“Someone’s sitting in the shade today because someone planted a tree a long time ago.” – Warren Buffett

In our latest video, Mike Brady of Generosity Wealth Management discusses the importance of focusing on actionable, forward-thinking strategies in investing rather than getting caught up in the minute-by-minute analysis often seen in the media. With a look back at the previous quarter’s successes and insights into future market potential, Mike emphasizes a practical approach to investment that’s designed to navigate the inherent uncertainties of the financial markets.

Transcript

Hi there! Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered here in Boulder, Colorado. I’m here with my quarter end video and newsletter.

I want to start off with a question that someone gave me this past quarter. They said, “Mike, your videos are not often very technical. Why is that? Is there a thought behind it?” I want to assure you there absolutely is a thought behind it. There are lots of value-based and technical analyses out there every single minute of every day whether you want to read it or you want to watch it on CNBC or Fox Business News. You can watch for an hour or an entire morning and get lots of technical analysis on the cable news. You’re going to be very exact about something that might not really matter. It’s very interesting, but I’m more interested in the aspects in a very short amount of time, which is a lot of our thinking that will make us successful. I will tell you that one of the problems that I have – you’ve heard me say this before that I don’t watch TV news is because it’s 24/7. When we had a half-hour news, maybe in the evening, you have to be concise. What are the most important things? That means you get rid of a lot of superfluous information and talk and opinion. That’s just not the case when you have to be very clear and concise. That’s the approach that I take with the videos as well. What is the most important in a few minutes that I can impart that will be actionable, and that will make a difference? Being completely exact about something that doesn’t really matter isn’t interesting to me. Go ahead and read that in the Wall Street Journal or watch that on some of the specific business ones and you’ll get that. Every once in a while I sprinkle some into my videos but not very often.

Let’s talk about what I think about the last quarter. It was great. By the time you’re watching this video and I’m recording this on Sunday, March 31. By the time you get this video, if you’re my client, you’ve already gotten your statement. You’ll have seen that the unmanaged stock market indexes are positive. The bond indexes, depending on the duration, are either up a little bit or down a little bit – the unmanaged bond indexes. So, pretty flat or, like I said, plus or minus a few on the unmanaged bond indexes.

The real big news is how strong the equity markets have performed. It is very common just about now in the cycle where people say well, it’s obvious that it’s at a high. What do we do when the market is at a high like it is right now? My answer is well, it’s a high compared to what? I mean, it’s a high compared to a year ago, and it’s a high compared to five and ten years ago, but I hope that it’s a low compared to what it’s going to be. To be honest with you, the Dow Jones Industrial Average, which is an unmanaged stock market index, used to be 5,000. Then it was 10,000, then it was 20,000 and then it was 30,000. Now it is almost 40,000, and by the time you watch this video, maybe it will have gone over 40,000. I don’t know – it hasn’t as of Sunday, March 31.

All along the way, when it was at 10,000, I heard people say, “Oh yeah, it’s obviously at a market top. What should we do? Oh, it’s obviously at a top, it’s 20,000.” And then at 30,000. We’ll continue to say this all the way up as it continues to go forward, which I believe that it will. If I didn’t believe that it would, why would I have investments? Why would I have any exposure to any kind of a stock or equity-based investment if I didn’t think that the future was going to be higher than it is today? I don’t know when it’s going to be higher, but why else would I have investments if I didn’t think that the future was brighter than putting it into some kind of a cash or stick it in my mattress or my pillow.

I think that’s a really key concept that we have to remember, and don’t listen to others who might say, “Oh no, now it’s going to go down as we hit the election” or “This is a year that’s going to see all kind of turbulence” and this, that and the other. The future is inherently unknown and we have to keep that humility in mind at all times. That’s what I want to impart on the end of the first quarter. We have three quarters left. We have an election and we have a lot of stuff happening. Hopefully we’ll have some decline and decrease by the Fed on the interest rates.

What I want us to really remember is we have investments for a reason. That’s because the future, we believe, is going to be better than it is right now and we’re going to make profits along the way. If we don’t feel that way you’ve got to give me a call because there’s a mismatch. There is a mismatch in your thinking to what you might be doing, and it’s better to do that proactively now than later. That’s my message for today.

Michael Brady, Generosity Wealth Management, 303-747-6455. You have a wonderful week, a wonderful quarter and don’t listen to 24 hour news. It’s horrible. I hate it. Thank you. Bye-bye.

“Write it on your heart that every day is the best day in the year.” – Ralph Waldo Emerson

In 2023, the financial markets underwent a significant transformation, moving away from the volatile, stimulus-driven landscape of the post-pandemic era. This year was marked by remarkable economic resilience and recovery, characterized by easing inflation and a robust job market, diverging from the prior year’s instability.

Despite early concerns of an imminent recession, both the U.S. and global economies displayed strong growth. The U.S. economy, buoyed by consumer spending and a persistently low unemployment rate below 4%, coupled with a global economic uptick of 2.8% in the first half, showcased recovery strength. These gains were partly fueled by diminishing supply chain disruptions and geopolitical tensions from the pandemic.

Inflation, while starting the year at higher levels, showed a declining trend, with the U.S. CPI dropping from 6.4% to 3.1% by November. This downward trajectory is expected to continue, aiming for the Federal Reserve’s target of around 2% by mid-2024. However, global core inflation remains a concern, likely staying above 3% into 2024.

The stock market in 2023 witnessed a shift in leadership, expanding beyond the tech sector. The energy and industrial sectors outperformed, signaling a move towards a more diversified and balanced market. The bond market experienced modest gains, as reflected in the Bloomberg US Aggregate Bond Index, reminding investors of the inverse relationship between bond prices and interest rates.

Looking ahead to 2024, the economic growth is expected to moderate, necessitating a diversified investment approach and vigilant monitoring of inflationary trends. Central bank policies will be crucial in shaping the market, emphasizing the importance of staying informed and adapting strategies accordingly. With both positive and negative factors at play, it’s vital to maintain a forward-looking perspective and seek tailored guidance for individual financial situations.

Here’s what Generosity Wealth Management founder, Michael Brady, has to say:

Transcript

Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered here in Boulder, Colorado. It’s a lot more fun to make today’s video than it was this time last year because 2022 was a dumpster fire. Unmanaged stock markets and unmanaged bond indexes are both down over 10 percent, depending on which one you want to look at. Nothing was good, and it felt that way. You know what? That’s not the situation we’re seeing ourselves in for 2023.

Let’s go back just a few years as a little bit of a multiyear view of the world. So, 2020 was a positive year, with lots of money dumped into the economy because of the COVID shutdown. In 2021, we still had supply issues, but we dumped lots of money in and 2021 was a positive year for the unmanaged indexes. In 2022, we had supply issues and lots of money inflation, so 2022 was a bad year. Just horrible. In 2023, the first and second quarters were good. The third quarter was not good for the unmanaged indexes. This fourth quarter has been just a roaring great quarter. For 2023, we’re looking positive, depending on the indexes. It’s definitely double-digits. The unmanaged bond indexes are still single digits, and we’re clawing our way back from what was given up in 2022.

You have to remember that with unmanaged bond indexes, when interest rates go up, bonds go down. The bond indexes go down in general, and of course it’s the flip. When the interest rates go down from the Fed, the unmanaged bond indexes will hopefully go up and should go up. That’s why there’s that inverse relationship.

As we’re looking at 2024, we should be optimistic because it feels like the markets, most of your pundits, the media, and most of your major investors are expecting a 2024 decrease in interest rates after such a sharp increase in 2022. This is good for the unmanaged bond indexes and for the stock indexes, and hopefully that will also correlate to people being a lot happier as we have a positive 2024.

Let’s not forget that we have a pretty volatile situation going in with a sitting president who is running for reelection and a former president who, if he’s the candidate, may run again. Nonetheless, we’re going to have two candidates for the presidency in a very sharply divided country. As always, there’s lots going on in the world, whether that’s the Middle East or Ukraine. Hopefully, in 2024, we don’t have any issues with China that we’ve all been talking about.

If you’re looking for something to be pessimistic about, you know what? I’ve got something for you. If you’re looking for things to be optimistic about, hey, I’ve got that too. We’ve got the interest rates. We’ve got an economy that’s chugging along. We’ve got companies that have made themselves more profitable by increasing the profit margin. If you’re looking for stuff that’s going to be positive, there is lots to be positive about as well.

Three out of four years historically, as we go back 100 years, the unmanaged stock market indexes have been positive. We had a negative year in 2022, and 2023 has been positive. Hopefully, 2024 will continue, but I have to say that humility is a big part of everything that I’m about. Generosity, humility—and why do I say humility? For the first part of my life, I wasn’t as humble as I should have been. But with some experience, I realized that you never know everything. There’s lots going on that you miss. You do the best that you can, and the future is also inherently unknown, so what can we do to navigate inherently unknown waters going forward? That’s what we’re doing here today.

Mike Brady, Generosity Wealth Management, 303-747-6455. Let’s have a great 2024. Thank you for being my client in 2023.

Time well-spent results in more money to spend, more money to save, and more time to vacation. – Zig Ziglar

In our latest financial market update, unravel the financial landscape of 2023 and hear a balanced perspective amidst the market’s ups and downs. Despite recent losses, the market has experienced impressive growth over longer time frames, reminding investors of the significance of perspective and patience. Dive deep into the impacts of the Fed’s decisions on the bond and stock markets and explore the ripple effects on the real estate industry.

While we can’t control global events or federal decisions, we have complete autonomy over our financial strategies and emotional responses to market fluctuations. Explore the power of perspective and the journey to financial resilience, even in a world of uncertainties. Blend wealth management’s macro and micro-elements in a space where clarity and strategy turn market turbulence into opportunities for long-term growth.

Transcript

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered here in Boulder, Colorado.

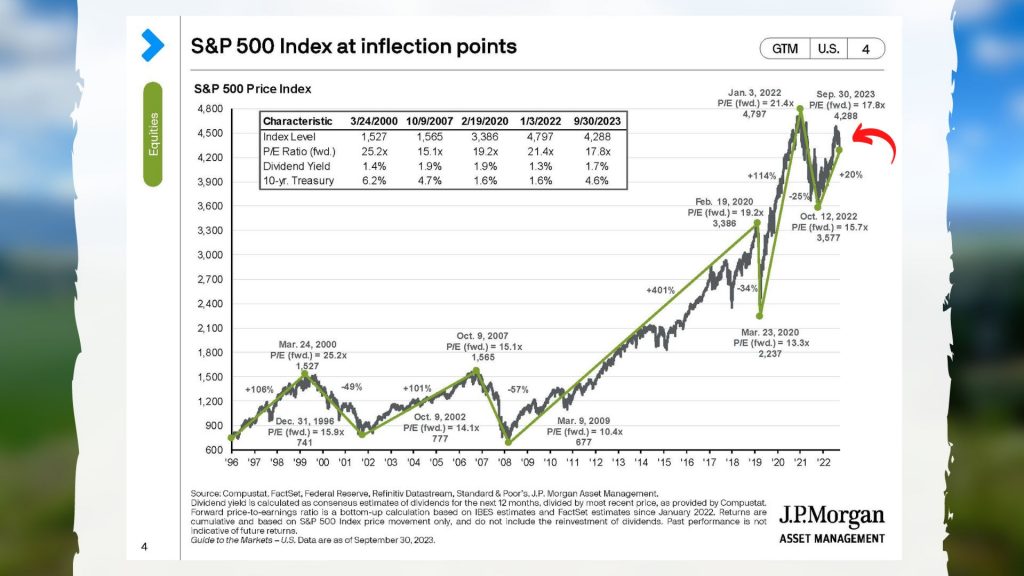

I’m recording this the first week of October and we now have three quarters of 2023 under our belt. Frankly, it was great until about two weeks ago, three weeks ago when we really started to give up much of the gain that we had made in July. July was a good month and then August was kind of a muted month, and September has not been good and so far this first week of October has not been good as well. It’s important for us to remember it’s our timeframe. Are we down from where we were in July? Yes. Are we up from where we were at the beginning of the year? The answer is yes. From a year ago, 12 months ago we’re actually dramatically up. Are we down from where we were at the beginning of 2022, which was pretty much the high, about January 3, 2022, for the unmanaged stock market index, the S&P 500. The answer is yes. But when we go back out that’s about a year, almost two years ago.When we go out three years, four years, five years, ten years are we dramatically up?

The answer is yes on the unmanaged stock market indexes whether it’s the Dow, whether it’s the S&P, et cetera. That’s why we kind of look at it. People are like oh my gosh, it’s down. The answer is yes, it depends on your timeframe, and it’s important for us to always keep the proper timeframe. Is it down for the week and for the month? Yes. Down for the quarter? Yes, maybe. But then we’re looking at years – a year, two years, five years and then even ten years. If you need the money in the short term it’s absolutely relevant, but as we get a longer and farther time horizon the less the gyrations on a daily, weekly and monthly basis have meaning to you. Unfortunately, we have a 24/7 news cycle so it is important for them to excite your emotions on a daily basis – daily, if not hourly.

Up on the screen I’ve put the S&P 500 which is an unmanaged stock market index and you’re going to see where I put an arrow next to the “you are here” and that’s where we are. The Dow Jones which is not reflected on this chart is another unmanaged stock market index and it has actually turned negative for the year. The S&P is positive for the year, Dow is slightly negative.

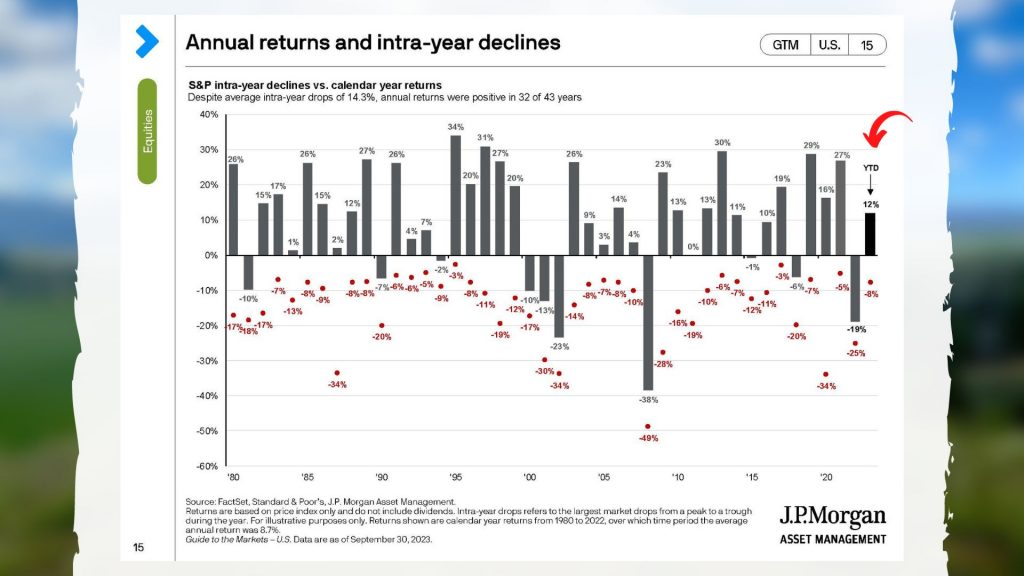

The second chart are annual returns and intra-year declines. You’re going to see that year-to-date number is positive for the S&P 500. The red numbers are during the year how much is given up from the top to the bottom within the year, so it’s called an intra-year decline. It is normal. You look at all those red numbers down there and you’ll see that it’s normal for there to be ups and downs within the year. When it happens, let’s not freak out. It’s normal. It’s always difficult as a human being to not extrapolate out. If everything is going up, you feel that it’s going to go up forever. If it goes down you feel like it’s going to go down forever. We look for patterns and we look at the clouds in the sky and we’re looking for little puppies and other things in the clouds when really there’s nothing like that. We see patterns but we can’t create patterns that might not be there.

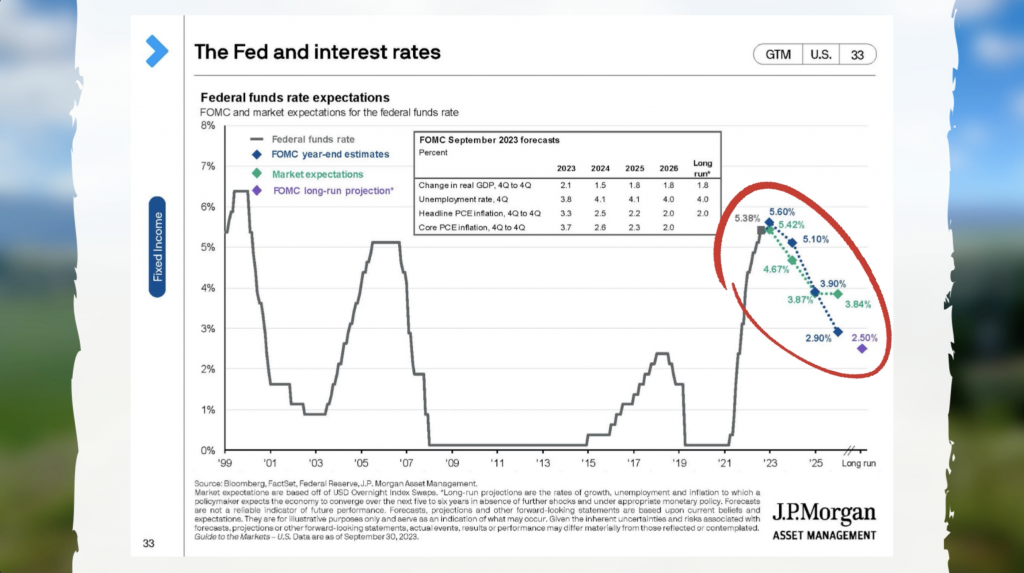

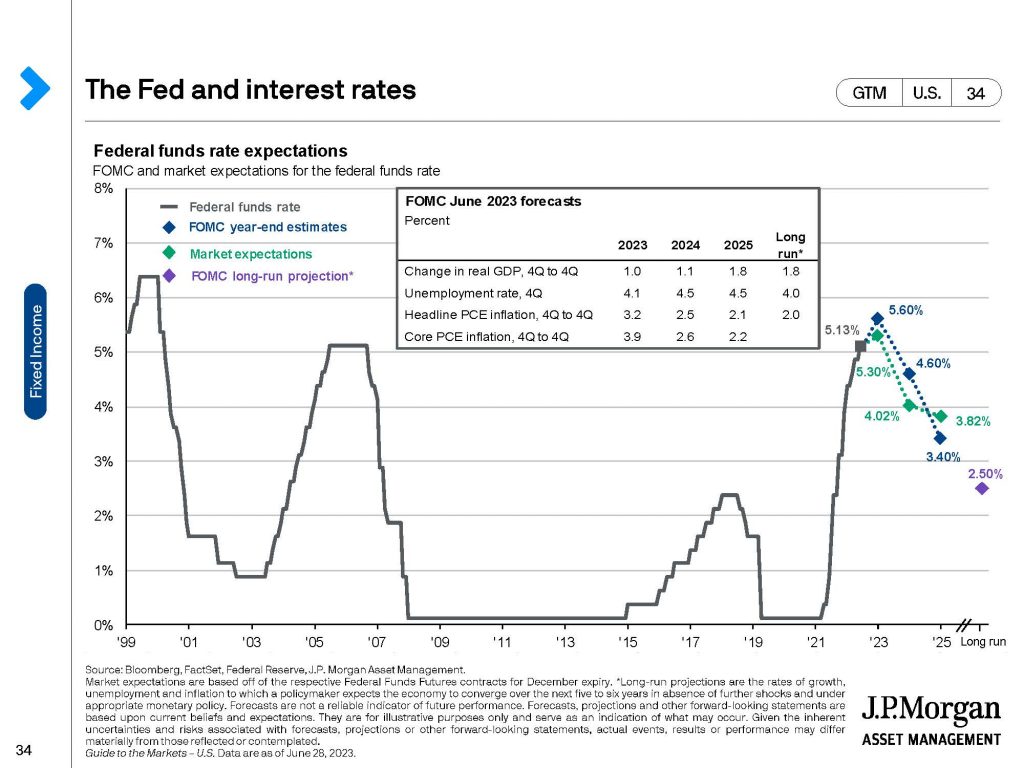

I think the big thing to watch out for is the Fed. I’m pretty irritated at the Fed. I’m by no means the only person. They waited too long to do something until they woke up some morning in the beginning of 2022 and said, “Oh, we should do something.” And then they overreacted all through 2022, in my humble opinion. Everyone’s got an opinion and people always say in hindsight it’s 20/20. Well, go back and look at all the videos. While it was happening, I was saying, and many others were saying, this is just way too much of an overreaction. You should not try to shove in one year, which is 2022, all the interest rate increases that you should have done over a longer time horizon. That has a huge impact on the economy and, of course, on the subsequent bond markets and stock markets as well. My concern is that they’re going to wait too long in order to reverse that trend. Right now, they’re in a holding pattern.

Up on the screen, you’re going to see what the expectations are. I’ve put a circle around it. There’s an expectation that it might go up just a little bit more but then it will decline. So, the most recent decline, in my opinion again, is due to the expectation they would start that reversal immediately, and now they’re in a holding pattern saying no, we’re not going to do something. We’re not going to do anything at this point. That’s frustrating, that’s irritating. Especially when we look at the unmanaged bond indexes. They have been impacted because the pricing of bonds is dependent upon the interest rates that are out there. Until the interest rates are reversed, bonds are going to stay suppressed and perhaps even go down, which is what’s happened most recently because people had an expectation of lower interest rates which really hasn’t happened.

This also has an impact, of course, for any of you who have a house that you’re trying to sell or a house you’re trying to buy. Any real estate is frustratingly very expensive. A mortgage at 3% is a lot cheaper than a mortgage at 7.5% or 8%. And so that has a real crippling effect on the number of transactions, the price of the properties, the inventory, things of that nature. This is not just for residential home properties, we’re talking commercial as well. Loans, home equity loans, commercial and business loans. That’s a real dampening impact on the economy which has me concerned.

They’ve said that if everything is a priority, nothing is a priority. If everything is important, nothing is important. It’s good to know what you should really be focused on. In my opinion, it is the impact of the Fed both on the bond portion of a portfolio but also the impact, the spillover into the stock portion, the equity portion of the portfolio as well. So, it’s very frustrating.

What can you and I do about the Fed interest rate? Nothing. That’s outside of our control, but that does not mean we’re completely powerless, so let’s talk about that.

I was talking with a good friend of mine the other day and we had this realization of two different views of the world. He has a tendency to look from a global point of view. He would love to sit here and talk for 15-30 minutes about the Ukraine and the Russian situation and whether we should provide more aid or less aid. Just really talking about these global issues which is fun and interesting over a cup of coffee. However, I’m less interested in that because whether he and I agree or disagree or we solve the problem, nobody cares what Mike Brady thinks. I’m not going to impact that, or if I do, it’s going to be very minimal by the people that I might elect into Congress which then will make Congress or the President of a political office who then will make the decision.

Instead, many of you may or may not know, but I went to Ukraine in August to help out. I’m the treasurer of the Board for an international adoption and hosting organization. There I helped out with 300 kids who are stuck in Kiev and in central and eastern Ukraine. They came over to western Ukraine and I was able to help them deal with their trauma. It was only a week but it made a huge impact as we had this camp, Camp Say Yes we call it. That was very impactful. Can I impact the big global? The answer is no, but what I can wrap my hands around, my mind around is that there are some kids who have some trauma that need some assistance and I can provide some of that support.

When I take that same philosophy to finances and to wealth management it’s “can I impact the Fed?” No, I can’t. What I can do is keep my emotions in check. I can make sure that long term my portfolio is the appropriate percentage of both the equity portion in the stock, the right balance in my portfolio. I can keep track of those other aspects that can derail me from my long-term financial plan. There are lots of decisions that I can make to shore up what I believe will increase my probability of meeting my financial goals and reaching those goals long term.

I think that having that long-term vision, I think that understanding what it is that I can control and impact, and make sure that I’m as solid as I can as I go through the future which is always inherently unknown. We have to remember that. There’s always government politics and government craziness, at least in my 54 years it’s always been a part of that. What I can do is to know those things that I can control and try to do the best in order to be prepared for all that.

Mike Brady, Generosity Wealth Management. 303-747-6455. We’ve got one more quarter in 2023. Let’s hope the Fed cooperates with us, but if they don’t let’s keep our eyes on the long-term goals.

“Money, like emotions, is something you must control to keep your life on the right track.” ― Natasha Munson

Knowing whether you have an investor or trader mindset is a really important aspect of ensuring that you are satisfied with your financial plan and goals. Discover the fundamental principles that underpin effective investment planning. In the latest GWM video, we explore the importance of setting clear financial goals, understanding risk tolerance, and crafting a well-defined investment strategy tailored to your unique circumstances. Financial growth and security can really only happen when you know yourself fully. Take a watch and let us know what you think!

Transcript

Hi, there. Mike Brady with Generosity Wealth Management, a comprehensive, financial services firm here in Boulder, Colorado.

Today I want to talk about investment management and planning. One of the first questions to start with is are you a trader or are you an investor.

Before I really talk about that and how that flows out into our planning, there’s this great book called A Conflict of Visions by Thomas Stowell, who is this famous economist. He’s now in his 90s, and what he said is when you have a disagreement with somebody whether it’s political, religious, it doesn’t really matter, you’ve got to think of it like a tree. You’ve got a tree. You look at my hands and the root of the tree is here and then branches come out. There are all these decisions – a decision matrix. If you’re disagreeing way up here at the top level, the top leaves you’ve got to go back down the tree, down the limbs to where you might have had a conflict division, where you might disagree. We agreed all the way up to here and now we disagree and that disagreement from a philosophical point of view then has repercussions all the way out here like that.

I think of the same process when it comes to investment management and planning. Are you a trader or are you an investor? Very key. An investor is someone who purchases something, purchases an investment, assumes the investment will be greater in the future and knows that there will be ups and downs along the way, but makes very few changes to that along the way.

A trader, on the other hand, is very actively managing saying wow, I want to buy this stock, that stock, this mutual fund. They want to time the market, they believe that now is the time that the market is going down so I want to move over to cash. Very actively managing it. That is a trader and a trader mindset. A lot of the uncomfortable, the displeasure, in the future is when you say that you’re an investor, you’ve set things up like an investor but then you have a trader mindset. That might be your tendency and your bias.

Once you decide whether you’re a trader or you’re an investor, then you have to decide do I take individual business risk or do I not. That means individual stocks. Do you buy a certain company and be very specific to it or do you buy that broad sector, do you buy the broad market? You could by in the automotive sector and be very heavy in that versus an individual automotive stock. Or do you buy the market as a whole, the S&P 500, the international unmanaged stock market index. It’s really a philosophy of in addition to market risk do you take individual business risk.

That is a very key ingredient and once you’ve decided that, then the question is how do you do that? Do you do that through the various ways like mutual funds? Do you do it through separately managed accounts? Do you do it through ETFs, all of which require a very detailed video to describe some of the pros and cons in each. All of them can be not necessarily good or bad. It’s just a preference. What’s better, a sports car or a truck? Well, neither of them. It depends on what the purpose is. It depends on the individual as well. It’s the same way with your particular investments.

One of the most important decisions as well is are you a believer in mathematics, the CAPM, the Capital Asset Pricing Model, meaning that “hey, I can figure out where the value of this and market is or this particular stock and that’s what it’s either overvalued or undervalued”, or are you more of a behavioral finance person believing that the market is filled with human beings who are emotional and sometimes make irrational decisions. That’s a very key decision to ask yourself and to think about. And of course to talk with your financial advisor to say “hey, what do you think? What’s your philosophy on all of these various aspects?” They are important to craft a portfolio that you’re going to be happy with.

The most important thing is that not that every single day, month, quarter or year is happy for you, but that you’re able to survive it. I think of it like a marriage. When you get married you know that there’s going to be some disagreements and not every single day is going to be sunshine and roses. But, of course, there’s more days that are good than are bad and that you know hey, I can weather this and this is for the long-term good and I’m a better person because I’m mashed up with this other individual in this thing we call marriage. It’s no different with investments. You’ve got to stick with what the plan is that you’ve got and that’s where good investment management comes into play.

Warren Buffett says that bear markets transfers money from the impatient to the patient. Whether you’re a trader or an investor, whether or not you believe in individual business risk or individual market risk or how these things come together. The most important thing is to be patient because even if you’re a trader buying and selling and doing all this other stuff there is a streak that’s going to happen at some point that is not in your favor and you’ve got to weather that as well.

I believe in taking individual market risk but not business risk. I believe in a more passive approach being an investor and not a trader. I believe in many other things that help, but I guide that with my clients.

If you want to talk about investment management and planning and the thought process behind it I’m always happy to talk about my philosophy and how it might work for you. If you’re my existing client or if you’re not how it might fit with your individual situation. Mike Brady, Generosity Wealth Management, 303-747-6455. Thanks.

“The goal isn’t more money. The goal is living life on your terms.” – Chris Brogan

Amidst dynamic market shifts, we remain focused on long-term investment goals. Over the past years, we tackled volatility, geopolitical tensions, and economic disruptions by adhering to a broad-minded and long-term approach. By embracing the power of long-term investing and recognizing our biases, we’ve weathered storms and continued to make sound choices that reflect life goals. While we cannot predict the future with certainty, I am confident that our diligent research, robust risk management practices, and unwavering focus on your long-term goals will continue to guide us through both favorable and challenging market conditions.

As we move into the second half of 2023, I invite your engagement, if you have any topics you’d like me to address or concepts you’d like to understand better please let me know! Together, let’s navigate the journey ahead and seize opportunities to be generous with yourself, your loved ones, and your community!

Transcript

Hi there. Mike Brady, Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered here in Boulder, Colorado. It’s now the middle of the summer, at the end of June, or kind of the beginning. I just wanted to do a recap of not only this year but also maybe the last two to three years to bring us up to where we are now so we can put it into a larger perspective.

So, 2019 was a good year for the unmanaged stock market index. As 2020 hit, we had a huge decline once the COVID shutdowns hit. We dumped a lot of money in as a government, as a world, and gosh darn it, 2020 was a great year. Go figure. In 2021 we threw more money in, trillions of dollars, and that started to have an inflationary impact. We had a good year in 2019, a good year in 2020 as well as a good year in 2021.

In 2022 we started off the year – that was last year, and the Fed said hey, we’ve got these inflation problems. We’re going to start raising interest rates very quickly which is what they did. There’s a huge shock to the system, but I would also argue that we threw a lot of money into the system in 2020 to paper over some of the issues. You can’t just slow down a huge economy, a world economy, and expect positive returns. In 2021 we dumped a lot of money in when we created demand, but the supply chain issues were not resolved. So, we had restricted supply. That led to some of the inflation, which then was sharply addressed in 2022. Then in 2023 we’re still addressing that, but not in the same way that we did in 2022. The first nine months, three-quarters of last year in 2022, were sharply negative. It was not fun at all. You know this.

If you look back at my quarterly saying hey listen, these things happen every once in a while, and this too will pass. At a certain point, this is an overreaction, and I believe that the first three quarters of 2022 was giving up what we shouldn’t have gotten in 2020 and 2021 which we papered over. We put a bandaid on with a bunch of money flowing in which had its own repercussions. Since the fourth quarter of 2022, positive for the unmanaged stock market indexes. The first quarter of 2023, this last quarter of 2023 as well, the second quarter, was a positive one. That’s nice. We’ve got three quarters in a row of positive returns.

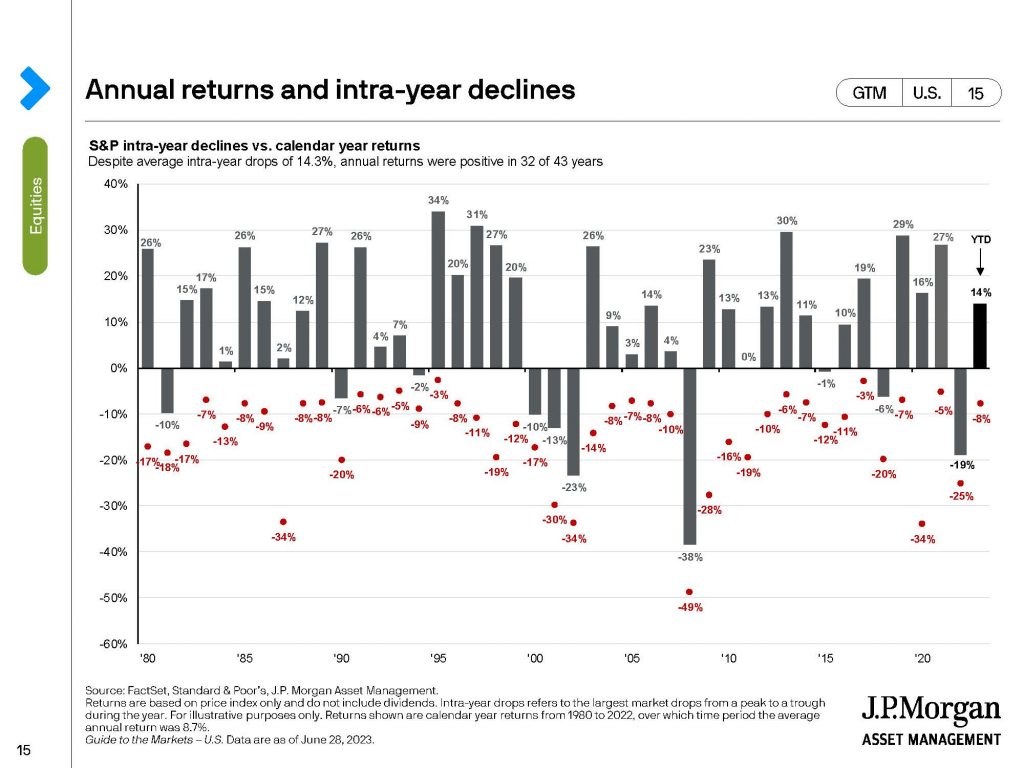

Up on the screen you’re going to see a longer period. Depending on the unmanaged stock market indexes and what someone’s portfolio looks like, it’s one-third to one-half of what was given up in last year 2022.

When we look at the unmanaged bond indexes they have not come back quite as quickly which is very frustrating. It’s unique that bonds and stocks go down at the same time in the same year and 2022 was that perfect storm. They haven’t come back quite as nicely because interest rates haven’t gone down quite as nicely as we would like.

When you look up on that screen what you’re going to see is interest rates are projected to decrease over the coming months. Yes, there might be another increase or two, but pretty much everyone and some other comments from the Fed have led us to believe that the opposite of what led to such a bad outcome in 2022 will be a good income in 2023 and 2024 as interest rates then go down.

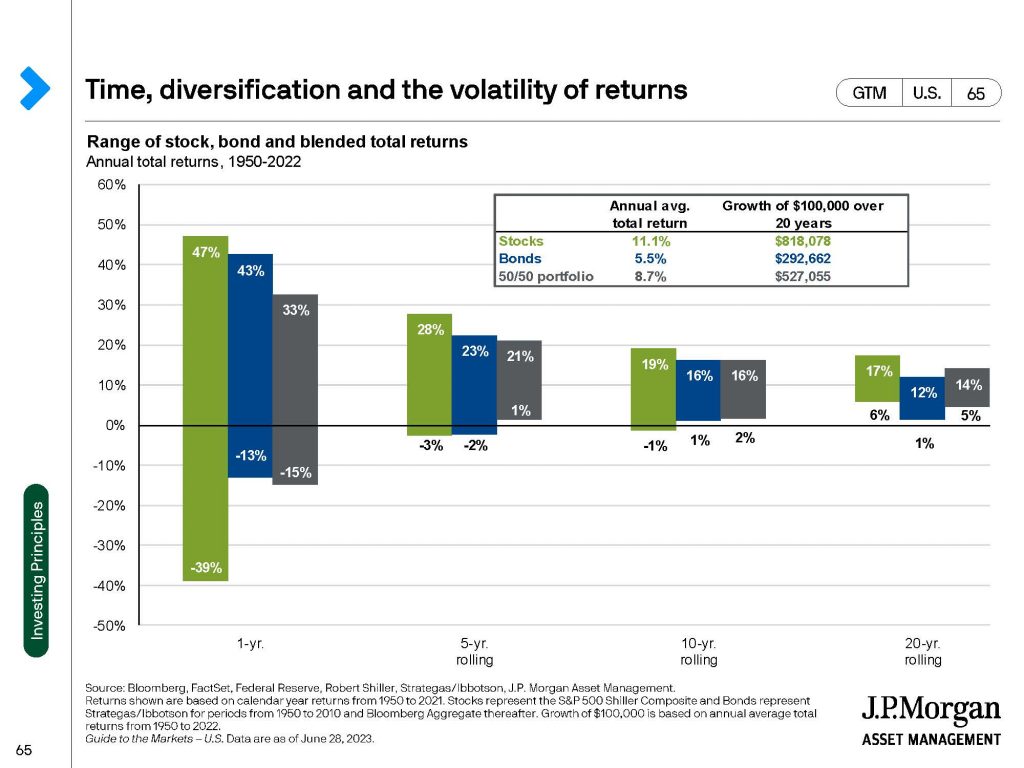

When we look up at the screen, you’re going to see one, five, ten, and twenty years mixed mash of stocks by themselves is that bar on the left-hand side, bonds by themselves, and then the third bar in each one of those categories is a mix of stocks and bonds, unmanaged bond indexes and stock indexes. What you’ll see is over five years, there’s actually never been a five-year time horizon where a mix and match of stocks and bonds hasn’t at least broken even or made just a little bit of money. So, one year absolutely. Two years, definitely. Once we go out from a three, a five, a ten or twenty year time horizon historically what has happened as the negatives have been offset by the positive with the positive winning out.

When I showed you that first screen – I’m going to put it up here again, three out of four years are positive, one out of four are negative. That’s just the way it happens. Sometimes it’s two years in a row that are negative. Sometimes it’s not three years positive, it’s six years positive. Great. Wonderful. When we start adding them all together, that’s when we get into historically up three out of four years.

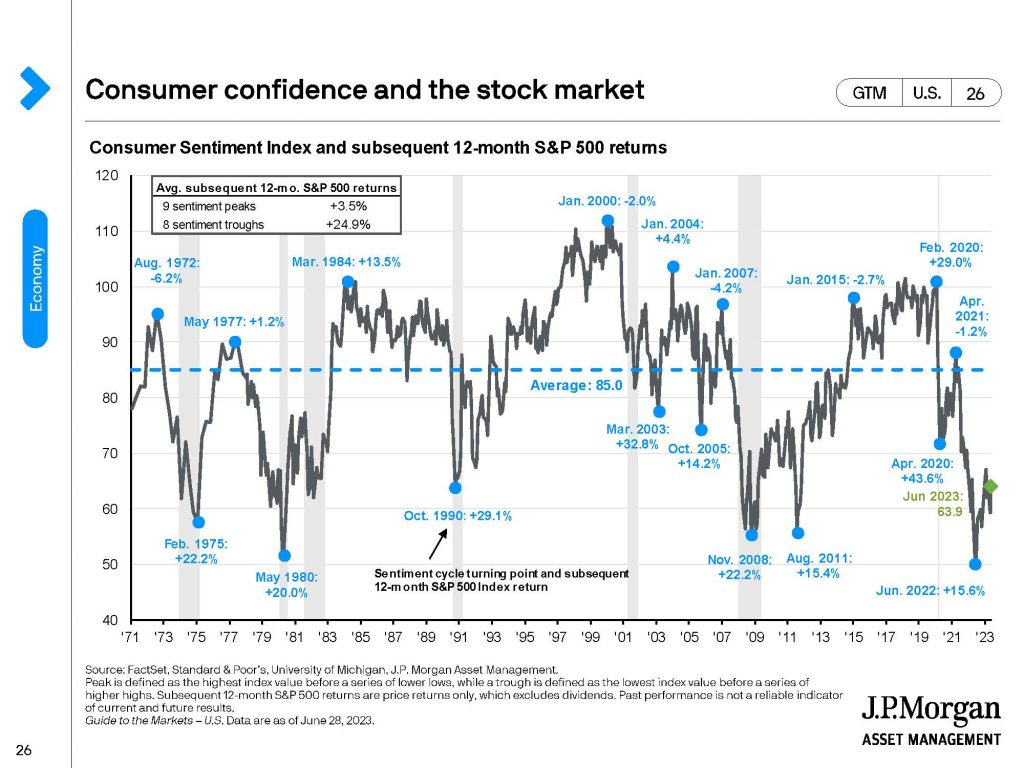

Here up on the screen, we’ve got some consumer confidence starting to rebound. I put a circle around it. The thing that we as investors have to remember is when everyone is feeling great, that’s when you maybe need to worry. When people’s enthusiasm is at its lowest, it’s counterintuitive but that’s when we want to buy. That’s when it might be the best opportunity for us to have that extra investment or to hold tight because maybe the recovery is right around the corner.

Think back over the last year-and-a-half or so, nine months ago. Were you like “god, I wish I had more money I could throw in.” Maybe, maybe not. You’ve got to be in control of your own emotions and understand that when it feels the most uncomfortable is often the time when the recover is right around the corner. That’s historically then the case. Consumer confidence is what we call a lagging indicator. Not a leading one, but a lagging one, meaning that once things are looking great, then everyone feels good. That’s too late. Once everyone feels bad, it’s already gone down so that’s too late as well. The emotions do not lead us to the right outcome or the right path that we want. The first advice that I would give is to be aware of that and to think about it for yourself and many times be contrarian to what your emotions are telling you and give me a call and we can talk it through.

One thing I would like to share, though, as we’re in the middle of the year is I have done for some clients some research on some of the big banks – the savings and checking account rates, and they’re still pretty pathetic, I mean almost zero. If you’ve got a lot of money in a bank it behooves you to do some research. There are CDs, there are money markets, there are treasuries. There are a lot of different strategies and you’ve got to pick the one that’s right for you. You’ve got to do your research, talk with me. I’m just telling you that there’s a lot of different things that are out there that you should explore. A little bit of work can dramatically increase just the cash that is risk-free or practically risk-free.

Normally going from one cash to another cash equivalent, it’s not that big of a deal, a tenth of a percent, maybe a fifth of a percent. Now we’re talking about big variances of a few percent, and that can make a big impact for cash that maybe you want to keep safe, you want to keep on the sidelines. Maybe you’re going to need it in a year or six months or for whatever purposes you might need. You may as well maximize it and especially in the short term. These rates are high right now, but if the interest rates start to go down they will go down as well.

Start to think about your cash and are you maximizing the interest rates on your cash? Of course, you should be maximizing your total return from a long-term point of view as well. That’s what you hear me say every time I put out a video saying we’ve got to have some long-term vision of multiple years, where’s the path we’re going towards, and how are we going to get there.

That’s it. Things are looking good for 2023. The fourth quarter of 2022 was good, and the first and second quarter of 2023 was good. We still have a ways to go to completely wipe away what happened in 2022 and get back to where we were in 2021. Given some time, I feel confident that we’ll be there before we know it.

Mike Brady, Generosity Wealth Management, 303-747-6455. You have a great day, a great summer. Bye-bye.