“The individual investor should act consistently as an investor and not as a speculator.”

― Ben Graham

There are so many things to feel optimistic and positive about, and conversely there are so many things to be pessimistic about. Which you focus on is your choice. We are inundated with data and noise about what’s important and while we could run ourselves in circles trying to address each thing, it’s more important to identify the two or three things that will make the biggest impact in our lives and focus on those.

Each Summer I spend the season at my second home in Dubois, Wyoming. With the new location comes a fresh perspective. Finding practices that can help you cut through the noise and focus on identifying your goals and strategies is imperative. While the market is good right now, it’s always uncertain, keeping your sights set on your big picture will help you weather any storm.

In our end of quarter 2 updates we discuss the key points in our current market.

Transcript

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered right here in Boulder, Colorado. Although right now I’m actually at my cabin where I’m privileged to spend the summer just east of Yellowstone, east of the Grand Tetons right next to Shoshone National Forest which is right there. In today’s Zoom world you would think this might be a picture, a backdrop but it’s actually reality. This right here – see that little orange thing – that’s the water well that I had dug about a week ago. See that woodpile. That’s a pretty good looking woodpile. And those mountains back there. That’s the Absaroka Mountains just right outside of the Wind River region in northwest Wyoming. There’s so many things to be optimistic about, so many things to be pessimistic about if you choose. Lots of chaos, lots of data, lots of noise, and I think that it’s important whether you’re running a business like I am, whether or not you’re worried about it for your own personal life for reaching your financial goals that you decide what to focus on. You could sit here and worry about a hundred of them and do a pretty bad job on a hundred, or you could worry about the one or two or three things that are going to have the most impact on what it is that you want. I think it’s important to do that and I do that every summer. What is it that’s the most important thing for the next 12 months and that’s where I am right this second.

So, this past quarter – another good quarter. Sometimes when I do these videos at the end of a quarter it’s sort of like well, let’s not try to overanalyze this thing. Things are going great and let’s take it when we can. So far this year in 2021 it has been positive, very low on the declines meaning that there’s been basically about three or four steps forward and really only one small little step backward. That’s a really good thing. There’s been very little volatility. With the unmanaged stock market indexes like the Dow and the S&P hitting new highs then when they’d go down by 100 points or 200 points, we used to all freak out. Well now because the Dow is well over 30,000, it’s statistically not as meaningful as it used to be.

So far this year most of the unmanaged stock market indexes are right around almost double digits or into double digits positive which is, once again, just wonderful. Who complains about that.

Bonds give or take. This is broad because there’s so many different types of bonds but in general the bond markets are breakeven to negative. If you’ve got a balanced portfolio with stocks and bonds and some cash and stuff like that, of course you’re not going to be double digits most of the time. If it’s just a broad picture here because the bonds have a tendency to bring that return down when they’re down and they dampen the effects of negative stocks in other years. It’s just kind of give and take. That’s why you have a diversified portfolio for those people where it makes sense to have a diversified portfolio which is pretty much everybody.

Up on the screen I want to put something. There is the weight. On the righthand side there, the top righthand corner I’m going to zoom in on that just a little bit. You’re going to see the weight of the top ten stocks is almost 30 percent. So, when we look at the S&P 500 which is an unmanaged stock market index, the top ten are 30 percent. So if they all went down to zero, the market would go down 30 percent. They have a huge impact on the S&P 500 and that has increased over the last three or four years. I mean we know this. Some of the big technology firms have had a huge impact and so they are having even more of an impact today than they did just two-three years ago.

Now, the same thing with that bottom righthand corner and I’m going to zoom in on that. That’s the top earnings so, of course, their earnings have just been killing it over the last 12 months. I mean COVID was very bad for some small companies in particular and very good for some of the big companies. And we’re seeing it right there. In that chart we’re seeing that in the returns as well of the unmanaged stock market indexes.

This next chart I’m going to put up on the screen is – look at that, way over on the righthand side. I’m going to circle it in red. I said at the beginning of the video that it’s important to keep your eye on what are the major things, the major decisions that you need to make. And one of them – the very best advice that you should have had for yourself or, if you listen to me, that I gave you was hey, listen. These things happen. Stay invested in the market. Stay invested for the long term. You don’t let short-term decisions, data, emotions determine what you’re going to do for the long term.

That right there at the very bottom to where it is right now, that’s what we have to keep in mind. It’s the big picture. Don’t let yourself be persuaded by that pundit on TV or your brother-in-law or whoever it might be who’s whispering in your ear to say, “Oh my gosh. It’s different this time.”

I’m going to show in this next graph that three out of four years, historically at least, have been positive. And that’s what we have to keep in mind is the duration that we have for our investments. If you need the money in the short term you shouldn’t have the money in the markets anyway. It’s not the market’s fault, it’s your improperly placing money in a long-term vehicle, money that you need short term.

I’m going to put up on the screen my third chart and the bottom righthand corner there, if we are so focused on the declines of the market we are not going to have the ups of it. If I am so concerned, as an example, of getting into a car accident that I never get into my car, my life is not as rich. My life is pretty darn local because I never leave my house or it takes me an hour to get from here to the grocery store. So, it is risk mitigation. It is not risk elimination. And so when we look at the bottom you can see that when there’s been a decline in the market, it’s followed by a huge upswing as well. Yes, you’re probably saying to yourself, “Wait a second, Mike. Just the math is if I lose 50 percent, in order to break even I have to make 100 percent.” That’s true from a math point of view. This still shows that when the market goes down, it has rebounded back to breakeven and then some and keeps going. And that’s what we have to keep in mind. The hard thing – and many times in our lives is to do nothing. We want to be industrious. At least we’re doing something. Sometimes the best thing that you can do is to do nothing or to stay with your long-term plan even if your questioning it on a short-term basis.

This next thing I’m going to put up on the screen – you’ve seen me show this before – is going back all the way to 1980. So, that’s 40 years. Forty years of data and three out of four years in general are positive. If you look at the far righthand side you’re going to see that the last ten years have had a lot of positive numbers, but they’ve also had the numbers underneath – the ones in red – are the intra-year declines. Those are within the year a step backward. So, if it went up ten percent and then it went down six percent for the year and maybe it ended positive, it went back up. But that negative four percent from the top, the biggest draw down is that intra-year decline.

You can see there for this year it’s been super low single digits. Very positive. Yes, it went high and then it went back down, it went back up, et cetera. Up and down, seesawing around, but that’s the nature of it. That’s the reason why we can’t look at things like a mosaic. You can’t get too close to your face. You’ve got to have some perspective and that is one of the major things that I emphasize all the time is you’ve got to keep the duration, the big picture in mind and what are the two or three things that are going to make you successful. And one of them, of course, is the big picture in mind. The second is do you have the right duration, the right timeframe for that particular pool of money.

So far this has been a great year. Let’s hope it continues. Now we’re hitting some of the summer months – July, August, September, October. A lot of times historically they’re not as attractive but sometimes they’re good. I mean there’s no absolutes. We don’t want to make a short-term decision here based on we don’t need the money in two or three or four months hopefully, so let’s not necessarily freak out.</p?

I’ll continue to have videos throughout this next quarter, but in the meantime I hope that you’re having a wonderful summer and I hope that you are, like me, that you get to change venues. Change something up in your life so that you see things in an even better way than you did before.

Mike Brady, Generosity Wealth Management, 303-747-6455. You have a wonderful day.

“I find television very educational. Every time someone turns it on, I go in the other room and read a book.” ― Groucho Marx

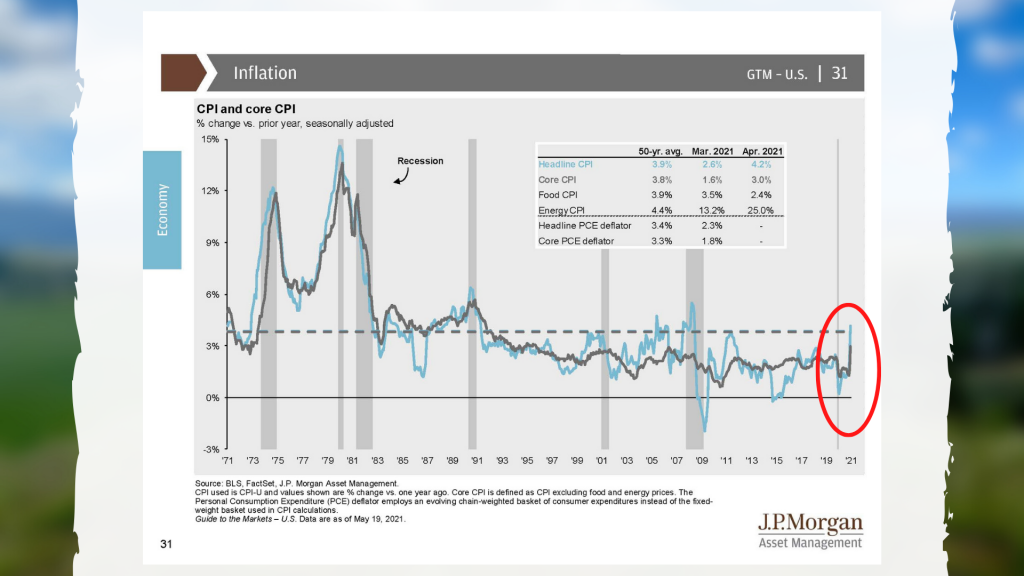

Last month’s inflation was 4.2% year-over-year percentage growth. That’s a large number and if you get your news from the TV news outlets, which we highly recommend you don’t, you are likely up in arms.

The news outlets are there to elicit emotion from you. If you’re going to have a detailed analysis of a complex system like the world economy in two minutes or even five minutes, watching TV news is not going to give you what you need to make an informed decision. Even the news programs on dedicated financial news channels is not where we get our analysis. We always turn to economists that we’ve learned to trust so that we can provide our clients with clear and concise updates.

So, is now the time to panic due to inflation? No, we don’t believe there’s ever a time to panic. But is there a time to be concerned about the impact to you, your life, the economy, your portfolio, things of that nature? Well, that’s not quite the right question to ask. The real question should be, is this temporary or is this systemic?

Watch to hear the answer and a full discussion on inflation.

Transcript

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered right here in Boulder, Colorado. Although I’m hoping that this will be the last video that I do in Boulder for the next four months or so, it’s the end of May. I’m going to head up next week to the cabin and, as you know if you’ve been watching my videos for a long time I can do everything I can do here in Boulder right there from my cabin. It’s 30 minutes outside of a 900-person town overlooking these beautiful mountains and pastures and all that. This next summer I’m very excited because they’re going to put in fiber optics right to my cabin. The whole valley there is getting fiber optics so thank you Rural Electrification Act, whenever that was.

Listen, I want to talk today about inflation. Last month’s inflation was 4.2% year over year percentage growth. That’s a large number and I have to tell you that if you get your news from the TV news outlets, which I highly recommend you not do, you, of course are probably all up in arms. Let me just address something that I said there. It is my belief – just my opinion and you can have a different one – that news outlets are not there to inform you. They are there to elicit emotion from you. If you’re going to have a detailed analysis of a complex system like the world economy in two minutes or even five minutes, watching TV news is not going to give that to you. Even the news programs, the dedicated financial news channels, that’s not where I get my analysis. I get my analysis from economists that I’ve learned to trust – Alex Tabarrok and Tyler Cowen and others and their detailed analysis. They’re usually writing every day great blogs. I post them in my newsletter periodically.

But the question is, is now the time to panic due to inflation? And the answer is no, I don’t believe there’s ever a time to panic. But two, is there a time to be concerned about the impact to you, your life, the economy, your portfolio, things of that nature. So, it’s the wrong question frankly. The real questions are is this temporary or is this systemic? What are all the factors in it? What are the conditions today that might be similar or dissimilar from the last time we had huge inflation which was in the 1970s, and people always go back to. There’s an old adage that every general is fighting the last war. Well, let’s make sure that we’re not fighting the last war against inflation because things were significantly different in the 70s. I mean think about the cars and TVs and microwaves that you had back in the late 70s, or your VHS which was probably a Betamax. I mean things are a little bit different 40 years later. The response and the understanding from an economic point of view about how the economy works has also evolved over that timeframe. It doesn’t mean that we shouldn’t be humble about the future because it’s about the future. Nobody knows exactly what the future holds.

So, let me get back to some of those questions that I’ve thrown out there. Let’s remember that 12 months ago pretty much everything came to a stop. So, the demand for our goods and services came to a screeching halt in general. Now, we’ve got an economy that is almost like a postwar growth economy. The demand for products and services is super high. Is the supply there to meet? No, not necessarily. I mean I was going to finish my deck on my cabin this summer and I can’t because wood has gotten super high. Right now they’re up at my cabin building a new water well and it’s costing me significantly more because of all the metal shortage for the piping that goes down to the aquifer. These are short-term demands that are not being necessarily met by supplies and by the supply chain.

Now, let’s step back for a second. By the way, before I complete that thought, these are short term. When there’s a huge demand there’s other people who come in that will meet that demand whether it is done in one month, one year. But it doesn’t mean that everything is doomed from here on out. At a certain point there is a give and take with supply and demand. There’s never a perfect amount of supply. There’s never a perfect amount of demand. Sometimes they get out of whack and for many core inflation items that’s the situation right now.

So, let’s move on. Is it nominal or is it relative or is it absolute inflation? That’s another thing we have to ask ourselves. If your wages are going up by 5% and inflation is going up 5%, it’s kind of a wash. Or the opposite. If your wages are going up which is what is happening now in order to get service workers in and many workers gets the employment down is wages are going up. If your wages are going up by 8% and inflation is going up by 4% to 5%, you don’t really care. You’re actually relatively wealthier even though inflation is going up as well. And one of the things that has happened over the last 20 to 30 years is we’ve become very addicted to inflation that’s very, very low and has been declining practically down to zero. That’s not necessarily the norm. So, when inflation from one year ago until now goes up, when we’ve become accustomed to a low rate and now there was oh wow, wait a second. Maybe it’s not always low like that. It does come back up. Let’s not extrapolate that out into the everything is horrible and it’s going to continue to extrapolate out in the future.

That’s one of the things that continually surprises me is from a stock market point of view, we know that every year there are going to be, in most years – not every year – but in most years there is a double digit decline within the year. So the market might go up a certain amount and then it usually goes back and forth. Four steps forward, three steps back, et cetera. And when that happens it’s like it’s never happened before. Some people get very excited about it. I’m not sure that helps getting excited about it. Inflation is the same thing. Inflation goes up and it goes down. It doesn’t always go in a straight line.

So, let’s talk about what that really means for the market. So, I’m going to put up one sheet – that far right hand – I’m circling it in red. That is what happened last month. That is over the last 50 years or so you can see that what I just circled is what happened. It went over 4%. It’s 4.2%. These things happen. The last time that happened was 2007 right before it declined. There’s some huge fluctuations there but one month does not make a trend. So, let’s remember that and we have a datapoint of one. Let’s not blow it out of proportion.

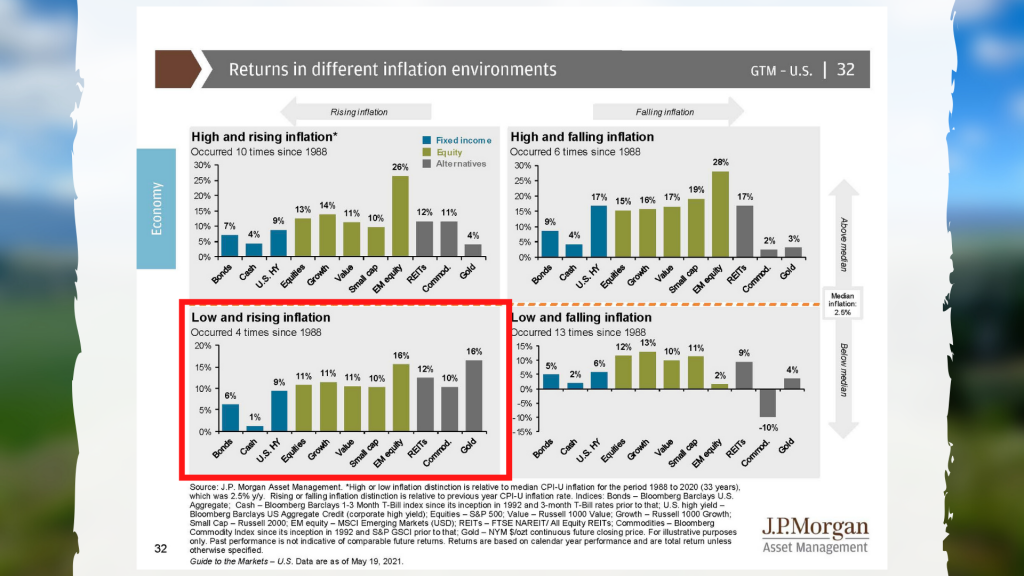

So, what happens? There’s this perception that when the inflation goes up, therefore the stock market is going to go down. That’s not true. Here I have just highlighted that bottom left quadrant and this is when we have low inflation and inflation is rising. What has happened? On average since 1988 – so that’s the last 30 years or so – the four times that has happened the market has increased over the next 12 months. That’s not a guarantee. This next time it could be different. We’re talking about the future here. But if there’s some knee jerk that inflation goes up and stock market goes down, that’s just not the case.

You’ve heard me before talk about duration and how important that is. As a matter of fact, the longer I am in this industry and the longer I work with clients and with money and financial planning, yada, yada, is the more important I believe the duration is which means hey listen, if you’re going to ask for a guarantee from me that the market won’t go down over the next month or two I couldn’t give you that. I could never give you a guarantee anyway. However, when we look out one year, two years, five years, ten years – which is what we should do – inflation has not been the deciding factor of whether or not you’re successful or not. If you need the money in a month or two or even six months you shouldn’t have that amount of money – you should have it in money market or in cash ready and not invest it however we’ve got our stuff for a longer term.

One of the things in the 1970s that’s different from today is it was stagflation, remember. A stagnant economy with inflation and high unemployment and all these things. We have low unemployment that’s decreasing. We have an economy that is growing, not stagnating. But yes, we have one month, one datapoint of inflation from an incredibly strange and bizarre event 12 months ago to lead us to an inflation year over year. So let’s not extrapolate this out. Let’s not panic and let’s not do anything.

One of the hardest things is to not do something at times. And many people say what, we’ve got to do something. You know what? “At least I’m trying. At least I’m doing something.” No, sometimes doing something in a knee jerk reaction is the worst thing that you can do. And the best advice that I can give as your financial advisor is not to do anything. Frankly, some of the best advice that I have ever given in my career was 12 months ago or 13 months ago or 14 months ago when it was like “hey, get off the ledge”. Don’t do anything because the real people who got hurt were those that panicked. And by the time that you, as the end consumer, hear the news from that news TV channel, it’s already been priced in. It’s already happened. And so if you feel you’re getting ahead of the game, you’re not. The best thing that we can do is keep our eye on the ball which is not panic. Let’s realize that inflation, not a big deal right now. What is really inflation? Is it relative or is it nominal? Is it short term? Is it systemic or is it temporary? These are the things that we need to ask ourselves. And right now, no. The warning flags are not out there. And know those who are economists, who are really managing money, the ones that I read are not panicked, which therefore means I’m not panicked and you shouldn’t either.

Mike Brady, Generosity Wealth Management, 303-747-6455. I hope to see you soon I suppose. I’m going to be up at the cabin, but I have so many Zoom meetings. Hopefully we’ll have those Zoom meetings as well. I think I’m going to grow a beard like I did last November and turn into true mountain man except when I’m working during the day. Have a great day, a great beginning of the summer. Bye-bye now.

You don’t have to control your thoughts. You just have to stop letting them control you

Powerful emotions drive irrational thinking in all areas of our lives. Twelve months ago we had an awful lot of irrational thinking. There was no way that anyone could have predicted that we would be where we are today, that the financial market would have not only recovered but experienced growth. It seemed like the recovery timeline should have taken longer, but it didn’t. But how did people fare? When you look back 12 months ago the people who made the best decisions were those that were in control of their emotions. Those who weren’t on the other hand, didn’t fare as well.

Let’s discuss why this is so and why looking long-term is always important, no matter what’s happening in the world.

Trascript

Hi there. Mike Brady with Generosity Wealth Management; a comprehensive full-service financial services firm headquartered here in Boulder Colorado.

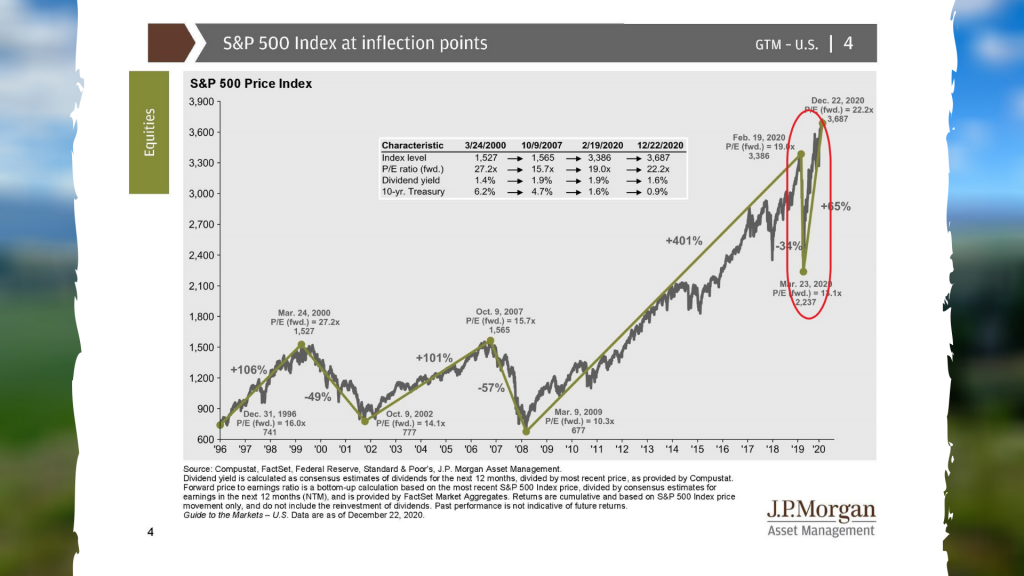

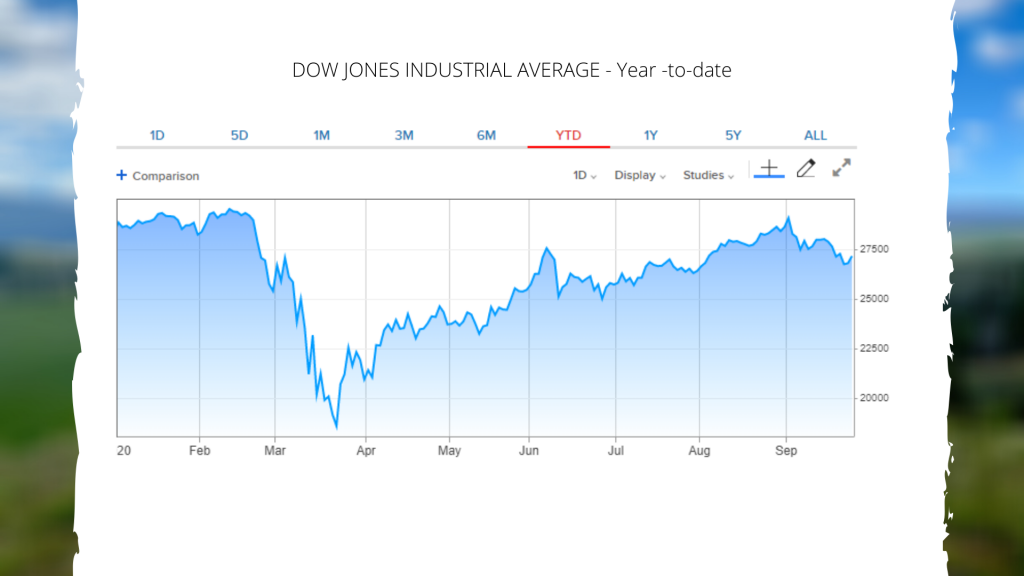

I’m recording this on Tuesday afternoon March 30th and the unmanaged stock market indexes have basically reached all-time highs within the last month or so, which is not the situation that we saw ourselves in 12 months ago. Let’s think back to where we were in March of 2020. The market had just absolutely cratered, some of the worst days ever as a percentage loss, we’re talking plus or minus ten percent in one day in the unmanaged stock market indexes. You remember how the Dow went all the way down to about 19,000? Right now it’s over 33,000. It had gone down from about 29 or 30 all the way down to 19. I’m going to put a chart up on the screen. At that point nobody was saying “oh yeah this is great, this is wonderful”. No, there was a lot of pessimism.

One of my core beliefs is that powerful emotions drive irrational thinking, powerful emotions drive irrational thinking in all areas of our lives. I mean I’m continually surprised when people my age or older people who have some gray in their hair still allow themselves to be whip sawed around by the external news or other people, that they allow what the person on TV or they read in the newspaper or the confirmation bias, the people that they talk to have a tendency to get them all worked up to elicit a powerful emotion and it’s my belief that that leads to a very irrational thinking.

Twelve months ago we had an awful lot of irrational thinking. There was no way that I thought at that point that we would be where we are today, that the recovery would be all the way back to where we are now and then some, but I felt strong that there was going to be a recovery, I just thought it was going to take a lot longer and there are reasons for that that are very complicated. When you look back 12 months ago the people who made the worst decisions are those that were not in control of their emotions or those that listened to that guy on TV or the absolute negativity, there’s a confirmation bias, a negativity pessimism bias that many people have, which is you’re actually looking for negative things to confirm that everything is just all messed up and that Armageddon is right around the corner, which, of course, it was not then and it never turned into that as well.

Duration and your time horizon are absolutely essential. I have said this pretty much every single video for the last 12 or 13 years because I feel so strongly about that. This past quarter has been positive for the unmanaged stock market indexes, which is wonderful, continuing a trend that started about 12 months ago. That recovery just continued on into 2021. In general, the unmanaged bond indexes are about break even maybe even a little bit negative, but that happens sometimes.

We always have to take our investments into long-term consideration. You might say to yourself “yeah but I’m 80 or I’m 85.” Well, okay, your life expectancy is shorter than somebody who is 30 or 40 or 50, but you also have to think and ask yourself “am I investing this for just my own use or is my time horizon for the people who might inherit it?” So, maybe the time horizon is longer than what you think. If you’re just about to retire your mid 60s, perhaps you’re married, there’s a 50 percent probability that one of you will still be living by age 90 so your time horizon is still many five and ten year time horizons.

One of the things that, I’m just going to quickly look here, is we also have to remember to properly assess our skills. There’s this concept called the Dunning Kruger Effect — remember Garrison Keillor he would always say all the children are above average, well we always have a tendency to think that we make the right decisions, that 12 months ago “oh yeah I just had a sense that the market was going to come back very quickly so I just had a sense that was going to happen”, which is very self-serving, a little bit of hindsight bias not quite remembering the way things played out. We have to avoid that and keep the long-term into consideration.

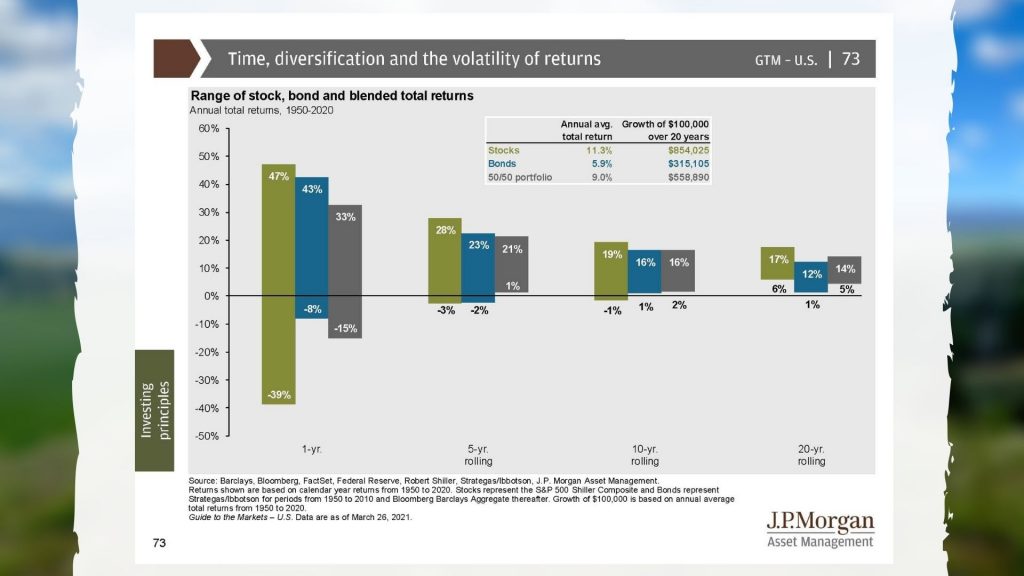

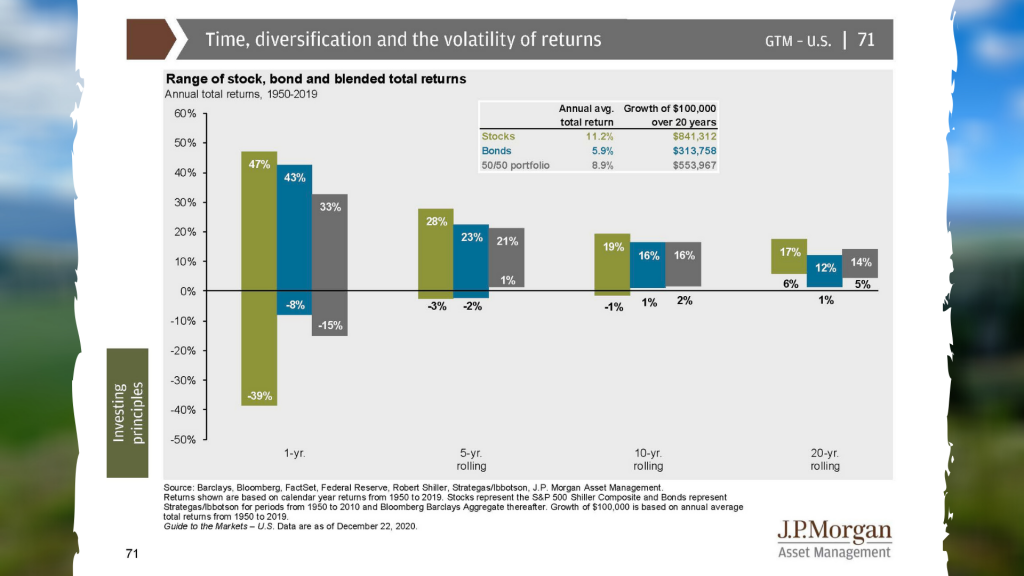

I’m going to put a chart up on the screen, you’re going to see the one, the five, the ten and the 20 years, which is those three bars for each of those time horizons going all the way back to 1950. So, that’s 71 years of an unmanaged stock market index, an unmanaged bond index and then a mixture of the two. When you look out at the ten and the 20 year, which is what I believe that you should, you can see that they’re all positive. There has never been actually even when we look at the five, a five, ten or 20 year time horizon where a mixture of bonds and stocks haven’t at least broke even or made a little bit of money. When we let our emotions control our decisions all of a sudden we’re stuck on that short-term time horizon, which is that far left which is the one year or maybe even shorter than that in quarterly, month or even week.

I can tell how long people have had an experience investing, many times I can tell by just the way they talk with me. If something happens and they’re totally casual about it then they probably have some experience or they understand that maybe they’re hiring someone like me who has the experience of over 30 years to be cool as cucumbers when something unforeseeable has happened of a big nature. You know what, we’ve kind of seen it all in different variations, sometimes more dramatic like we had last year, but these disruptions to the system have always happened and always will but what we can control is our reaction to them.

Mike Brady, Generosity Wealth Management. I will have all the statements out in a week or so for all my clients. I provide a statement a nice comprehensive statement at the end of every quarter so you can kind of see where things are going. I’m always available to talk. If you’re not my client would love to talk with you about what a long term ongoing relationship might look like. 303-747-6455. Have a wonderful day. Thanks. Bye-bye.

“Knowledge is of no value unless you put it into practice.” Anton Chekhov

30 years ago, financial advisors were the primary source for market information, such as how things are performing, statistics, etc. Access to the information was not readily available to the general public and it was a financial advisor’s job to communicate specifics with clients.

Now, thanks to the internet, anyone can access pretty much any information they want, any time they want. Thus, we generate much more value by showing you what to do with all this free flowing knowledge and analysis.

Watch as Generosity Wealth Management founder, Michael Brady, explores two questions he receives frequently: Why do you focus more on the non-technical; Is the market at a high?

Transcript

Hi there. Mike Brady with Generosity Wealth Management; a comprehensive full-service financial services firm headquartered right here in Boulder Colorado.

Today I wanted to address a couple of questions that I get periodically from people and one of them is around these videos. Somebody said to me “Hey Mike, I’ve been watching your videos for a really long time and I realize that you talk about some of the soft stuff, some of the non-technical. You don’t put charts up on the screen and do all kinds of lines and sit here and talk about this company’s PE ratio or somebody else’s sales earnings, et cetera.”

So, I’ve been doing this for about 30 years, and 30 years ago we had an advantage, we being the professionals, over your average person because we had more information than they did. We were able to pay for Bloomberg Terminals. I remember going to this Bloomberg Terminal, you would have to wait for it to be available because there was one for this entire office of 15 people or so. Or I would go to a paper copy of Morningstar, and I would sit there and photocopy it, and when you showed a client to it was like, oh my gosh there’s so much information here. That of course moved to monthly updates on CD ROMs and then the Internet came around, and then all of a sudden there was too much information. The information was not the deciding factor it was what do you do with that. It was almost too much. It was chaos. It was too much noise.

I’ve got to tell you, right now that when you watch TV, whether it’s one of the 24/7 news channels or the 24/7business channels, you’ve got all the internet blogs, et cetera, you can sit here and get all of the technical analysis that you desire. So, that’s not where I’m going to add value in my opinion; I’m going to instead add the value of what do you do with it.

So, if you’ve been watching my videos, you know that periodically I bring up poker because I’m a pretty big fan of the concept of poker. Believe it or not, I actually don’t like to play poker necessarily, but I appreciate the game and what it takes in order to be good. If you’re not a poker player, you think that it’s well all the cards are random, and it’s just kind of the luck of the draw. Nothing could be farther from the truth. If you’ve done any analysis into professional poker players, you will find that they ascribe success to the experience.

You’ve got to play thousands and tens of thousands of hands before you become really good. You’re getting instant feedback on your decisions. It is incredibly mathematical. It is money management. I mean, yes, it’s random how the cards are going to be played out, but you’ve got your hand, you’ve got cards that you might see, what are the odds against somebody else. It’s money management, meaning well I’m sort of in a good position so I’ll not put too much money on the table, or I’ll take some money off, et cetera. It is as much control of your own emotions, mathematics, and of course, experience to understand that.

In an uncertain game, and we can apply this lesson that I’ve just talked about to an uncertain world, which is what we’re talking about when we talk about the future and your financial plans.

So, those guys on TV they get to sit here and do all of the sexy stuff about this stock or that stock or this chart but they don’t really have to live with the consequences like you do. Have you ever noticed that they talk about their winners but they don’t talk about their particular losers? So, that’s something I think is very, very important.

Kind of a second question I wanted to address here today is around “is the market at a high?” I get asked that question or hear other people, you know, I might be in the locker room, and someone will say “well, the market is obviously at a high”. And I always think to myself compared to what? Compared to 20 years ago? Yes, it is at a high. Compared to ten years? Yes. Five years? Yes. That’s the wrong question. You can’t go back in time 5 and 10 and 20 years from now, all we can do is say today is day zero. Today is today.

So, the question is “is it at a high in comparison to where it will be or in our probability, in our estimation where it will be 5, 10, and 20 years from now?” So, that’s the question. Not it’s obviously at a high right now. Okay. Compared to where it was in the past. Sure. That’s actually a good thing, right? I mean don’t you want it to go higher? The question is what are we going to do today in comparison to where it might be in the future? I, of course, make my own analysis. I talk with clients about that I do believe it’s a very high probability in my judgment, in my estimation of the future, which is uncertain and unguaranteed that it will be higher in the future because why else would you have investments?

I sit here and emphasize duration all the time, meaning what is your time horizon? Because if you’re trying to get is it going to be higher in one month, six months? That’s flip of a coin. Sorry, it’s not going to be high probability of one way or the other.

So, I think that these soft things some of the best decisions that you’ve probably heard in the last year as we’re coming up on one year of this whole COVID, remember a year ago the market was just plunging 20, 30, 40 percent. The best advice was not mutual fund A or mutual fund B or this exact stock or that exact stock, it was stay invested. That was probably the best advice that you could’ve heard either from me or from somebody else. It’s those things that you know when you look back at many different data points, when you have lots of experience, when you work with someone who has lots of experience so that you can learn from them not only what to do but what not to do. And that’s really what I’m here to do.

So, anyway, Mike Brady. Generosity Wealth Management. 303-747-6455. Have a wonderful day. Have a wonderful week. Bye-bye now.

“What the new year brings to you will depend a great deal on what you bring to the new year.” – Vern McLellan

2020 was a rollercoaster of huge declines followed by a huge recovery, with ultimately happy investors at the end of the year. 9 months ago however, we didn’t know this would be the case. We were filled with uncertainty about the global health crisis and the ramifications it would have on financial health. For that reason we talked strategy such as keeping your emotions in check, remaining long term focused, having humility, knowing your bias, et cetera.

Listen as Generosity Wealth Management founder, Michael Brady, compares having a strategic versus tactical look at 2020 and what that means for the new year.

Transcript:

Hi there. Mike Brady with Generosity Wealth Management and I am here to talk about 2020 and looking at 2021. I want to talk more strategic versus tactical today. I want to give some good beliefs that I have that I think are very helpful and really the reason why I talk about strategic versus tactical.

Let’s just talk real briefly about 2020. Personally, I have had some highs and lows. I know after talking with many of you, you had some personal highs and lows, but the markets did as well with investments. If we look back just nine months ago it was significantly double digits, bear market, very sharp, very under water and very pessimistic with a lot of fear going forward. Very few pundits at that point would have said, “Oh yes, it’s going to end the year positive.” But you know what? That’s where the unmanaged stock market index is and the unmanaged bond indexes went as well. When you look at bonds, when you look at stocks they all pretty much from a market index ended the year positive, with some ups and downs. One of the things that we can learn from that, of course, is about ourselves. What is our emotional control? What is our humility and what is our risk and tolerance which I’ll talk about in just a little bit.

I talk an awful lot on these videos strategically. Let me tell you why I do that and how I define strategy versus tactical. Let’s pretend you want to lose some weight. How you view yourself is a strategic decision, but so many people spend all their time on what is exactly the perfect weight loss program. Is it Weight Watcher’s? Is it Jenny Craig? Is it something else? What’s the perfect exercise? I the meantime they have paralysis of analysis and they don’t stick with it. They don’t view, they don’t spend enough time on the strategic where they say I view myself as an athlete. I view myself as someone who doesn’t eat that chocolate cake. It’s not a big twist, not a big struggle to not eat that chocolate cake. It’s hey, that’s incompatible with who I am and the image I have of myself. So the strategic part is incredibly important.

A lot of what I do in these videos is talking about the strategic because I have come to the conclusion that a lot of people spend time on the tactical. And all those pundits on TV are talking about the tactical. This stock, that bond, short-term decision this, short-term decision that. Where 80 percent of reaching your financial goals is clearly defining them and having a plan for how you get there, and keeping certain things in mind as you go along. The tactical decision of your investment strategy is not of zero importance. It is only of lesser importance and not as important as the sum of the strategic decisions that you proactively make every single day. Going forward from day one but, of course, reiterating that to yourself as the years go by.

I want to knock off a couple of them right now. I’ve got a list here. Your attitude and your behavior is incredibly important. Number one, humility will lead to diversification. Humility means that we don’t know the future. You may notice that when I sit here and talk on these videos I’m like, “Well, I believe this and I have a high confidence that this will happen.” But the moment that I ever say, “This is absolutely what’s going to happen,” stop watching and fire me because nobody knows the future and what I have found is that the less data they have it feels like the more confident they are in that prediction going forward. Pundits on TV do that all the time. And what good humility leads to is diversification knowing that you don’t know exactly what the future is so you try to increase your probability of that desired outcome by being under the bell curve. A bell curve looks like this and we want to get right there. We’re not shooting for the stars. We’re certainly trying to not have a disaster. Therefore, we’re shooting for the middle so that we can increase that probability and that leads to diversification.

The second thing that I would like to say as a good strategy, good belief is know your biases. One of the biases I’d like to highlight today – because there’s actually quite a lot of biases – overconfidence, confirmation bias, et cetera. Today what I would like to talk about is all you see is all there is. That’s just not true. If you hear three pieces of facts and say well, it’s all fact based. There it is. That’s the conclusion. You know what? There might be another side of the story to that. Everything coin has two sides and so when we find the conclusion from the facts that are laid before us, we have to continue to look at the facts. We have to look at the other side. If every pundit is saying that it’s going to go up, try to read things that say why it’s going to go down. And, of course, vice versa. Frankly, I find this in discussions that I have with friends and family and things of that nature is listen, just because you’ve just given me some facts there, there might be some extenuating circumstances. What’s the content? What’s the intent of what you’ve just displayed from an argument point of view? That’s the reason why if you ever watch any TV shows or been in court there’s a prosecutor and a defender. The prosecutor lays out facts and then the defendant lays out facts as well. They, of course, have different views on perhaps the exact same facts. It is the same thing when we are looking at our financial plans and, of course, our investment strategy.

The third thing is emotional control. If that wasn’t tested this year I don’t know what was. I am very pleased that the people that I associate with the most had a great emotion between the greed and the fear that is natural as human beings. Those people who do the middle way as I like to say it. They don’t get too excited one way. They don’t get too depressed the other way. They understand that emotions sometimes lead us to do things that are not in our best interest. It is emotional control. And hopefully when you talk with me, when you meet with me, when you watch these videos you can understand that while I have enthusiasm, I’m an emotional guy. I like to hug people. I’m by no means a robot. I certainly don’t let myself get caught up in the moment and I don’t let myself be controlled by my emotions. Acknowledging that I have them, but not being controlled is the path that I believe.

The next thing I have is being default aggressive. That is a military term. When you don’t know what to do, do something. A good plan today is better than a great plan forever in the future which may be never. Not forever but never, and so default aggressive. That means something different for everybody. What I mean is if you don’t know what to do, doing nothing might not be the right thing. Moving to cash is probably not the right approach for most people. That’s doing nothing. That’s when you don’t know what to do. History has shown that over a long time horizon one of the best things to be is to be in the market and to be invested, fully invested at all times. And so it’s important keeping in mind that you’ve got the emotions as well. You’ve got to find the one that is right for you. Of course, you can’t be too aggressive, but you can’t be too passive. Everybody has their special place on that spectrum from conservative to aggressive, but you’ve got to do something and that’s just one of my beliefs.

The very last piece of advice I have is to think long term. You don’t let short-term decisions dictate long-term decisions and plans, et cetera. If you are 70 years old I hope that you’re going to live many five and ten year periods between now and when you leave this Earth. If you’re 80 years old, the same thing. If you’re retiring, if you’re in your 40s and 50s, historically the longer you wait – I’m going to put a chart up there a little bit later in this video. The longer that you are invested you have a higher probability of having that desired outcome. I’m going to put that up in a chart. You’ve got to have control of your emotions. You’ve got to think long term along the way. And, of course, the news I’ve got to just tell you – I don’t watch news and CNBC and all those things. It’s just my opinion because do you leave that hour program or whatever it is that you’re doing more informed or emotionally charged one way or the other? If you’re watching the evening news or during the day 24/7, do you leave charge because they’ve reached your emotions or have they reached your intellect? And I certainly will say it’s probably the former. Are they there to inform you or to get you emotional and to elicit some kind of a response. I find it not helpful whatsoever.

So, one thing that I want to talk about is every once in a while I hear someone say well, the market, the Dow Jones which is an unmanaged stock market index, it’s obviously at a high. My answer is obviously? I mean what does that mean? Yes, it is obviously at a high compared to where it was five years ago. That is a true statement. It is not necessarily obviously at a high from where it will be five years from now which is all I care about. If I wasn’t invested five years ago and I’m only now deciding whether to invest, it doesn’t matter where it was five years ago. It only matters what it will be in the future. And so if you believe long term that the market is going to be lower – and long term is multiple years then yes, you should not have investments that are at risk in any way from a volatility point of view. But if you’re long term the only thing that matters that’s obvious is that where it was in the past, in the future it is unknown. And I will be very confident in my own thinking – and history has shown this – it is good to have investments for the long term. I’m now reaching my thirtieth year of meeting with clients. I got my license in 1991 and now it’s 2021. When it was 5,000 on the Dow people said it’s obviously a high. And then it was 10,000. Well, when it hits 10,000 that’s a real emotional mark. It’s going to have a hard time going above that. And then it was 15,000 and then it was 20,000 and then it was 25,000. Then 30,000. Now it’s over 30,000 and so why would we say it’s obviously at a high.

So, just one or two more things and I know this is a long video but we have a lot to do and I think it’s important because of the incredible year that we’ve just had. Up on the screen is the S&P 500 which is an unmanaged stock market index. You’re going to see and I’ve just put a circle around it, that’s what happened last year. A huge decline, huge recovery, everybody’s happy at the end of the year. Nobody was happy nine months ago. It’s just that simple. It is the reason why we keep in mind many of those strategic beliefs that I have been talking about for the last 11 minutes about keeping your emotions in check, keeping long term, having humility, know your bias, et cetera.

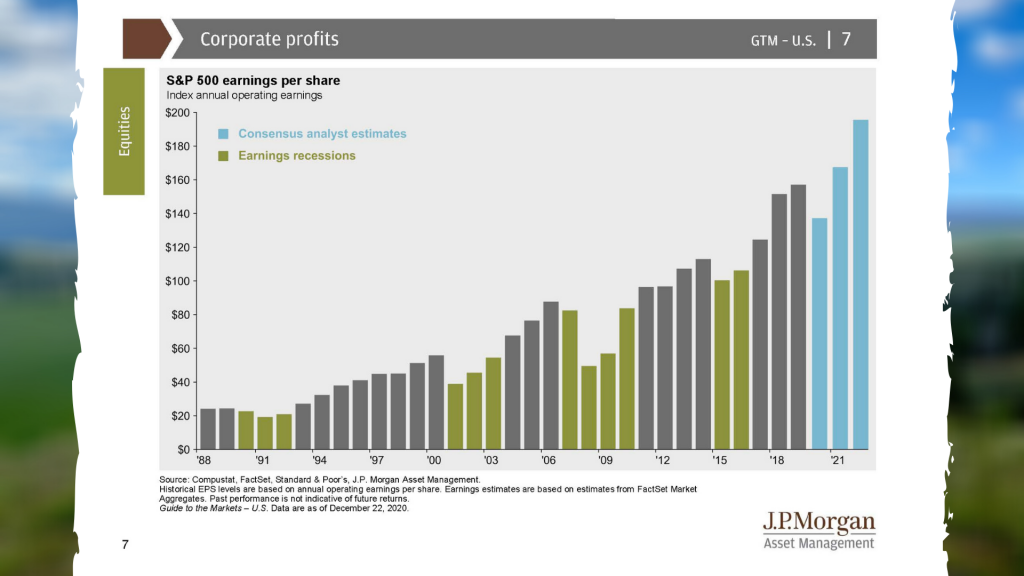

The next thing I put up on the screen is corporate profits, up on the right-hand side, all those blue ones. That’s 2020, 2021, 2022. They’re all positive. I think that’s a good thing.

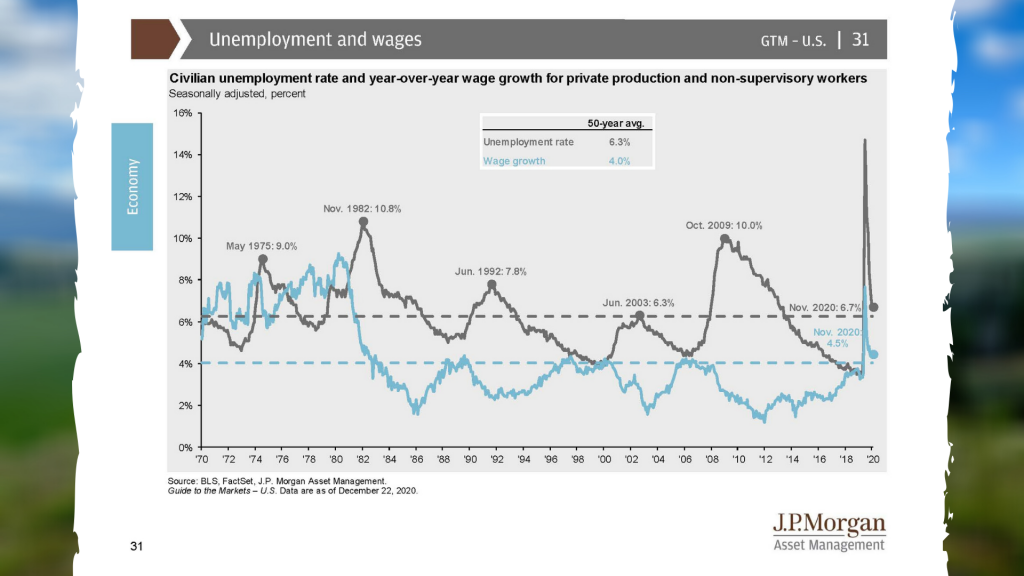

The next thing is unemployment. You’re going to see that we are now back after that huge spike in the second quarter of this year. We’re back to the 50 year average for unemployment. Now is it where it was a year ago? No, it’s not. Is it an absolute disaster? No, it’s not. Could it be in the next year or two as various stimulus plans go away? Yes, it could. It doesn’t mean that we don’t go forward with our particular investment strategy.

The last thing I want to point out on the screen and I alluded to it earlier in the video which is this chart right there. Time diversification of volatility of returns. There’s a bunch of different graphs there. It’s three bars together, that’s one year. The next grouping is five years, ten and 20. What that means is the first of those three bars is 100 percent stock market index. The next middle one is 100 percent unmanaged bond index and the next is a blend, 50-50 of the two. When you look at the second setting of the five year rolling there going back 70 years to 1950, we never had a time horizon when a 50-50 stock and bonds has lost money over five years. Could it in the future? Absolutely. Nobody knows the future. But you know what? I feel good about that. I feel that of all the choices available to me, perhaps that’s one that’s worth exploring very deeply.

Mike Brady, Generosity Wealth Management. A little bit longer video than normal but I had a great time doing it and hopefully you had a good time listening to it. I’m always here to answer anything. Thank you for being my friend, my client and you have a wonderful day. Bye-bye now.

“Every word matters. Don’t make the simple complicated, make the complicated as simple as it can be. You’re not finished when you can’t think of anything more to add to your document; you’re finished when you can’t think of anything more that you can remove from it.” – Ruth Bader Ginsburg

Don’t miss the forest for the trees. While some say timing is everything, with investing, it’s long-term goals to have in mind. The length of the long-term may vary, however the focus is the same- keep your eyes forward and don’t let it stray towards little ups and downs along the way. It’s often three steps forward and one step backwards, so don’t make long-term decision based on short-term feelings.

Listen as I review the 3rd quarter.

Transcript

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive full-service financial services firm headquartered in Boulder Colorado. And this is my last video that I’m doing from my cabin up in Dubois Wyoming. Quick little jaunt down to Boulder but I’ve pretty much been here since mid-May. It has been wonderful. I’ve had the opportunity to take some time to reflect. I think I told you that at the beginning of the summer that I believe in deep work meaning deep focus and I’ve made some huge changes this year kind of behind the scenes hopefully you’ll see. All good, of course, things that I’ve been thinking about. Also looked at some managers and got rid of a couple of managers and added a couple of managers. This has for me personally been one of the best summers of my life up here continuing to run the business. Many of you I’ve had meetings with via Zoom or on the phone. I’ve continued to add new clients. I’ve had some of the best projects and most fun projects in a long time and it was nice to have less hustle and bustle because I’m 30 minutes outside of a 900 person town and so I might go into town once, maybe twice a week but other than that I’m in this beautiful cabin with five acres right next to two million acres of forest land and that affords me the opportunity to really focus and to concentrate and work on kind of big picture things, which I think is very helpful to me and hopefully helpful to you as well.

So, I’m recording this on Friday in the evening after the market has closed on September 25th. You’re going to get this hopefully, if everything works out okay, right at the end of the quarter September 30th, October 1st give or take. And so, I’m not exactly sure what the numbers are but I do know that I’m going to put a picture up on the screen, this is the unmanaged stock market index the Dow Jones, you’re going to see that January getting into February it was up and then February and March were absolutely horrible; that’s when the impact of COVID started to be felt. At that time if you recall and go back to the videos that I made I believe that it was oversold and I’m like wow this is a huge reaction we’ve got to see how things play out. And then what we saw is April, May, June, July, August, five months of a very quick recovery. February through March was one of the quickest and deepest declines ever in kind of recent history. Of course, the recovery has also been one of the quickest and sharpest recoveries. The month of September wasn’t good for the unmanaged indexes; it’s that simple. But you know what? Every month isn’t going to be positive and that’s the way it works. You take three steps forward two steps back at points and if you only focus on the steps back then you don’t have the steps forward.

There are people that I talk to you every once in a while who are so focused on buying at the right time that they actually never do anything they never really invest because they’re so focused on well I might buy in or invest at the wrong time and then it will go down and that’s a very short-term thinking. If you’ve been paying close attention there are certain themes that I repeat over and over again in my videos and one of them, of course, is you don’t make long-term decisions based on short-term feelings or short-term information. In my experience has been if you’re so focused on what’s happening in the short-term you miss the big picture, you know, he trees in the forest if you’re so worried about the various trees you’re going to completely miss the entire forest and then it’s too late. I don’t know what else to say.

I believe that our emotions are very important to keep in check. You’ve heard me over the last year or so say that if you’re watching the news, it’s my belief, particularly if you’re watching the news it’s not there to inform you, it’s to incite your emotions. And so, I say that because over the next one to two months in particular in a political year your emotions might be even more vulnerable than normal. And so, keep that in mind and protect yourself. It’s one thing to have the emotion, it’s another to act upon it so it’s better to not have it but if you’re going to have it at least don’t act on it and so that’s one of my big pieces of advice.

I had this kind of ah-ha moment here at the cabin. We built a deck, we did a foundation for a shed, we do various things and it’s kind of interesting that I have anxiety about those projects. Are they going to get done right? Are they going to be done on time, et cetera.? And mainly my participation in it. I mean maybe there’s a good reason why I’m not a doctor because sometimes I’m working on a project and something happens and I’m not quite sure how to get myself out of it. That’s why I say something about a doctor maybe the patient is open and they started bleeding I’m not sure I would stay calm and know what to do. But then I also look at what I do for a living. I basically invest and watch over people’s entire life savings, their retirement, their kids and their grandkids and I don’t bat an eye. I mean right now I’m actually working on some really interesting situations for some existing clients and brand new clients that are really kind of complicated and quite large amount of money but I don’t bat an eye. I mean it’s completely fun and wow this is a great puzzle that I get to solve. I’m quite grateful. And unlike when I’m out working it’s like wow I’m not sure how to get out of this. So, a lot of it I think it has to do with experience and what you’re comfortable with. For me I’ve done what I’m doing so many times that I have a certain intuition.

I’m reading a book right now called Thinking, Fast and Slow or thinking slow and fast I can’t quite remember, but they said something that I thought was really good. They’re all talking about intuition and they say that intuition is really just recognition that you are recognizing something from before, a pattern or whatever so that really boils down to experience. Intuition is really just recognition even if you don’t know it. And so, I recognize that in myself I’ve done it so many times I have an intuition about what the answer might be and of course I’ve got to check that because sometimes you have biases as well. I’m a big believer in knowing what your biases are and being mindful of them, but it’s also important to know that experience means a lot.

So, we’ve just come through a deep downturn earlier in the year, we have just experienced a huge recovery and I think everybody was surprised by how quickly it recovered. That is not normal. Let’s remember how we felt this year. Let’s remember the decisions we made so that we can remember it the next time it happens again. Remember, the market sometimes goes down so let’s not freak out when it does because we know it’s going to. Once again, it’s good for us to remember this so that pretty soon we too start to recognize the pattern of wow it goes down, it goes up but the reason why I’m invested is because it’s for the long-term.

One more thing I want to say before I say goodbye is I’m also a huge believer in knowing what your timeframe is. Absolutely essential. One week is completely different timeframe than ten years. Two or three weeks ago the NASDAQ, which is an unmanaged stock market index, was really going down. And so, my friend said I’m totally getting killed, I’m just losing so much money. And I couldn’t help but wonder really in one day or two days when it’s just come up tens and tens percentage points in the last for five months you’re going to decide your happiness for the day based on one day or even one week? It’s good to know and keep in mind the long-term picture. Absolutely essential.

Mike Brady, Generosity Wealth Management 303-747-6455. Quarter end statements will be going out very soon. I think you’ll be very pleased. We have one more quarter in the year and as always I always am very optimistic and really looking forward to hopefully a good end to the year. If not it’s okay we don’t make decisions based on one quarter or even one year. Have a great, great day, great week. Bye-bye.