Recent headlines about global conflict and market volatility can make investing feel uncertain. When emotions rise and news cycles move quickly, it’s easy to feel pressure to react.

In this video, Michael Brady of Generosity Wealth Management shares a timeless perspective on navigating moments like these. Drawing on decades of experience, Mike explains why emotional control and discipline are two of the most important ingredients for long-term financial success.

Markets will always experience ups and downs. Geopolitical events will always occur. The key is not predicting every headline, but building a thoughtful plan and maintaining the perspective to stay on course.

Mike also shares a helpful reminder: intra-year market declines are normal, even in years that ultimately end positive. Long-term investing is about progress over time — not reacting to every moment of uncertainty.

At Generosity Wealth Management, the goal is to align wealth with purpose and possibility, helping clients live well today while preparing confidently for the future.

Transcript

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive full-service financial services firm headquartered in Boulder, Colorado. Although I am in Michigan right now, if you’re ever wondering what my childhood backyard looks like, that is it. My mother’s in assisted living. She moved there over the summer, and I’m doing the last little bit in my childhood home. My parents have had this house for 50 years, and I’m helping do the last little bits in order to put it on the market and close that chapter.

I did a video about a week ago that was going to go in this newsletter. But it did not get sent out because I’m replacing it with this video. While we were editing the newsletter, the Iran–Middle East conflict came up, and I thought I’d be a little more timely and remind you of certain lessons that are tried and true.

One of them is that we have emotional control at all times. If you want to be successful in the financial world and reach your financial goals, it is my opinion that one of the first things you do is have emotional control. Remember that the media—whether it’s print, scrolling, or TV—often tries to elicit emotion from you, not necessarily inform you. If you’re getting excited or upset, check yourself.

One thing we can do is ask, “How am I feeling right now? What’s causing that? If it’s not helping me, stop doing it.” It’s just that simple.

The other is discipline. Have the discipline to know what our plan is and move towards it. Periodically I hear people say, “Well, we’re obviously at a high.” First off, when the word “obviously” is in anything in our industry, you know it’s not obvious. But the question is, are we at a high in the unmanaged stock market indexes? The answer is, we might be at a high from where it was 5, 10, and 20 years ago. I certainly hope it’s at a low in comparison to where it will be 5, 10, and 20 years from today. That’s all that really matters, because we can’t live in the past, but we certainly can live, and we will hopefully live, the future. Why else would we have investments if we didn’t believe that they would be higher 5, 10, and 20 years from now?

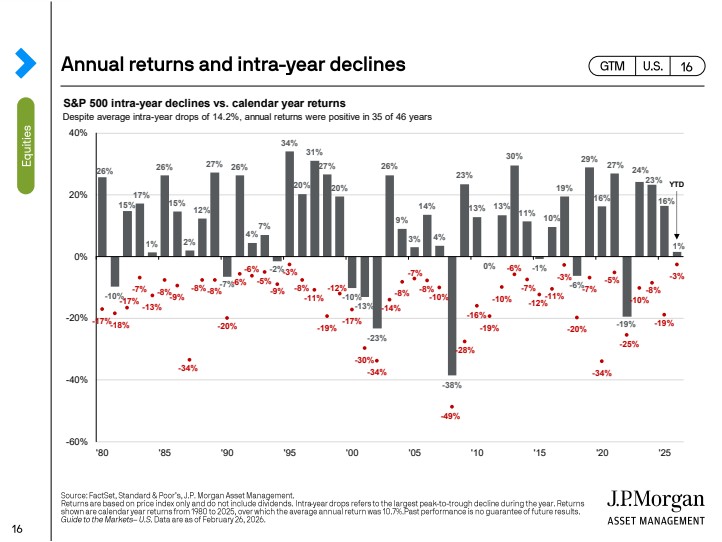

Up on the screen is something that I like to remind people of: the numbers below the X axis are the intra-year decline, and it is normal for there to be declines throughout the year. It doesn’t mean that the end of the year ends negative. It is normal for there to be declines.

Someone asked me the other day, “Mike, your videos are not very technical.” And my answer is yes, that’s by design. If you want technical, you can go to any business news channel and get that technical analysis. You can open up print media or a business magazine or newspaper and have all kinds of technical analysis. Twenty or thirty years ago, I could wow you with that information and charts. Today it’s all free and available. But what is more important than all of that technical data is what it actually means. What are the ingredients for success that they might not be talking about in the media or that you might not see others talking about in your neighborhood or community? That’s what I’m here to present: what I believe, and my beliefs have come from decades of experience in discipline and emotional control.

Know your liquidity, have your duration in mind, and then execute properly. Money that you need in two weeks is certainly different from money that you need in five, ten, or twenty years. Even if you’re in your 60s or 70s, we hope that you will have many five- and ten-year timeframes going forward.

I want to bring us back to the fact that geopolitical events will always happen. The market will always go up and down historically. The way I believe is that if you’re so averse to risk or so afraid of any kind of decline, you’re not going to get the ups. It’s three steps forward, maybe two steps back. Three steps forward, two steps back, but you’re progressing along a path. It’s no different than if you’re so afraid of a relationship—friendship or romantic—of being hurt that you’ll never find true love. It’s the same when trying to reach your financial goals. We need to mitigate risk; we can’t eliminate it.

We have to ask, “What’s our duration?” Are the investments we’re in consistent with what we want to do? Can I keep my emotional control, and am I disciplined when things happen that I know are going to happen, like the market going up and down or geopolitical issues or things in the news or in our own country? These things have always happened, and they will continue to happen. How am I going to react?

Is the purpose of my money to make me happy? I would say yes, to live your life so you’re not a burden on others. Your purpose and possibility is really what we talk about—Generosity Wealth Management aligns wealth with purpose and possibility. If that’s the case, then let’s get immune to those external things and stay with our plan. Be peaceful and calm in sometimes non-peaceful situations in the world, but we can be our own oasis.

So, Michael Brady, 303-747-6455. Give me a call or send me an email if you ever feel like you want to talk about something. Let me know, and we can have that communication. Have a great rest of the day, great week. Bye.

2025 reminded us of something easy to forget in noisy markets: certainty is an illusion. With 24/7 news, constant opinions, and confident predictions everywhere, it’s tempting to believe someone knows exactly what comes next.

They don’t.

At Generosity Wealth Management, we believe the real value isn’t prediction — it’s perspective.

Transcript

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered right here in Boulder, Colorado. It is the end of 2025. So this is my 2025 review, and I would say it’s more lessons learned, because you can have all the technical information about 2025. You can read it, you can watch it on TV. I mean, when I started in this industry 34 years ago, you know, it was hard to find that information. People genuinely didn’t know. Now we have 24/7 news and the Internet, and I’m just telling you, you can read more analytical stuff than I can provide you in this particular video and this newsletter. So I want to do it at a high level, but I also want to do the 2026 preview, which is very light because I don’t believe in that. I believe that the future is inherently unknown. And so we’d better have some conviction, some foundation, some base that is, you know, key that we need to remind ourselves about. And that’s more important to spend that money than trying to guess what 2026 is. Because frankly, I could flip a coin, you could flip a coin, and one of us is going to be right. I mean, it’s that simple.

The problem with many pundits is that they are trying to be very exact about something impossible to be exact about. The way I like to think of it is the economy and the stock market. It’s not math, it’s not physics. It’s more like biology. Math is A plus B equals C. Physics is, hey, these are the rules of physics. Biology, that’s the economy, and that’s the investments. You know, even the smartest doctor is not quite sure what’s going to happen because it’s so complex. There’s so many variables. Well, wow, the other people I gave this poison to, they died, but you’re doing okay. Or the other way around. An antidote that might work for you doesn’t work with somebody else. And side effects and counteracting. That’s why anesthesiologists get paid so much money, is they have to keep all these different—you know, this thing helps and this thing hurts—and you know, on balance, this is the way, you know, hit these dials to help a client out.

So, you know, the economy, the investments, they’re like biology. It’s like a body. It’s a very complex system. And so, I’m hoping that one thing that we will take away from 2025 is some humility up on the screen.

I have shown the intra-year, and I’ve just circled it: all those red numbers, that’s how much a decline was within that year. And you’ll see that it is normal for there to be a decline of over 10%. Double-digit declines. That’s normal. And this year was no different. The S&P 500, which is an unmanaged stock market index, was down 19% at one point this year, but the year did not end with a negative 19%. You can see throughout the graph that, on average, three out of four years are positive, and one is negative. Okay, sometimes they’re strung together, you know, negative, negative, and then positive, positive. There’s a whole number of different ways that it can play out. But on average, when you hold it for a long time, three out of four are positive, and one out of four are negative. But almost every year has a negative decline throughout the year, so we shouldn’t be surprised when it happens. What’s very frustrating about this year is that the sky-is-falling crowd comes out, as it did in March and in April, but with so much confidence. Not the, well, I think this is going to happen, I think this is going to be the impact—it’s definitive statements of it will, and that’s just not true. I hope that we take away from this year that that which you hold with such conviction is sometimes wrong.

I have humility in what I do with clients all the time. Now, I might hide it. Okay, I mean, those of you who know me well saying, wow, he talks with a lot of confidence. Well, I talk with some confidence because I’ve seen it, 15,000 trading days since I started. When I started back in 1991, in August of 1991, the Dow was at 3,000. And then I heard people say, wow, it could never get above 5,000, never get above 10,000, 20,000, 30,000, 40,000. I mean, every single time it’s obviously at a high; well, it obviously can’t get any higher. Well, you know what, I’ve heard that my entire career as it went from 3,000 to 5 to 10 to 15 to 20, all the way up to where we are today. The Dow Jones, which is an unmanaged stock market index. This year, almost every one of those unmanaged stock market indexes were positive across the board—S&P 500, bond indexes, international, you name it. It was a very good year, despite what all those people on TV and all—if you’re doom scrolling on your Internet news feed—say how everything is going to be absolutely horrible. Many of those same people might be saying the same thing in 2026. They’re just trying to be right. Oh my gosh, I can’t say that I was wrong, it just hasn’t happened yet. Well, whatever.

I believe that if you don’t think that five years from now the market is going to be higher than it is today, why would you have any investments? If you don’t believe that, move it in cash, for goodness sakes. Okay? So I don’t know if this next year, 2026, will be negative. I don’t know if 2027 will be negative. But I feel with high confidence—but no guarantee—and I feel with high confidence through my experience and the experience of others over a hundred years that it’s a good bet that I will win on that if I have investments properly matched to me and my emotional level, my goals, okay, my risk level, that five years from now it’ll be higher. Whatever mix that I do, why else would I have investments? Let’s keep our eye on the ball. What happens in a month and a quarter doesn’t really matter. We keep our eye on that ball.

So one of the things that I recommend and I repeat over and over again is emotional control. If you don’t have emotional control, I don’t know what to tell you. People are going to whisper in this ear, and they’re going to whisper in that ear, and you’re going to move this and this and this, and you’re going to be so flexible that you’re really bendable, and you’re not going to be happy. The way I like to describe it is, you know, one person worried every day throughout the year, another person didn’t. The returns are exactly the same. One person just had a very poor journey, the other one believed in the system, had their thing, and executed it. So knowing what your purpose is—I mean, Generosity Wealth Management, I want to be very clear on this: we align wealth with purpose and possibility. What that means is we use wealth to help you. What is your purpose? What do you need today? What do you want to have happen so that you can be generous with yourself? What’s your purpose with your family? What’s your purpose in your community? What’s your purpose maybe in the future, but what’s also possible that you haven’t even imagined yet? Okay, so let’s have that conversation. That’s what the value is of Generosity Wealth Management. We help explore that and bring alignment of wealth with purpose and possibility, and we do that in a number of different ways.

I want to talk about one of some of the things I’m very proud of in 2025 is we really upped our game as it relates to retirement analysis. You need to know what your number is. You need to know how these balls in the air come down into an equation that leads to the outcome you want. And hopefully it’s positive; let’s try to avoid the negative. But what can happen proactively so that’s not just chance? What are the things that we can control? What are the things that we can’t control? And the wisdom to know the difference. We really upped our game as it relates to tax planning so that we can provide you with our thoughts, some talking points that you could have with your tax professional. I’m not a CPA. But I work and brainstorm at a very high level with you and with your CPA, because I believe that this is something—it’s most people’s single biggest expense: taxes. So you’ve got to be an expert in it. Retirement accounts outside of your house—it’s most people’s single biggest asset. I have to be an expert in it. I joined the Ed Slott Elite Advisors, and I’m very proud of that. My knowledge has dramatically increased. And of course, you’re the benefactor of it. And I want you to ask me tough questions. I want you to talk about me with your friends and work colleagues so that they know that they’ve got an expert that they can come to. I work with business owners, I work with people who are retired and not retired. I want to work with good people who I like, like you, if you’re my client already. Because I got to tell you, this is the truth: there’s not a single client that I have that I don’t like, that I don’t kind of look—and there’s no client that is like, oh God, I got to pick up the phone, or I got to give them a call. No. Okay, they weed themselves out. I spend a lot of time at the beginning of a relationship to find the people that maybe were not a right fit, and that’s okay. I want to attract the right people. I don’t chase people, I attract the right people, and then we kind of date. We decide we’re going to be right for each other, but if for some reason we screwed up, I kind of help you find that, or you find out on your own that maybe we’re not right for each other. So I want to work with people that I have lots of chemistry with, they have problems that I can help, that I can provide value to you first, so that of course, you can see the value in what I’m bringing as well.

2026 I want to summarize. I don’t know if it’s going to be up or down for the unmanaged stock market indexes, but I do know the value of diversification. Knowing what your purpose is and what the duration of your money is, is important. I know that discipline, okay, whatever that discipline, and emotional control, I know that these things—every year, I could say 2026 or I could say 2023 or the year 2000—they’re the same throughout the years of my career. These things I keep coming back to, and also, of course, humility. Hey, we don’t know everything, so let’s do the best job that we can and keep control of our emotions as we move forward.

I do want to have more clients. So if you—my client, who I love, all right, who I am willing to jump on a phone call and a Zoom with and give you the best advice that I can, and the experience of what has worked and not worked with other people—if you know friends, family, work colleagues that are just like you, I want to replicate you. Then have them contact me, and we’ll determine independently if it works out. I am going to expand my business. We’ll talk about it—not today—but I have new and fun and cool things that are in the pipeline that you will hopefully see, and I’ll roll out to you in 2026 and even into 2027, and that is all in service of the client, because when the client sees the value, if I make you a raving fan, then you will talk to other people, and that’s how my business grows. And of course, as I bring in other junior advisors and replicate some of the knowledge that’s in my head with them, to serve you continually, that’s how we can be of benefit to the community. And you’re part of the Generosity Wealth Management community. Felicia and I, Sarah Cassidy, we thank you for being our clients, and we just really want to have a wonderful 2026, and we’re glad that we’re doing that together. So, Mike Brady, 303-747-6455.

As 2025 nears its end, Generosity Wealth Management founder Michael Brady takes a moment to pause — not just to reflect on a strong year for markets, but to share insights on what truly drives long-term financial success.

In his latest video update, recorded just before Thanksgiving, Michael discusses why patience, emotional control, and thoughtful planning often matter more than the latest market move. He also highlights his recent speaking engagements in Las Vegas and Austin, where he explored how technology like AI can deepen advisor-client relationships and how tax-smart retirement strategies can build wealth that lasts.

Because at Generosity Wealth Management, it’s not just about managing investments — it’s about aligning your money with your goals, your time horizon, and the life you want to live.

Transcript

Hello clients and friends. Mike Brady here with Generosity Wealth Management, a comprehensive full-service financial services firm headquartered here in Boulder, Colorado. Today I’m recording this right before Thanksgiving. Not sure when you’re going to get the newsletter, as I’m writing the rest of it and adding this video, but it’s been going really well.

From an investment perspective, the unmanaged stock market index is really on a tear. I think that it’s important for us to remember that, from a market point of view, it is normal for the unmanaged stock market indexes to have a double-digit decline that happened earlier this year. Who knows how the rest of the year is going to turn out? But I am always keeping clients focused on what their time duration is and making sure that it matches up with what their goals are. Because, frankly, the investment management part of what I do feels like the simplest part:

Where do you want to go?

Which tool in the toolbox helps you get to what your financial goals are?

What’s your time horizon?

Can you keep your emotions in check?

And of course, avoid stupid stuff.

I made plans for people 20 or 30 years ago, and some met their goals and some didn’t. It usually had nothing to do with investment A or investment B, but it did have to do with some of the abstract, some of the satellites around that core of having good investments, which is you got excited about your brother-in-law’s Chihuahua farm or you did some other investment that sounded great at the time but really didn’t help you achieve your goals. Or it was that you simply didn’t save enough, or you had some other unfortunate incident happen in your life, unable to work, loss of your spouse, things of that nature. That’s why I really want to keep all those things in mind.

Today, though, I wanted to pivot from the investments, which are going great this year, and I’m hoping that 2025 ends in as good a situation as it is right now here in November.

But I want to talk about some of the things that have been going on from a seminar perspective. I just spoke in Las Vegas recently, which was great, and in my newsletter, I’ll talk a little bit about that. I was talking about how I use my note-taking AI to help me be more efficient and stay present in every client meeting. I’ve had clients for 20 years, 30 years, and of course, I’m always bringing on new clients as well. So thank you to those of you who continue to refer your friends, family, and acquaintances to me so that I can help them out. I use my AI note taker because it hears things I might have missed. It really helps me be present in the meeting when you and I are talking, so I can hear what the problem is, what the issue is, and what your emotions are, so I can then, of course, come back with the best recommendations for you. I was honored to be a part of that panel there in Las Vegas, talking about how I believe AI is going to revolutionize the relationship that advisors like me can have with our clients, can go even deeper, and really understand where you want to go so that we can come up with the solutions in order to get there.

I was also recently in Austin, Texas, at an Ed Slott Elite Advisor seminar, and that was training for me. Most people’s single biggest expense, aside from everything else, is taxes. Most people’s single biggest asset outside of their house is their retirement account. So I have to be an expert in everything retirement accounts, and I have to be an expert in taxes, even though I’m not a CPA. I’m not going to do your taxes, but I work at a high level with your tax planner. Now, here’s one thing I like to tell people: do you have a tax preparer or a tax planner? A tax preparer costs you money; that person is a historian. They take your number in that box, put it on that line, and provide very little proactive guidance. A tax planner helps save you money. They are working with you throughout the year and proactively giving you advice. They are in the wealth-maximization business, like I am, not necessarily in the tax-minimization business. I think that’s a really key distinction: they are there to sometimes say, maybe we pay a little bit more taxes this year, but over your lifetime or over multiple years, this is in your best interest. You’ll actually be wealthier in the long run if we pay a little bit more in taxes right now.

This leads to my next conversation, which is satisfaction and gratification. There’s this old study called the marshmallow study, where they had a bunch of kids, around 6 years old, brought into a room and put a marshmallow in front of them. They said, “You can have the marshmallow now, but I’m going to be back in six or seven minutes, and if you wait that long, I’ll give you another marshmallow.” All they had to do was delay their gratification for a few minutes, and they would get twice the reward. Those kids who were able to delay gratification tracked better throughout their lives than the control group, who needed instant gratification. They found that those who delayed gratification had greater life satisfaction, greater career satisfaction, were married longer, had higher incomes, and had higher net worth—all of the things we want in our lives. They were able to do it because they were in control of their emotions and delayed the gratification.

One of the things I talk with clients about all the time is what’s right for you. Is it a Roth IRA, a Roth 401(k), where you pay the taxes now but delay the gratification for the tax-free income all along the way and the tax-free withdrawals? Or do you want that instant hit right now, which is a tax saving today? It’s really an individual choice. We have to individually do the math, but this is something I want to work with you on, and I want to work with your CPAs. My ask of you is that I want to grow my business. I want to help your friends and family and acquaintances, and one of the value adds that I bring is that I really listen to you. I use the AI in order to help my notes—the boring part—so that I can truly be present and hear what you want to do and match up those investments. Here’s the value add: I’m going to really look at what your assets are and position them accordingly, and be an expert in them. Like I said, that’s why I’m continually traveling to go to seminars, to be the absolute expert in your biggest types of assets, and also work with your CPA on your biggest expense, which is your taxes.

If we manage and control that expense and hopefully minimize it over multiple years and over your lifetime, then you’re going to be better off. That’s what I want to do with clients. With that extra money, with those extra assets, what do you do with it? That’s where the generosity comes in, so that you can be generous with yourself, with your family, and if you believe it’s in your best interest and the community’s best interest, you can be generous with your community, both local and global. That’s really what I’m about, and that’s why I’m saying to you: I want to be that trusted advisor. If we keep some of these key things in mind, then I believe that you’re better off, the community is better off, and your family is better off if we keep some of these fundamentals in check.

Michael Brady, Generosity Wealth Management, 303-747-6455. You have a wonderful rest of the year. You’ll hear from me again in January as I recap what happened in 2025 and, of course, as we look forward to 2026. Thank you.

Generosity Wealth Management founder Michael Brady was recently invited to speak at the Financial Planning Advise AI Conference in Las Vegas, joining an esteemed panel of thought leaders to explore how technology is reshaping the advisor-client relationship.

In a session focused on practical AI applications in financial planning, Mike shared how he uses tools like Jump and FP Alpha—not to replace human relationships, but to enhance understanding and trust.

“I’d use this even if it didn’t save me time,” Michael told the audience. “As long as it deepens trust and catches what I miss.”

Mike discussed how AI note-takers and data-driven tools can help advisors stay fully present in client meetings, capturing nuances and emotional context that might otherwise be overlooked. By leveraging technology for administrative precision, advisors can focus more deeply on what truly matters—the client’s goals, emotions, and vision for their life.

“AI doesn’t replace empathy,” Michael explained. “It enhances it—allowing us to listen better, think clearer, and create more meaningful solutions.”

The discussion, moderated by industry experts and joined by Stephen Chien and Lawrence Sprung, CFP®, CEPA®, emphasized how the right use of AI can make financial advising more human—not less.

True financial confidence comes from perspective. This quarter offered a reminder that markets don’t move in straight lines—April’s turbulence made headlines, but as history has shown, recoveries follow setbacks. Michael Brady shares why he remains optimistic, how he helps clients focus on what they can control, and why aligning wealth with your deeper purpose will always matter more than short-term noise.

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive full-service financial services firm headquartered here in Boulder, Colorado. It is the end of the quarter. It has been basically a pretty darn good year except for one month, which was April, which of course got all the headlines. Lots of stuff happened in April, and at this point in time, with the returns for the unmanaged stock market indexes where they are, historically 75% of the time the year ends positive. But you know what, there’s a lot of time left. We’ve got October, November, and December. But I’m feeling very good and very optimistic.

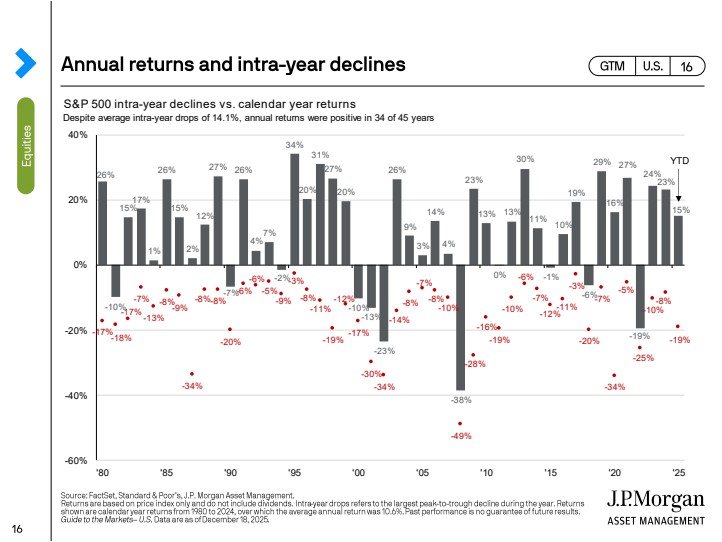

It is important for us to remember the long-term view. The reason why I bring that up is, look at this chart up on the screen, and I’ve just circled what happened in April. When you look at that, that’s multiple years. I know those things are going to happen. But the reason why we have equities, the reason why we have investments long term, is because times like I’ve just circled historically always recover.

I remember back in April, a client emailed me because they were watching the news, and it was all about the tariffs and a catastrophe—the doom scrolling. If you’re looking for negative news, you’re going to find it everywhere you look. It was like, why do I have equities? Remind me again why we have equities? The reason we have them is because of the nice recovery. It was negative 19 on an unmanaged stock market index like the S&P 500 for the year. It is now in the double digits for the S&P. 14% positive for the year. Quite the reversal and overreaction, which I said at the time and which I believe has been proven out.

The market will go up, it will go down. That is the one given that I’m going to express out in the world. If you are looking for negative things, I feel that there are a lot of advisors, a lot of TV pundits who do a lot of fearmongering, a lot of fear-based selling or advice, and that’s never my approach. I believe that every problem has a solution. When a client comes in to see me, I want you always to leave with some hope and optimism, because frankly, for the negativity—and if you’re looking for negativity, you’re going to find it—my job is to find the positive solution in every situation.

When it comes to working with me from a wealth management point of view, it is finding where you want to go, what’s your why, what’s your purpose, what’s your financial goal that we’re trying to get to, and how are we going to get all the balls that are in the air, which is your life? Things that have happened in the past, things that are happening right now in the present, and things that you want to have happen in the future—how can they all be put down into an equation so we can be diligent and proactive about the particular variables in that equation? The equation’s answer is what you want, which is the desired outcome. That’s it.

It’s not all investment related, and it’s not about worrying too much about things that you may not have control over. Let’s have control over the things that we do have control over, which is understanding the aspects of our lives, where we are presently, where we want to go, and how they fit in. Investments are a part of that, but it is only one part.

That’s why I call myself a wealth manager, not an investment advisor. I care about increasing your wealth and helping guide you like a coach, but you get to be the hero. The success and the failure is yours. We are now nine months into the year, and I’m feeling very good about the next three months. But you know what, our time horizon is not three months, so what’s most important is that we have the right duration for you, that you and I communicate very well if you are my client.

If you are not my client, consider being my client.

If you’re one of my clients, please, I am bringing on new clients. I have an infrastructure that supports me meeting with good people that you feel I could help out, like I have helped you out. I will treat them like kings and queens, and I will really do what I can to understand where they want to go and help guide them through the full-service financial services firm that I have, which is Generosity Wealth Management. We align wealth with purpose and possibility, and that possibility is what may or may not even be in your mind right now. That’s something we can explore together. Michael Brady, Generosity Wealth Management, 303-747-6455.

Have a wonderful fall, and I will talk with you at next month’s newsletter as the year continues to unfold. Thank you.

In this quarter’s video, Mike Brady—founder of Generosity Wealth Management and the Generosity Group—steps away from the noise and into the quiet of Wyoming to share something deeper than market headlines. Drawing from 34 years and over 15,000 trading days of experience, Mike offers timely insights on what it takes to succeed in today’s financial world: humility, emotional discipline, objectivity, and a clear sense of purpose.

Whether you’re new to working with us or have been with us for years, this update is a reminder that true financial success isn’t about predicting the market—it’s about preparing for what matters most to you.

Watch the video now to hear Mike’s reflections and the mindset that continues to guide our clients through uncertainty, opportunity, and lasting legacy.

Transcript

Hello, I’m Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered in Boulder, Colorado, though I’m recording this from my place in Wyoming. I believe strongly in stepping out of your routine to think and brainstorm, and being up here in Wyoming gives me plenty of opportunity for that. This is the year-to-date video for the end of the second quarter.

First, I’d like to extend a warm welcome to all our new clients who’ve joined us in the last two or three months. I recently integrated another professional’s clients into my business and have enjoyed meeting many of you. You’re the kind of clients I love working with, and I’m thrilled to have you on board. Generosity Wealth Management is growing, and I’m excited about the future. I’ve been in this industry for 34 years, with Generosity Wealth Management established for 18 of those, and we’re building a legacy that will outlast me and others. We’re always looking for new clients, so if you’ve had a positive experience with us, please consider referring others who might benefit from our services, especially business owners looking to sell their business in the next three to five years. That’s my specialty—helping maximize value and manage the impact on personal wealth.

You can learn more about our work at generosity-group.com, the company I founded to align wealth with purpose and possibility. We do this through three key areas: Generosity Wealth Management, offering comprehensive financial services; Generosity Estate Planning, ensuring dignity and control over your assets and medical decisions during your lifetime and beyond; and Generosity Business Exit Planning, tailored for business owners preparing for a sale. Please visit the website to explore these services further. Additionally, I’m part of Ed Slott’s Elite Advisors Group because, outside of your home, your retirement account is often your biggest asset, and taxes are typically your largest expense. Being an expert in both is critical to serving you effectively.

Now, let’s reflect on the last quarter and year-to-date lessons. If you’re looking for a highly technical market analysis, this isn’t the place—you can find that on CNBC, Fox Business News, or other financial websites. My focus here is on the broader lessons. The first is humility. No one can predict the future with certainty. Three months ago, many were confident in their forecasts, yet April was a tough month, followed by a recovery in June that few anticipated. Over my 34 years and 15,000 trading days since 1991, I’ve learned the market always surprises. History may not repeat, but it rhymes, and humility is essential when approaching an inherently uncertain future.

Another key lesson is objectivity. Personal biases—whether political or otherwise—can cloud your judgment. If you lean strongly one way politically, you might gravitate toward news or people that reinforce your views, leading to confirmation bias. I proactively avoid this by seeking diverse perspectives, as I shared in last month’s newsletter with resources like allsides.com and groundnews.com. These platforms present the same story from left, right, and center viewpoints, helping me form my own conclusions.

Discipline and emotional control are also critical. Every year brings trepidation—whether it’s a politician you dislike, a global conflict, market fads, or significant declines. Volatility is normal; most years see at least a 10% drop in unmanaged stock market indexes. My videos consistently highlight that three out of four years are positive, but declines are part of the journey. Emotional discipline ensures a more enjoyable financial path. Money is meant to help you relax and achieve your goals, so your investments must align with your time horizon. Funds needed in the next month or two shouldn’t be in the market, while those for five, ten, or twenty years can weather volatility. Knowing your personal goals and maintaining discipline is key.

We could dive into tactical details about the past or upcoming quarters, but without the foundation of discipline, emotional control, and a clear time horizon, those details are secondary. Focus on the right questions to maximize your chances of achieving your goals.

That’s it for this quarter. I’ll be back with another video next month. If you have questions or concerns, reach out to me at 303-747-6455 or via email, which is displayed on the screen. I hope you’re having a wonderful summer. Bye-bye.