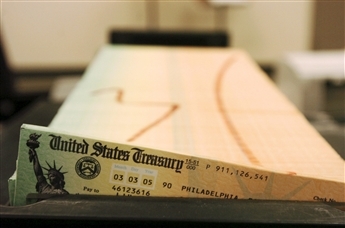

$1 Billion in Unclaimed Life Insurance

1 out of every 600 people is the beneficiary of an unclaimed life insurance policy.

Could it be you? How do you search and find out?

Click on the link for some suggestions.

1 out of every 600 people is the beneficiary of an unclaimed life insurance policy.

Could it be you? How do you search and find out?

Click on the link for some suggestions.

I was recently asked “what are some characteristics or traits you’ve noticed in people who seem to reach their goals?”.

Hmmmm…..good question.

I suppose I could be completely self-serving by saying “they click on my videos in my newsletter” but that’d be too obvious.

So, I’ll start off by saying “they treat their life and goals like a business”.

For the rest, you should watch the video.

Good morning. Mike Brady with Generosity Wealth Management, a comprehensive full-service wealth management firm headquartered right here in Boulder, Colorado, although I have clients in many different states.

Today, I wanted to ask a question that a client had of me. They asked after reading the book The Millionaire Next Door, it was like, “Mike, in your over 20 years of meeting with clients, hundreds if not thousands, what are some of the characteristics that you’ve seen that are similar to those that have achieved their goal? People who perhaps 20 years ago you met and they stated what their intention was and then they were successful in reaching their goals, and others that were not successful.” I want to answer that question here today. By the way, read that book The Millionaire Next Door, because you’re going to find some habits that this book talks about that people with very good balance sheets that have worked hard for their net worth, but they have many similarities together. That’s really kind of what I’m talking about here today but just more of from my anecdotal and observational experience.

The first thing is, they treat their finances, their goals, their retirement goals, etcetera, as a business. They have a good conversation with themselves and with me and with their spouse and perhaps their family about where they want to go, and they have a plan; they have a goal, they have a plan and they review it periodically and that could be within the year, maybe annually, maybe every other year just to track where it is that they’re going. They also understand the relationship between income and expenses, saving and investing. You’ve seen me do this before. This is your income and this is your expenses and the difference between the two, the income has to be greater than the expenses. It’s that simple. If you don’t know if your expenses are equal to your savings or if they’re even greater, than that’s the first warning light on the old dashboard that you might not be setting yourself up for success.

No matter how busy a client is, whether they’re a doctor, a lawyer, a business owner, or a family with a bunch of kids, the people that I have found have been very successful treat their life like a business. I have to say one indication of that is they a lot of times return paperwork very quickly. They have prioritized up all dealings with their finances and reaching their particular goals. That could be educational goals for their kids as well. That could be providing for older members of their family you know, etcetera. Whatever those goals are they have made a real priority, they’re organized, and they address it accordingly and in a timely fashion.

Another thing is they are engaged. They review paperwork, they ask good questions, and they’re more engaged and that’s one thing that I’ve found is common amongst those that reach their goals. Then the last thing is a little self-serving and I’m just going to preapologize on that one, but they have good advisors and they have an estate planning attorney, they have a CPA, and they usually have a good financial advisor, and hopefully that’s me of course, that’s my observation. They listen to them, they ask questions, there’s a true dialogue, a relationship, a collaborative relationship, and they have a tendency to follow that advice particularly when all of those members are working together, agree on how to go forward and they have good advisors and they recognize the value that they’re bringing. Those are some things that I have found in my over 20 years of working with people, and I can many times tell starting off when I meet someone who doesn’t become my client whether they have the right habits or not just by the fact of whether or not I ask them for the data to do a financial plan and they can’t even pull that together. I really question at that time how serious they are about their goals in order to get a plan and then of course to review it.

That’s it for this week. Mike Brady, Generosity Wealth Management, 303-747-6455. If you’re my client, I love you. If you’re not my client, I would love to talk with you and hopefully we can both love each other and help each other out.

Unfortunately, there is a perception by many Americans that Social Security will be a bedrock of their retirement, when in fact it is just a complement, and usually a small one at that.

According to the Congressional Budget Office, someone retiring at 65 today will receive 43% of his/her annual income from Social Security. Where does the rest come from? Your investments and savings, additional job, or significantly reduced standard of living.

Which would you rather have? Call me if you need help determining a retirement strategy.

For the full statistics on this, click here

Collect Social Security early, late, with your spouse, alone, etc.?

The following article is a rather detailed discussion for ways to use and plan for social security.

Things that I go over with clients all the time.

One of the best, most useful articles in a long time.

How about applying that to your financial plan?

Save 20% every year and live off only 80%.

Let that 20% work for you for your retirement.

Many times I’m asked what my rich clients did to get that way. Invariably I say that the majority spent less than they made, saved it, and invested wisely.