up. Plus we need to look at the financial profit and growth, Expenses are very low in companies their profit margins are very high. Look up at that sheet there. I put on there the corporate profits right there at the top there. Profit margins are very high, which I think is good and I think bodes well going into 2014 and 2015, particularly because of the amount of cash that has been kind of thrown into the market through all of the quantitative easing and all of the fed action. One of the things that we’re going to hear an awful lot about in 2014, is whether or not there is going to be a tapering. I think that if things continue as they have been going for the last six to 12 months we’re going to hear more and more about that tapering. If December has shown anything the tapering has already started, though was not in effect. The amount of cash, I think of it as a bowl we put lots of money in, just because we’re not putting more money in doesn’t mean that all the money that has accumulated in that bowl just automatically evaporates. No, it’s still there ready to be invested and ready to be loaned out, etc. In 2013, we also had a lot of stock buy backs. We also had a lot of dividends and earnings that were distributed, so it was just absolutely a great year for the stock market as a whole.

I wanted to show you this next graph here or next chart, it’s the S&P 500 price of earnings ratio. That’s something that you’re going to hear an awful lot about going forward. Right now you can see that at 15.4, that’s the price over the earnings and earnings went up. The prices went up quicker than earnings, so the number has gone up. It is higher than it was a year ago still below the 15-year average. That 15-year average also include those crazy 1997, 1998, and 1999 years when the S&P PE ratio was in the 30s and the 40s. I remember those times and it was crazy. You’re going to see that from a real earnings chart up on the screen right now the trailing it is still cheap. The reason why that number is going down is only because it’s relative to the price and so the prices have gone up faster, but it’s still relatively cheap. You can see that dotted line when it gets below that dotted line is when it starts to get more expensive. Now you’ve heard me talk about the bond markets doing poorly last year. This is a 70% increase in a 10-year yield in 2013; you don’t need to know everything about that yield. I have to admit I’m a little bit of a 10-year yield nerd; I love to watch it on a daily basis. When the yield goes up the reason why the yield has gone up is because the price of the bond has decreased. Now here is a long-term trend, but in one year it really spiked up. You can see it right then and there. Then you might say to yourself “oh my God it’s at almost 3% right now, if it continues to go up then the stock market obviously is going to go down. That’s not necessarily the case.

Look at this next chart here and what you’re going to see, and I’m going to kind of put some arrows there about where we are right now, that’s the correlation meaning a correlation of one is two things move exactly the same way. If one goes up the other goes up in equivalent of that’s a correlation of one. If one goes up a little bit, 10% let’s say, and the other one goes down 10% that’s a negative one correlation. The correlation is still positive meaning that when one goes up the other continues to go up as well until the 10-year yield gets to be about 5. Then there seems to be a real opposite between what the bond yields do, which is based on the bond price going down, and the stock market price going down as well as money is flowing into those bonds to get the higher yield. Let’s talk about what happened in 2013 for the global market. You can see that European, Australia, and far east did very well last year just like Europe did, Pacific did, and emerging markets did not do as well last year. What is interesting is this, this next chart there; all the emerging markets are on the top. The emerging market GDP growth, which is the national income of that country is all between 4% and let’s say 8%, but their markets did not do that well.

When we look at the bottom chart you can see the developed market, that’s the U.S., the UK, Europe, etc., and our year over year growth has been around 2% or so, but yet our market says almost in the high 20s, so there is a disconnect between the magnitude I would say between what happened with the GDP, but also the particular stock market. A lot of it has to do with is it already overpriced, did it go too fast and now something else is trying to catch up to it. That kind of concept of the economy does not necessarily mean that the market is going to do exactly the same. One thing I want to throw up on the chart again is the annual returns per year going back oh a good long time, a good 30 years and you’re going to see that most years, those red numbers down there, most years there is a decline of a double digit.

Now let’s kind of talk about 2014. It is difficult to make a prediction about the future. It’s just that simple and frankly I’d avoid the whole thing if I could, but everybody expects it. I think we need to take it with a grain of salt and this is going to get back to our discipline here in just a little bit. I am optimistic for 2014 and 2015. I stay behind what I said 12 months ago, which is that we ought to have good managers that take advantage of some trading ranges and if we have a whirlwind like we did last year, great, we positioned ourselves to be a part of that because we have a diversified portfolio, if 2014 turns out to be negative. Then we still need to have some bond exposure because I believe the bonds will do well if the stock market does poorly. As we create this portfolio together I think we have to probably increase our equity exposure in general, that’s what I’m doing in general, but each client is specific. Please don’t make changes if you’re not a client of mine without talking to me or really talking with her specific advisor. If you’re one of my clients you know that I’m going to be talking with you about that. We’ve got to be disciplined in regards to not getting crazy.

The thing that makes sense for you and your goals to be a conservative investor don’t start going I want to go all equity or I want to go aggressive, etc. because one of my jobs with you is to be a behavioral finance guy meaning that the exuberance and the excitement to say oh my gosh let’s double down, let’s go all in, real investors unfortunately many times buy at the top of the market and sell at the bottom of the market and we want to be the smart money and not do that. We want to be the smart money and many times invest and stay disciplined to our plan even when we’ve got some bright shiny object or a new diet plan has come up, etc., we want to kind of quick make adjustments. That’s what I’m doing with some of my client’s portfolios, is making those adjustments, but also sticking to what we have, which is a diversified portfolio perhaps a little bit more equity exposure, but not getting crazy on it. The reason why I’m a little bit more optimistic going into 2014 and 2015, is the amount of cash that we have in there, the great efficiencies that we’re having that it’s going to continue to play out I believe in 2014 and 2015, for companies. I think that some of the tapering is not going to affect things as greatly as so many people feel and so I think that’s going to be maybe not a nonevent, but a big enough event as we think going forward.

That’s it, that’s my year-end review. That is kind of my 2014 preview, but my biggest thing is the safe discipline with having good portfolios. If somebody reaches their goal before you so what, you’ve got your goal, your plan, your risk tolerance, you stick to it. You stick to that particular plan. It might sound boring, but you know what, sometimes boring wins the race. Mike Brady, Generosity Wealth Management. I’d love to hear from you 303-747-6455. You have a wonderful day, thank you.

In my video today, I discuss what I’m hoping people don’t take away from 2013.

Diversification? What that?

For a full discussion of this, listen to my video.

Transcript:

Hi there, Michael Brady with Generosity Wealth Management, a comprehensive full-service wealth management firm headquartered right here in Boulder, Colorado.

Today, I want to talk to about the lessons of 2013. I know it is only mid-December but we’ve got 11 1/2 months and I think it’s close enough. More than anything, I want to talk about the lessons I’m hoping investors don’t take away from 2013.

Before I get started, let me just say you’ve heard me for a long, long, time talk about diversified portfolios. A diversified portfolio does not guarantee that in a generally trending down market, that you will not lose money. It’s going to be stocks and bonds and cash. However, a diversified portfolio is still absolutely essential.

This past year 2013, the best thing you could have done was have 100% of your money in the US stocks, either stock index or a preponderance of individual US stocks in general. Why have any of those international stocks? Or avoid bonds. In general, bonds, ETFs, or bond mutual funds in general are down single digits or maybe even double digits if you’ve got some long term treasuries. If you’ve got a real estate investment trust, maybe you’ll break even for the year. If am an unsophisticated investor, I might say, “Gosh, this whole diversification things, ah that’s crazy. We should just look at the US stock market the past year and so for 2014, I should just have 100% of my money in the US stock market.”

My answer is that is the wrong lesson. I happen to be bullish. You’ve heard me considering the last two, three, four months, that because of the quantitative easing and the amount of money that’s out there, et cetera, and some other factors, I happen to be more optimistic for 2014 than I otherwise would be. I think at least for the next couple of years, things might be okay but of course that could change. As data changes, maybe my opinion changes. However, the reason why, I’m going to throw a chart up on the screen there and I’m going to highlight the purple ones. You probably can’t see it because it’s kind of small but that happens to be one unmanaged stock market index and you’ll see that in some years, 2003, 2004, 2005, 2006, near the top there, it is one of the best performers. All the way up until 2007 and then it’s the worst performer losing well over half of its value, 53%.

Then in 2009 it’s the best and then it’s okay for a couple years and then it’s absolutely the worst in 2011. Then it’s the best in 2012 and in this past year it’s down near the bottom again. That is all over the place but right there in the middle you’re going to see that the diversified portfolio, the asset allocation thing there is sort in the middle. It is never the highest, it is never really the lowest and that is one of the things that diversification has to do. If going forward into 2014 we know which asset class was going to be the best one to be in, of course we would move 100% of our assets. Unfortunately, we never know that going forward because we can only look in the rearview mirror and say this is the one that I wished that I had. Beating yourself up over it doesn’t help and then taking that and assuming and extrapolating that into the next year just rarely works.

I am going to throw another chart up onto the screen there and what you’re going to see is that over the last 62 years. This is all the way from 1950, that green bar there on the left hand side is the range in one year that some stocks in one of those years, it took two years when the stock market index went 51%. But also one year, it lost 37%. If it was bonds, the very best was that 53, the very worst was 8, but a combination of the two is that last one of 32 to 15. As we go out five years, what you’ll see is you’re starting to normalize your returns and start to get low or high but also higher lows, which is usually what people are looking for. Of course, if we can have our cake and have all of the high highs and of course the highest of lows, that would be a perfect world but when we go out 10 years and then 20 years, what you’ll see is a diversified portfolio starts to get rid of that uncomfortableness of the huge year by year fluctuation because when you have that huge decline on a one year, most people take that the next year will also be a huge decline.

When we look back to the beginning of 2009, March of 2009, that was kind of a low for the market after that huge horrible fourth quarter of 2008 and the first couple months of 2009, most people were not thinking wow the US stock market is what I want to buy into. That is not what most people were thinking but that is actually in hindsight the best time to buy. What I’m hoping that people will not take away from 2013 is that diversification has no value and that is a big joke. That is not the case. A portfolio of stocks and bonds and cash and then of course other types of asset classes that surround it, historically have had the effect of reducing some of the volatility in the high highs and the low lows over time and it creates in my opinion a better portfolio.

One of the concerns that I have is that so many unsophisticated investors will only look at 2013 and dump all of this money in 2014 into just that one asset class which is the US stock market or the unmanaged US stock market index either through an ETF or a mutual fund or an indexed fund or something like that for the wrong reasons. Not because they’d really thought it out but they’re going to have unrealistic expectations and that is unfortunately probably going to come back and bite them. Maybe not in 2014, maybe not in 2015, but if they come with these unrealistic expectations without a diversified portfolio—if I’m wrong, they’ll have nothing to stand on from a diversification point of view to offset what that wrong analysis was. That’s it.

There is so much in the news right now, most of it about the impending debt ceiling crisis. Most of what you read, hear, and watch is sensationalized (in my opinion), so in this quarter’s video I basically dissect where we are right now, paying attention to the data points that I think are relevant.

Being the contrarian I am, I also address some common, assumed facts or assumptions that I simply don’t believe.

A longer than normal video, but let me conclude by saying I’m still optimistic, and not freaked out (unlike pundits on TV).

Click on my video to get my thoughts

Transcript:

Hi, there, clients and friends. Mike Brady here with Generosity Wealth Management, a comprehensive, full-service wealth management firm headquartered right here in Boulder, Colorado.

Today is going to be a little bit longer video than is normal. This is a third quarter review and fourth quarter preview.

We’ve got about two and a half months left. You’re hearing all kinds of news—on TV, radio and print. I want to kind of debunk some of the things that you’re going to be hearing about. Because this session is going to be long and a little more technical and I might go a little bit faster just because I have so much to cover. I’m going to give you all of my conclusions right up front.

If you want to turn my video off in the next 30 to 60 seconds, you can.

Right off the bat, I’m not freaked out as in one of those just about to go off to this huge cliff in a week or even two or three weeks due to anything that the Congress is doing.

There is a momentum that is being built up on the private sector with available cash that we are going to I believe from an investment point of view come through this fine. It is not unusual for us to have various conflicts—whether or not it’s an international conflict or whether or not it’s our own Congress and the President having a dispute. I am not freaked out.

I’m going to debunk here in today’s video something that you might hear from an investment point of view and then we’re going to try to prove that and that seems a lot but here’s my summary is that a rising yield could not necessarily mean that the market’s going to go down and the bond markets in particular.

The economy—if the economy goes down or slows due to anything that the Federal Government might do, that does not mean that our markets are going to go down. The economy does not equate to the market. You felt that the last three or four or five years, the unmanaged stock market indexes have done very well, but yet the economy has muddled through and that’s just one proof. I’m going to give a few other proofs of that as well.

P. E. ratios are not everything. Consumer confidence is pretty much meaningless I my opinion. Warren Buffet is not infallible. He’s out there talking about certain things and sometimes I disagree with him. I think he’s a brilliant individual, but it doesn’t mean that he’s God and that everything that he says we have to take as God’s word.

I do believe that the increase in the U. S. debt as it relates to as a percentage of our national GDP over the long term does provide a headwind that will dampen some of the opportunities that we have in the investing community.

That is something that I think long-term, but it doesn’t mean that it happens next week. Doesn’t mean it happens next month.

Time is your friend and that declines are normal. If you have been watching my videos and if you are one of my clients, hopefully that you have a portfolio of stocks, bonds and cash. Sometimes the stocks do well. Sometimes the bonds do well. They kind of mesh together. You might have some satellite holdings as well.

Stick true to what is the investment strategy for you so that you can sleep well at night. Understand that everything that you hear on TV and the news is not necessarily the truths and that in my opinion, the sky is not falling no matter what they want you all to believe.

If you want to turn off the video, that’s fine; but now we’re going to talk about it a little bit more in-depth with lots of facts to prove—I don’t know about prove—but to give some analysis to you about why I’ve come to the conclusion that I have. My clients expect me to give them straight answers. If I don’t know I tell them I don’t know.

The market has a tendency to go up, sometimes it goes down and sometimes it consolidates. Up, down, sideways. Those are the only three ways that it can go.

Up on the screen right now, you’re going to see it for the last 112 years. You’re going to see times when it has consolidated. You can see times when it has advanced and at times it has declined, but it has recovered.

Time is definitely in your favor as an investor. One thing you have to ask yourself is are you an investor or are you a speculator? Time is something that hopefully we all have, even if you’re going to retire next year. Even if you just retired or are in the middle of retirement. Hopefully, you’ve got a long life expectancy. So, not outliving your money is one of your goals; but also possibly grabbing income from it.

One thing as you look at that graph right there is you’re going to see the last 12 or 13 years. The question is that a consolidation or are we about to take off into one of those advances? Nobody knows 100% for sure, but I am more in the optimistic mode than I am in the “let’s jump off the ledge” and everything is going to be horrible.

Here it is over the last 13 years or so. You’re going to see up, down, up, down, etc. That last little bit is about March of 2009. I think we all know that friend, perhaps you were it and said oh my gosh, the market can’t continue to go up as it goes through the Dow went through 10,000, 11,000, 12,000, 13,000, 14,000, etc.

Sometimes it would go back down and that person would say, see I told you. I told you it was going to go down. Well, you know what, this is the same person who might have been in cash the entire time and this is the up and the down. Declines are a part of the market. As I mentioned, it goes up, down and sideways. You’ve got to be willing to take all three of those and you can’t expect for it always at all times to go just straight up.

The economy does not necessarily mean that the market will do the same thing and that they correlate and go in the same movement. If what happens with the debt ceiling slows down the economy in some way, which I don’t know that’s going to happen. There is certainly a lot of pundants out there who seem to know exactly what’s going to happen, either on the left hand or the right hand, what’s going to happen.

I don’t know. I just admit that, but here up on the sheet there, you’re going to see as an example of what I’ve just said, unmanaged stock market returns from various countries, Europe, Pacific, France and Germany and Brazil and Russia and you’re going to see that a lot of them are double digits. I’m going to tell you that Europe is very sick from an economy point of view.

This graph right there and that which I’ve circled, you’re going to see that in the last two or three years or so, we’ve had a declining year-over-year percentage return on the GDP for Europe as just one example. You’re going to see that on the right hand side that unemployment is in the double digits for Europe.

The economy does not necessarily mean that the market is going to go down if the economy goes down. It is definitely a headwind and I’d rather have it as a tailwind, something to help. If all other things—the amount of cash that’s in the economy—if other factors are pushing things so that the investments are going up, then the economy might be holding it down a little bit, but it doesn’t mean that perhaps there’s so much momentum on the investing side that it overcomes any other factors might have on it. It’s not just that oh, this is the negative. Wait a second. There are some positives as well.

The question is how does it net out? Some people might say the headwind from a bad economy or something that the government might do is going to negate all of the amount of cash that we’ve built up and all the balance sheets that are in corporations. The holding invasion is going on right now. I’m just not in that particular camp.

Another thing you can hear an awful lot about is the Fed. We have a new nominee. Her name is Yellen. They’re going to call her the dove because she will very likely keep a very loose monetary policy, meaning that there’s going to be lots of cash available for loaning and she’s very accommodating towards that. If the economy does have a tendency to slow down and muddle through, my guess would be that she’s going to maintain that low interest rate and maybe even increase some of those bond purchases. We’ll have to see, but I think our loose monetary policy is going to continue.

Interest rate yields have been increasing significantly in the last month. Here’s a graph here showing over the last 20 or 30 years or so, even longer than that, you can see that they’ve really gone down during that timeframe. Yet in the last two, three, four or five months, it has increased. However, just because the yield on the 10-year right now is around 2.64% or 2.65%, it’s not until it gets around 5% historically that has really caused a negative impact to the degree that while if it is continuing to increase, the market is going down.

You’ll see that on this graph right here. There’s a lot of number there. Essentially what you are seeing there is that dotted line right there in the middle is the 5% mark. As the interest rates continue to go up, the yield, the unmanaged stock market indexes went up as well.

Only once when it hit over 5% did it cause such a drag on the available capital for investment and for improvement that it started to hurt the U. S. stock market. We’re still far from that at 2.64, give or take. That’s what it is as of Thursday when I’m doing this video.

Another thing that I want to talk about is you’re going to hear about consumer confidence and that consumer confidence is up or is falling, etc.

I put no credence on consumer confidence. I’m putting that chart up there. You’re going to see that sometimes with consumer confidence that is low is when you would have liked to have invested 100%. Sometimes when it’s high, it’s a lagging indicator and people feel really good about things.

By the way, the University of Michigan only surveys 300 to 500 people on one day over the month. So it’s not a very big sample in my opinion and I put no…I don’t care. I don’t care about the consumer confidence and hopefully, you don’t care as well.

You’re going to see right here on this map graphically people are feeling good right now and it’s because we’ve had a little bit of a housing bump up in the last two or three years or so. That is one more proof that interest rates are probably going to remain very low because we have a housing recovery. People are feeling really good and they have a hard time seeing how they’re going to increase the rate from the Fed in a very short timeframe.

That and the fact that we have so much federal debt out there that we have to finance, we have to keep the rate at a very low rate. I do believe that’s probably going to stay low.

I do think that it’s very reasonable for companies to have accumulated corporate cash over the last two, three or four years. Right here on this next graph, you’re going to see deploying corporate cash at that very high level. Companies have been very rational in keeping their cash ready to invest when they sense. This is a good thing.

In cash return, the shareholders are also at a very high level. The amount of dividends that are paid out. There’s a lot of cash out there for those investors on the sidelines ready to jump in.

You’re going to hear a little bit about P. E. ratios and other things. Right now, I’m not concerned that it’s too low or too high.

I think it’s going to be just fine. This graph right up there. You’re going to see that when that dotted line from top to bottom there. Many times when it’s at this level, the returns for the stock market indexes have been positive. Sometimes they’ve been negative. You can see that. A large preponderance of them have been up on the top side. Only when it gets up to a 20 and 30 time does it really, really get way out of whack.

The next thing I want to talk about is that I do believe that Warren Buffet has been talking about the U. S. debt as a percentage of our GDP which is really our national income for the country not concerning to him.

Right now, it’s at about 102% or 104% and I do think that long-term, it provides a headwind against the investing and the ability of that particular country in order to move forward because it is, of course, sucking out the available capital to finance that particular tax.

You’re going to see here on this graph that I’ve just put up there that the U. S. is kind of on the right-hand side of that 100 mark. You’ll see that as you go down, Greece and Portugal and some other countries that are really an absolute mess as their debt got bigger and bigger and bigger. It’s not by the size, by the way. That’s what the yield is. The yield comes after some of the problems.

For right now, just really look at how the U. S. is on the right hand side of that vertical line, which is not the side that we really, really want to be on.

At this point, I do want to start summarizing which is time is your friend. On this graph right up there, you’re going to see is a depiction. The green is the range over the last 52 or 53 years of the unmanaged stock market index. It’s very high and very low.

Bonds, high and low.

Then we have a 50/50 mash of the two.

What you’ve seen is on an annualized basis, when you get out to five years, ten years and even twenty years, you have a normalizing return. You’re also seeing that they have a tendency and historically have been and that’s the only thing we have to go on. The future could be different, but historically what has happened is that those returns those people have been patient for five years, ten years and twenty years have had positive returns or even break even. There are not that may opportunities over a very long timeframe for there to be a decline.

One of the frustrating things is with this low interest rate environment, the options are very few I should say.

CDs and your money markets are hardly paying anything.

Bonds have a very low yield at this point. Unfortunately, many of us have been moved towards higher risks that we might not otherwise have taken.

Coming to a conclusion here, the last chart I want to show is right up there on the screen. It is the annual return. It is normal for there to be declines throughout the year. This year, believe it or not, has had from a top to a bottom, an unusually low top-to-bottom draw down. It has either been more up or sideways this year. Not a lot of huge decline on the down side.

It does not mean that when there’s a draw-down throughout the year that the year was all negative or that everything is just going to heck.

This graph is very important because we as investors who are in it for the long term who have hopefully created a portfolio that’s consistent with our risk levels and our objectives, etc. We have to understand that there will be some volatility in the market.

If you can’t handle that, we have to really seriously evaluate the strategy that you have. That is what I have here today.

Please give me a call if there are any concerns whatsoever. I can talk your ear off about some of my thoughts as we go forward and strategies that we should have or could have.

Mike Brady, Generosity Wealth Management, 303-747-6455.

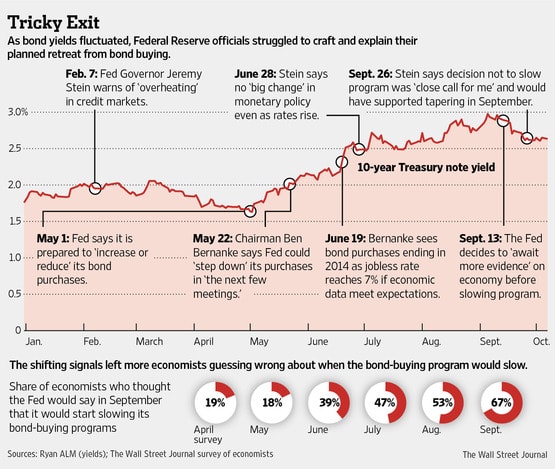

As I mention in my video, the price of bonds (in general) have decreased causing yields to increase. The above graph shows comments from the Fed which has led so many people to have speculated they’d cut back on the bond buy back.

As of last month, the Fed Chairman has stated the bond buy back will stay in place.

For more graphs and a discussion, here’s the full article.

In my video today, I ask the question “is it time to run for the hills, or jump off the ledge?” because of the recent increased volatility and decline in the markets.

Let me give you the short answer: no.

The bond correction was an over reaction, and the most recent equity dip is not a precursor to some big decline. At least not in my opinion.

For a full discussion of this, listen to my short video where I expand on these ideas.

Hi there, it’s Mike! Friends, Mike Brady here with Generosity Wealth Management – a comprehensive full service wealth management firm right here in Boulder, Colorado and today’s conversation is about whether we ought to run for the hills, find that ledge, and jump off it, because if you’ve been watching or reading in the news recently the volatility has gone up in the unmanaged stock market indexes and some of the bond markets as well.

They’ve decreased and the answer is no, I don’t believe that we should jump off that ledge and I think this is a short term correction to what we’ve seen. Let’s talk about the unmanaged stock market indexes first and foremost; your S&Ps, your DOWs, your NASDAQ, etc. I’m going to put a chart up there on the screen and if you have been watching my videos for a long time, you’re very familiar with this chart.

It is normal for there to be intra-year decline throughout the year, going back years and years and years. Every year there is one and every time there is one, we always freak out and forget that that’s a normal thing. I think this is going to be one more of those normal things, not the beginning of some huge decline where we lose 20%, 30%, or 40%. I just don’t see that with all of my analysis.

I also think that it’s going to be relatively short lived as well. Let’s talk about the bond market. The yields have spiked up in relation to the bond prices going down. Back in June, Ben Bernanke was the chairman of the Federal Reserve. He made some comments about starting to taper off. Now of course, he’s taken all summer to kind of back off some of those comments, but essentially let’s think about money in the economy as money in a bowl.

Here, kind of look at my hands there. Money in a bowl. You could put money into it; you can take money out of it. For the last four or five years, we have definitely been putting money in there by decreasing the interest rates, but also doing a bond repurchase. What he said back in June was not that we were going to start taking money out of it, but if we’re stop one of these two levers of putting money in – the bond repurpose.

You just said we’re going to put in – we’re going to buy left backs or we’re going to put less money in. Also, there’s an accumulated amount of sums and money in there already. I think that the concern isn’t overreaction and it took us a long time to fill this bucket with a lot of money. It’s going to take a long time for that impact to really be felt. At this point, there’s money in there for banks to lend out and they are definitely doing that at this point.

I think that the reaction even on the bond market, is an overreaction and I’m not freaked out about that as well. It is important to have a portfolio that has both stock and bond components in general, being very general, each client is different of course. The percentage that you have in those two of course is specific to what you’re trying to do with your particular strategy, whether that’s your retirement strategy or growth strategy and income strategy, etc.

The mix between these two, some things zig when the others zag. At this point, the equity markets in general have that. All of the bond markets in general have been down so they’re going to compete in force this year. In previous years, it’s been reversed where the bonds have done well and maybe sometimes the stocks at various points have gone down, so having that mix makes a lot of sense.

I’m going to end this video with something that I really like from Warren Buffet. Back in 1975, he wrote a letter to Katharine Graham who owned the Washington Post and he basically told her to keep the long view, the long picture in mind. Think of it as he wrote in the letter of a thousand coin tosses and there are going to be times when five or 10 of those are going to be in a row all head or all tails.

You might see it all-sided one way or the other, but it really is just a short time frame that does go back down to normalization. It’s the same way when we’re looking at investments. We’re here for the long term. We shouldn’t get too excited if there’s a month or a quarter or even a year that’s off. They do have a tendency to go up and down in value.

The reason why we have investments, of course, is that we assume that the future value will be greater than today. Whether that future value is five years, 10 years, 20 years – whatever it might be. Otherwise, why would we have investments? Why would you put it in there? You’d put in your master of storing in the bank savings account.

It’s important to take that into consideration that there are times both five to 10 coin tosses as Warren Buffet says, but we’re really kind of looking at it as we’re building this portfolio up together that works for us with our particular risk tolerance level and what you’re really trying to achieve. You’ve heard me, ad nauseum, talk about how important the strategy and the retirement analysis and the plan is and that we then use managers and other investment vehicles in order to support that particular strategy.

Let’s keep our eye on that particular strategy.

Mike Brady, Generosity Wealth Management. There was an awful lot here in a short amount of time, but I like to make my videos short, and pithy, and to the point. Hopefully today I achieved that.