“One moment of patience may ward off great disaster. One moment of impatience may ruin a whole life.” – Chinese Proverb

If you flip a coin 1,000 times–mathematically, 500 times it’ll be head, and 500 times it’ll be tails. However, if you look at the distribution of those heads and those tails, sometimes you’ll have 10 tails in a row, or you might even have 20 heads in a row. It doesn’t mean that the 21st or the 22nd will be either heads or tails. It’s just that they get clumped together. The reason we look at this analogy now is that’s what we’re seeing in the financial market. It’s very painful and no one is happy.

Of course heads and tails is completely random, the financial markets are not, their odds are even better than 50/50! When you look back over 90 years, three out of four years, not 50-50 but three out of four years are positive. In year’s like we’re having in 2022, this can be hard to remember because it’s been a pretty sharp decline, not only on stocks but also in bonds. And there’s a lot of reasons for that. We’re going to talk about it here today.

Transcript

Hi there. Mike Brady with Generosity Wealth Management. Today I want to start off with an analogy. If you flip a coin 1,000 times–mathematically, 500 times it’ll be head, and 500 times it’ll be tails. However, if you look at the distribution of those heads and those tails, sometimes you’ll have 10 tails in a row, or you might even have 20 heads in a row. It doesn’t mean that the 21st or the 22nd will be either heads or tails. It’s just that they get clumped together. The reason why I bring that up is that’s how it feels right now. Every day, every week, every month so far this year has felt like it’s been down. Very painful. I just hate it. Nobody likes it.

One thing that’s a little different from my analogy is, of course, a head or tails is completely random. That is the pure luck of the draw. With investment, and especially when you look back over 90 years – I’m going to put a chart up here in a few minutes that will show since 1980, which is now over 40 years – three out of four years, not 50-50 but three out of four years are positive. But, I’ve got to tell you that this year it’s hard to remember that because it’s been a pretty sharp decline so far this year, not only on stocks but also in bonds. And there’s a lot of reasons for that. We’re going to talk about it here today.

The very first thing I want to show is a long-term chart, and I’ve just put a circle around where we are right now.

Irritating. Absolutely painful and one of the reasons why I am always talking to people about their duration. You can sit back and watch these videos that I’ve been doing for 12-13 years, and in almost every single one I talk about, well, if you need money in the next couple of years, you shouldn’t even have it invested. That’s because periodically, there are these times where the market goes down, the unmanaged stock market indexes, and it takes a while for it to recover. And who knows how long this particular one is going to recover. But I’m going to show you that a balanced portfolio, at least historically, has come back 100 percent of the time. If you’re an individual stock, no, that’s not the case. Things go bankrupt, which is the reason why you stay diversified. Staying diversified, what’s your duration? Those types of things are real nice and cute and almost cliches until something like what has happened so far in 2022 actually happens. And then you remember why it is a core fundamental foundation to investing.

Up on the screen once again is where we are so far this year.

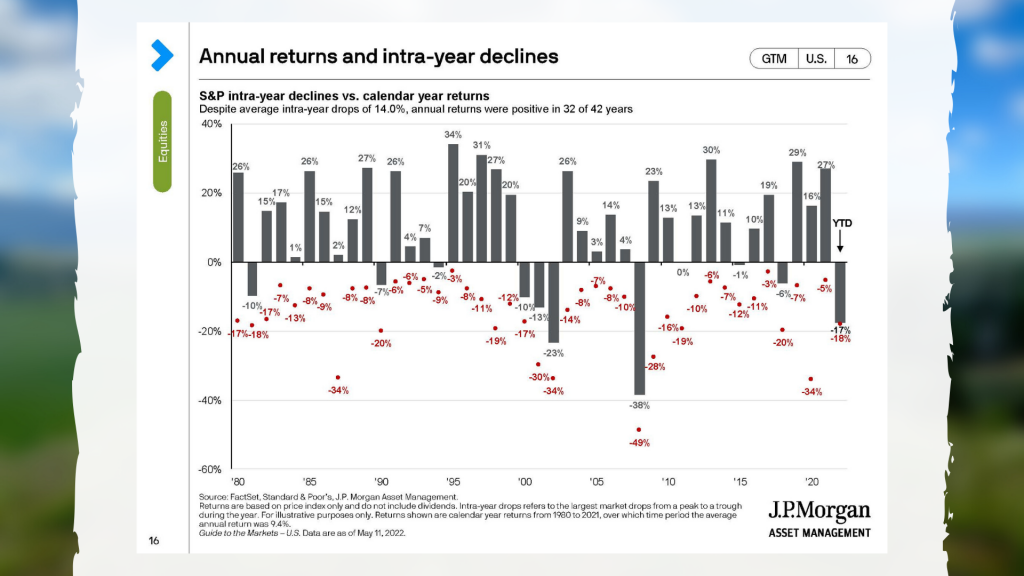

As you look at this next chart, the numbers on the red are the intra-year declines for an unmanaged stock market indexes, the S&P 500. That means that during the year, there’s a decline of that amount. A lot of times, it doesn’t happen at the beginning of the year. Maybe the first half of the year is really good, and then it gives up some of the money. The top number, the black number at the top is the way the year ended, the rate of return. So, just because there’s an intra-year decline does not necessarily mean that the year ends negative. It is too early so far this year; it’s now the middle of May, who knows how the year is going to end. But just because it has started off not good at all does not mean that the year will end negative.

This screen right here, I’ve circled that on the right-hand side.

You’re going to see that depending on where it’s invested, the unmanaged stock market indexes, this is kind of a compilation of them, you’re talking between 10 percent and almost 30 percent negative for the year. It’s really been a broad-based decline so far this year, which is painful for everyone. At least a couple of years ago, when the COVID decline happened, we’d have some up days. It feels like a long time since we’ve had an up day which is absolutely irritating. Sometimes these sequences of returns are not in our favor, and that’s what’s happening right now.

The next page and I’ve now circled it, are the returns for bonds.

Most of the time, stocks and bonds are decoupled, meaning that when stocks go up, bonds go down, and the other way around, bonds go up and stocks maybe go down. Right now, because of the interest rate increases, the bonds have also declined, and they have priced in future expected rate increases. When interest rates go up, bonds go down. They’ve priced it in. So, from my humble opinion, I believe that this is a relatively short correction, an overcorrection in the bond market, that will be corrected as the months play out. At this point, the hit has happened with the bonds. I don’t expect it to be much greater in the future. But, stocks are down, and bonds are down, which really is the core of a portfolio – stocks, bonds, and cash. Cash is paying nothing; bonds are negative this year, and stocks are negative as well, the unmanaged stock market indexes and the unmanaged bond indexes. So, it’s not really been a rosy picture. It’s been very painful, and this is the reason why you have long-term investments. If you’re looking at things on a daily, weekly, monthly, or even quarterly basis, sometimes you’re going to be very disappointed. And that’s when the fortitude, your emotional control, is so important. The best advice I ever give as a financial advisor is to stay in control of your emotions. You don’t take short-term trends and extrapolate it out into a long-term decision.

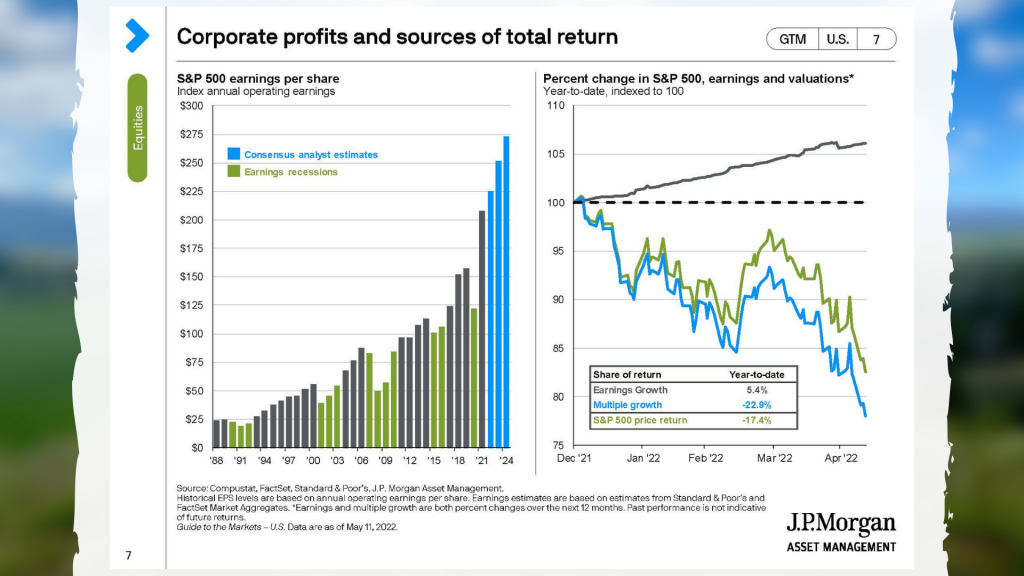

This next graph that I have on there are corporate profits.

You’re going to see corporate profits are good. When we’re trying to evaluate the future of the market, one of the things that’s absolutely essential is the money volatility which is high, and also what is the cash reserves and the profitability of the things that we might be investing in. That is good. That is a positive sign. That’s something that I’m very happy about.

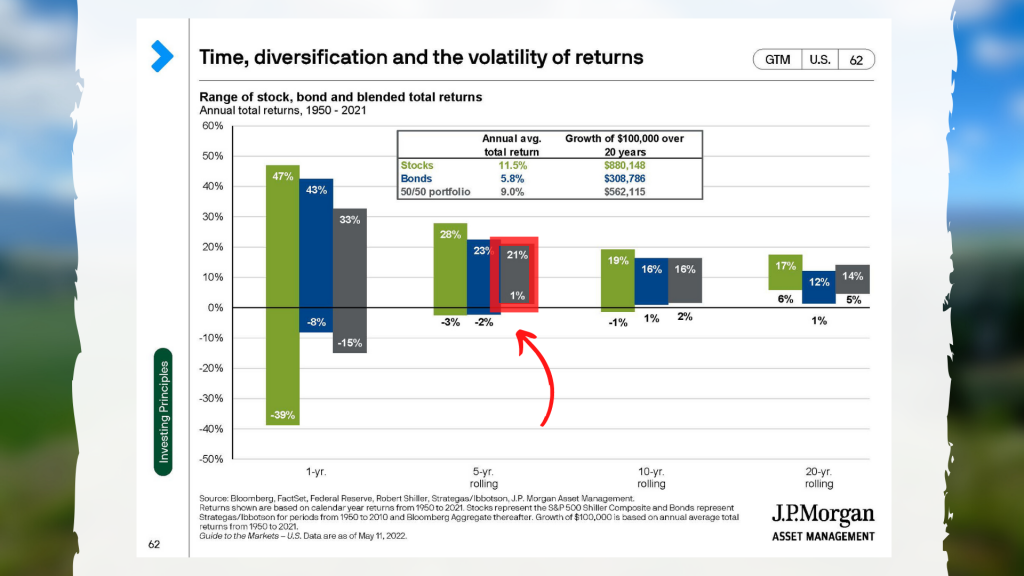

One thing that we have to remember, this next sheet here, I said earlier that if you have a diversified portfolio, I now have circled five years out, at 50 percent unmanaged stock market index and 50 percent unmanaged stock and bond index.

It’s returned, at least going back since this is all the way to 1950, so that’s 50, 60, 70, 72 years you’ve had a 100 percent recovery rate within five years. Now, let’s hope that it doesn’t take five years for us to recover our particular portfolios. It’s gone down. The absolute worst was that. Most recently, we had declines two years ago, right around Christmastime. Well, before that, it was the COVID and that recovered within the year, within nine months. Prior to that, in 2018 there was a huge decline at Christmas and it still ended up about breakeven, just a little bit negative for the unmanaged stock market indexes. But it recovered very quickly within months. When we look back at 2011 with the downgrade of the U.S. government, it recovered very quickly. In 2008 it still recovered very quickly. The worst financial crisis that we have seen in most of our lifetime was still a two to three-year recovery if you had a diversified portfolio. That’s one of the reasons why I’m always talking about you’ve got to know what your duration is. It doesn’t mean you’ve got to like it when you’re underwater. It does mean that you’ve got to be patient. Warren Buffet has a great quote that says, “Corrections like this transfer money from the impatient to the patient,” which is the reason why I always say you’ve got to be patient.

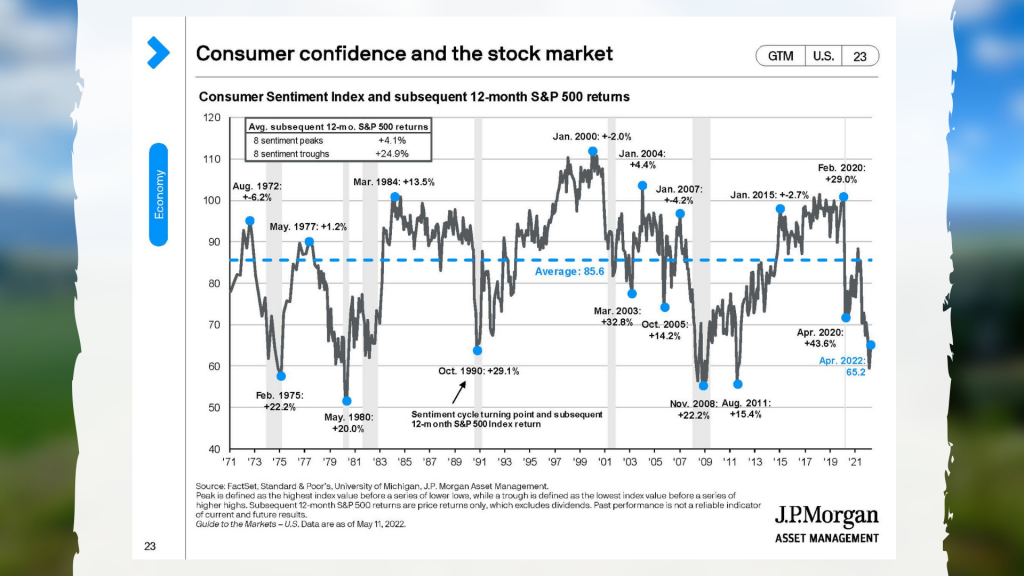

Right around this time, this next chart is consumer confidence.

When the market is down, a lagging indicator is confidence. Not a leading, it’s a lagging. Oh my gosh, consumer confidence is at an all-time high. That usually happens after the movement has already happened. In this case, it’s the opposite. Consumer confidence is at a low. That’s because after the fact – and I’m a contrarian – what everybody knows isn’t worth knowing. When everything is going up, then you’ve got to wonder, wait a second, when is it going to go down. When so much has gone down, this is when a contrarian like me says, “Gosh, now is when I might want to put more money in.” If I believe that it’s going to recover and it’s going to be higher in the years going forward from where it is now, don’t I want more invested in the unmanaged stock market indexes. Of course, that just makes sense. But I will tell you that our emotions have this tendency to say well, it’s going up so it’s going to continue to go up so, therefore, you’re buying at the top, and you sell at the bottom. That’s what real investors who do not have professional investment advice many of them do. Not all, but many.

The last chart I want to talk about today is inflation.

It is unbelievable how inflation has shot up in the last year. When we had COVID and the whole world pretty much closed down, we dumped lots of money into the economy and I think that was a wise thing. Otherwise, we never would have been able to restart the economy at any point. This is my opinion, and the opinion of many, many economists is that was a smart thing, but sometimes you can just go too far. A year ago, way too much money was poured in, fiscal bills that were unwise that have thrown so much liquidity in that it increased inflation, and that’s what we’re seeing right now. Yes, there is a strong argument to be made that it’s also through some of the demand that we have when we don’t have the supply in order to meet that demand. I get it. And that doesn’t help that we’ve got China is in lockdown with all of their COVID issues that they’ve got going on. Absolutely. What the value is of these two variables to get to where we are right now, it’s where we are right now. It’s that simple.

A year ago, I have to tell you that especially as these massive spending bills were being passed that there were many economists who were saying that this was going to lead to a high increase in inflation. I even had a couple of clients send me some articles talking about it, and I said, “No, I don’t believe that. Let’s not extrapolate out one or two months’ worth of data into an entire year.” Well, that whole year has now gone by, and yeah, we’ve gotten higher inflation than most of the economists a year go would have imagined including me. So, it’s remarkable that some of the signs were there. It could have gone the other way. I mean, there’s an old joke that economists predicted nine out of the last three recessions. And we’re always thinking, yeah, oh my god, this is horrible. Well, in this case, it was a situation where it has actually turned out worse than most economists have even imagined. And thank goodness there were not even more fiscal bills that were passed that were proposed.

How exactly the supply issue is going to continue to impact things, we’ll just have to watch it very closely. One thing that we have to keep in mind is that there’s always a reason to be pessimistic, and at a certain point you get that out of the system, and then it’s a buying opportunity again. If you’re already invested, then great, you stay invested. If you’re not invested sometimes, it’s a good place to be which is to be in there for any kind of recovery that might happen.

We don’t know when it’s going to happen or how long it will take in order to break even and for us to be in that positive again because frankly, so far this year we’ve give up much of what was gained in all of 2021. We’ve probably taken a 6, 12, 18 months step back to where we were. But what isn’t helpful is to catastrophize. That means if its gone down, you imagine, oh my god, I just don’t want to lose all my money. Just because you’ve made some money, it doesn’t mean you’ll always make money. And just because you’ve lost some money in some timeframe, it doesn’t mean you’ll lose all your money or continue to lose money. It’s not linear. It doesn’t move in a straight line, and so we have to remember that it truly is three steps forward, one step back, and sometimes it’s two steps back. When we look at the past 12 months, it has been three steps back. Three steps forward, three steps back which is absolutely irritating. So, it doesn’t mean that it’s flawed in any way. It’s how we want to view it and, of course, our emotions allowing us to make the decisions that we need to make which is to stay with the plan that we have.

Mike Brady, Generosity Wealth Management. You have a great day. See you. Bye-bye.

“The Stock Market is a Device for Transferring Money from the Impatient to the Patient.” – Warren Buffet

There are always reasons to be pessimistic. There are always reasons to be concerned. That’s why we keep our investments, keep our strategies sound and we stick with it.

While we’re seeing inflation soar, gas prices rise, and a war rage on between the Ukraine and Russia, we must remain focused through the uncertainty. The reason why we have investments is because we believe that in the future it will be higher. We don’t know exactly when that will be, but a good guess is that now is the low and we’ll be happy in the future.

Let’s take a look at what we’re seeing in the current state of affairs and what it truly means for our investments.

Transcript

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered here in Boulder, Colorado.

With today’s technology you never know if this is a backdrop or if it’s reality. And I’m just telling you it’s real. I’m out here in the gardens of my building. A beautiful spring day and I want to share it with you and I’m hoping that you’re enjoying the spring weather we’ve been having as well.

For the past year gas prices have steadily increased and they might go up more—I’m not really sure with the energy through Russia and Ukraine and some of the supply problems we’ve had there. We’ve got inflation. Twelve months ago we started talking about it. It has steadily increased. Now it is at the high in the last 30 to 40 years. We’ve got the worst start to the unmanaged stock market index, the S&P 500, in almost 50 years. There’s lots of reasons to be pessimistic if you allow yourself to be pessimistic. And, we’ve got continued from the pandemic supply chain issues. What does this all mean?

One thing that I like to think about, and I believe that you should as well, is what’s the long term impact of some of the changes that happen. We’ve had globalization now for many decades and I continue to think that’s a good thing. It’s not perfect. It’s not a panacea. I think that’s one of the things that we’re finding out is just because you do business with a country like Russia, it doesn’t mean that they won’t invade you or they might invade another country, one of your allies, that puts you at odds. We are interconnected which is both good and bad. So, there’s no absolutes in this. There’s a spectrum that is continually being negotiated between countries and the world and the economy. Things are complex.

The older I get, that is one of the messages and one of the things that I’ve learned is that it’s not if A, than B. It’s A plus B plus C plus all these things and then I might have an output of X, Y or Z. There are many things that contribute to an ultimate equation, to the solution, to the output. And we have to always remember that. Things are not simple. Things can be complex, and so we take that humility of not knowing exactly what the future holds into the decisions that we make.

I remember back in the 1990s. This is before I owned my house and I was in my 20s. Listening to this older couple – of course this old couple were in their 40s – younger than I am right now. And they said, “Oh no, we rent here in Boulder because it’s so expensive. We think that it’s real high in the market. We’d be crazy to buy a house here in Boulder.” Really? What do any of you who have property think of that decision. Not very long sighted. Not very forward thinking. I remember when I bought my house that I’ve lived in for the last 22 ½ years. I bought it in 2000 which was pretty much the high of the tech bubble. I remember people saying, “Oh my god, housing is at a bubble and you’re kind of a fool for having bought it.” Since then it’s doubled, it’s tripled depending on what source you want to go to, and I’ve lived in it the entire time. I love my house. I’m probably going to die in in hopefully many decades from now and it’s served my purposes.

Just yesterday I was talking with someone who’s considering real estate again and they said, “Well, should I really buy because it’s really at a high.” Well, it is at a high from where it was one year ago, five years ago, ten years ago. When we look back 10 and 20 years from now are we going to say that it was at a high now? Most people would say no. I’ll bet if you really think to yourself wow, if I have a 10 or 20 or 30 year house that I’m going to live in or rent out, it’s probably now might be the low.

Let’s take that into investments. It’s the same concept. When you have a diversified portfolio, and I’m going to put up on the screen some bar graphs that you’ve seen before, that a diversified portfolio of 50 percent of diversified unmanaged stock market index, and 50 percent of a bond index diversified, there’s actually never been a five year time horizon going back to 1950. One hundred percent of the time it has at least broken even or made money over a five year time horizon. The next five years could absolutely be different. Frankly, it’s still something that I believe is important for me to think that I’m making a bet. That’s why I have investments that five years from now, now might be the low in the markets.

I said two years ago when the markets went down significantly that I thought it was an oversold position and we might, for the rest of this year, the markets as an unmanaged index might still be down. It might happen, absolutely. It could even be in the next two years, but that’s why we always have to have a time horizon of, you know what, it might be high right now, it might feel that way. It’s definitely lower than where it was four months ago. That’s the reality. But it’s higher than where it was a year ago, five years ago, ten years ago, 20, 30. Going forward nine months from now it could be lower. Two years from now it could be lower. It could be lower – there’s no guarantees – anytime in the future.

However, the reason why we have investments is because we believe that in the future it will be higher. We don’t know exactly when that will be, but I would guess that now is the low and we’ll be happy in the future. Even though the ride, the fun of seeing it go up every single month isn’t there and it stinks along the way, that’s the reason why you don’t look at it every day, every week or even every month. That’s why you’ve got to string these things together.

There are reasons to be pessimistic. There are reasons that I’m concerned. I’m not going to lie. If the Fed doesn’t get this inflation, these numbers, under control that will be bad for the economy. That will not be good. You know what? We have recessions periodically. That’s why we keep our investments, keep our strategies sound and we stick with it. That’s what we do here as well.

Mike Brady, Generosity Wealth Management. Give me a call at any time, 303-747-6455. You have a wonderful day, week, month and let’s make it a great year. Bye-bye.

“The best way to find yourself is to lose yourself in the service of others” — Mahatma Gandhi

As the quarter is now over, it’s a wonderful time to reassess our mindset–do we have an investor mindset or a trader mindset?

An investor understands the long term and is not deterred by short-term events. They do not look for reasons to be pessimistic or instantly act upon a negative reaction.

A trader mindset does that. Short-term events are important, even if you’re invested for the long-term.

This was a tough quarter, and negative. Negative quarters are part of long-term investing, and what investors will experience periodically.

Let’s take a look at what we’ve seen so far in 2022 and compare it to years previous.

Transcript

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered right here in Boulder, Colorado.

I want to take us back to some recent history, just the first quarter of 2020. Covid hit, markets down 20%, 30%, 40% in the unmanaged stock market indexes and everything just looked horrible. At that time I said, “Hey, I think this is an overreaction and an oversold position.” But never in my wildest dreams did I imagine that by the end of 2020, not only had the unmanaged stock market indexes and the unmanaged bond indexes had recovered what they had lost, but they then went into strong positive territory.

So, 2021 which was last year, nice positive territory again. The first quarter of 2022 is negative for the unmanaged stock market and bond indexes. That’s part of the game.

One of the recurring themes that I have in my videos, whether they’re within the quarter or at the end of the quarter like this one is, is that we need to have an investor mindset, not a trader mindset. The difference is an investor understand the long term and is not deterred by short-term events. Does not look for reasons to be pessimistic. Does not say to him or herself, “Okay, it was so obvious,” or, “Oh my gosh, I should have been able to avoid that.” No, that’s a trader mindset. If a quarter of decline is not something that is palatable, then you have either a trader’s mindset or you really should not be in the stock or bond markets at all. It’s just that simple because it will always happen.

If you are an investor anywhere in the U.S. or the world, you have a portfolio that is probably down so far this year. But what history has shown even if it is in correction territory, which is what we have been in, correction territory is negative 10%. I’m recording this on Thursday, March 24, so I don’t know exactly how the quarter has ended. But if it’s around 10% that’s correction. A bear market is 20% negative or greater. If it’s negative 10%, what history has shown is that 75% of the time it’s positive again a year to a year-and-a-half out. And sometimes it’s longer.

When we look at major, major impacts like 2008 and a blended portfolio of 60/40, it took about three years to recover. However, that stands out in memory because it’s so unique when events like 2008 hit. So, 75% of the time going back decades it has recovered within 12 to 18 months. And that’s part of the process of being an investor. Having the temperament to remember that no, we should not have short-term vision. We should not have a short attention span. We need to think about what does this mean for the long term because you don’t invest for the short term, you invest for the long term. You trade for the short term and that’s not what we’re doing. We’re investing for the long term.

As we look to see what this actually means – I’m kind of curious but I’m watching it very closely. What does globalization look like with China and Russia? What does globalization look like with the supply chain breakdown over the last couple of years? Is there more onshore versus offshore? Are we going to bring a lot of that manufacturing, a lot of the being self-sufficient from an energy point of view to our country? Is there going to be more of that with many countries throughout the world than there is now.

We’ve become interdependent which is a good thing in my opinion. It’s better than not being interdependent with others, but this is a shake to the system. The geopolitical events that are happening is reshaping how Europe sees itself and it’s reshaping how the world sees its supply chains and its dependency. Does doing business with someone mean that they won’t invade you? No. The answer is no. We’ve just seen that. Does it mean that you can be a pariah and still invade your neighbors even though you’re part of the global economy? The answer is yes. So, what are the longstanding impacts of this is what I’m always looking at.

When we look at things from a portfolio point of view, from an investment point of view, there is still huge cash reserves by the main companies in the S&P 500 which is an unmanaged stock market index, the Dow, et cetera. The Apples of the world, the big companies have huge cash reserves and this is a good thing. They have seen and weather bad things over the last 10 to 15 years, and the alternatives of cash – just putting your money into a CD – is very unattractive.

So, I continue to be a long-term investor and recommend that for clients. Volatility is something that with experience you become well, experienced. That’s why we call it experience. And so that’s something that you have to live with.

That’s it. Things are going to be down for this first quarter. That’s the way the temperament of an investor has to acknowledge. I love what Warren Buffett says. “In times like this, it transfers money from the impatient to the patient.” Give or take a few billion dollars, he and I we hang out in the same crowds – I kind of wish.

Mike Brady, Generosity Wealth Management, 303-747-6455. Give me a call. Let’s hope the second quarter and third quarter and as things move forward when are we going to break even again? We don’t know, but history has shown that it does break even. Not a long time, but usually in a short time. Thank you. Have a great day.

“Learn from the ocean; not fearing turbulence, it uses the wind against it to rise instead.” – Matshona Dhliwayo

We invest because we believe the long-term is going to be better than the present. During turbulent times like we’re seeing right now with Russia invading Ukraine, in the midst of a mid-term year we need to remember this strategy.

Short-term events shouldn’t dictate our long-term financial strategy. In this video update, Generosity Wealth Management founder, Mike Brady, reiterates the strategy he recommends to his clients: Time Horizon Long-Term Vision.

Humility, like gratitude, is not so much a technique as it is a way of life.” – Ed Latimore.

New Year, same tried and true financial plan. While your goals may change, having a steady and reliable plan is crucial all year round.

In our latest video, Generosity Wealth founder, Mike Brady, briefly reviews 2021, and talks about the perils of predictions. Instead of a prediction, he offers you his 3 best to-dos and not to-dos for financial planning in 2022.

On the top of the to-dos:

Have some humility

Be disciplined

Concentrate on what you can control

Watch the complete video to see the additional three not-to-dos that serve as a warning of what to avoid.

2021 saw a positive stock market index and even with rising interest rates negatively impacting bonds, the year still had low volatility. While you may be tempted to hang on the words of pundits prognosticating the year ahead, remember that 2022 is an unknown. However, with these practical tips, you can weather any storm.

Transcript

Mike Brady with Generosity Wealth Management, a comprehensive, full-service financial services firm headquartered right here in Boulder, Colorado.

2021 is now behind us and 2022 is here already. Let’s call 2021 what it was which is a great year, low volatile for the stock market indexes. Pretty much anyone that you look at across the board it was positive and many of them in the double digits, the teens all the way into the 20s. We’re talking value, growth, international. You name it, it was a good, relatively low volatile year. One thing that was not good in 2021 was with rising interest rates, bonds. One of the reasons why you have bonds in a portfolio is to dampen the volatility, so nobody ever complains about making money quickly and having high highs, but nobody likes losing money on the downside or having low lows. So, when you combine these two things together – bonds and stocks – you combine them together and instead of having volatility like this, the volatility is a little bit, not as much on the high side unfortunately, but also you don’t have it on the low. So, over multiple years it is, in my opinion, a better way to go and you can live with it without the emotionality that comes with, “I’m a genius, it’s so high” to the “I’m a loser, it’s so low.” It allows you to say with your plan which is really what I think it’s all about.

You’re going to hear a lot of pundits whether it’s on the radio, the TV, maybe even in print media, talk about what they think 2022 is going to bring. Oh, the market is going to be up this or it’s going to be down that. I avoid it. I’ve been doing this for 30 years and those guys are always wrong, but yet everybody always asks about the next year and they always give out their opinion, and nobody knows what the future is. I think that there’s lots of reasons to be concerned about inflation and the economy and things of that nature, but what we’re not going to do, at least not what I’m going to do, is change a long-term plan that I have for clients based on short-term events which I’m going to talk about here in just a little bit.

I want to share with you three pearls of wisdom and then three things not to do. Since this is my year-end video, or beginning of the year video, whichever you want to look at it, these are core values to what I think so I would like to impart them with you.

Number one to do – and I’m going to put them up there on the screen – is have some humility. The world is complex. Every time that I think I know absolutely everything, you can be sure I probably don’t. The duality of life is true. You can be happy and sad at the same time. You can have things happen in the market that don’t fit real nicely into a headline. The markets can be up one week and down the next week and neither of them made sense. Why would there be a flip like that? Up, down, up down. No, people’s pessimism and optimism isn’t changing every day, but if you’re a newspaper reporter you’ve got to figure out how to make it to a nice, cute little headline. Avoid simple answers to complex issues, and in the finance world things are complex.

Number two, be disciplined. Think about how you were successful up to now in your life. Was it being overly emotional? Was it allowing your emotions to dictate your logic? Probably not. It was because you had some discipline. You were methodical, you hopefully had control of your emotions. I’m going to encourage people to always do that and to continue what made you successful up until now.

Number three is concentrate on what you can control. There are lots of things in this world that we can’t control, but things that we can control is how much we save, how much we spend, when we decide to retire. Some of the factors that could derail us from our financial plan whether that is mitigating the financial loss that might be from our inability to work or a loss of our spouse. There’s lots of things that we can focus on to help ensure that we reach our financial goals. But let’s also not spend so much time and most of our effort on the things that we can’t control.

Here are three things that I have found over the last 30 years that are not helpful. The first one is short-term data is dictating your long-term actions. That makes no sense. If you’ve got a long-term plan, don’t let short-term data dictate that. That’s not helpful whatsoever. Just because the last couple of weeks or the last couple of months have been up, it doesn’t mean the next couple are going to be up. Or just because the last couple of weeks or the last couple of months have been negative and everything you read on the news or watch on the TV is negative, that doesn’t mean the next two or three months or the next year is going to be negative. It just doesn’t work that way. So, don’t do that.

The next thing is let your emotions be manipulated by the media. Most emotions are through the TV media, maybe some through radio and a little bit less on the print. Don’t do that. If it bleeds, it leads and that is the same thing with finances. I’ve already talked about being disciplined and controlling your emotions and things of that nature. This is a part of it. This is one of the variables to you being successful is don’t let yourself be manipulated by entertainment people who really just want you to keep tuning in. Don’t be that person.

The third thing is don’t have a feeling. You know what, I just have a feeling the market is going to turn. I know more than the market is really what you’re saying. Don’t be that person. I have yet to see that work out. Stay invested, have your long-term plan and don’t mess with it. Find something that works for you that you can stick with, and then stick with it. Don’t listen to your brother-in-law, don’t listen to the TV guy. Stick with what works for you and not always listen to the other people who are not focused on what your financial success looks like.

That’s it for my pearls of wisdom and also things to avoid. This next year I’m very excited. I’ve got a couple of good charities that I’m giving money to in relation to all the people who are having birthdays this year. Every month this year I’m going to have a lottery where I pull a name out of a hat and I will contribute $250 to the charity of their choice. I’m really excited about that and we have a great birthday package in store for 2022.

That being said, I’m here at all times. I love what I do and I want to do this for another 20 years. I just absolutely love it and it doesn’t even feel like work and as long as I’m physically and mentally capable I’m going to be right here.

Mike Brady, Generosity Wealth Management, 303-747-6455. You have a wonderful day, week, month, year. Bye-bye now.

“Perpetual optimism is a force multiplier.” – Colin Powell

It’s important to keep the big picture in mind when looking at your financial investment portfolio performance. The first 6 months of 2021 were good, the last 3 have been pretty much break even and the final 3 months of the year have yet to be determined. While things are positive in the unmanaged stock market index and bonds and zero in the cash/CDs, when we look at the big picture we see that we need to stay the course and remain confident in our long-term plan.

Every year there is a reason for there to be pessimism, if pessimism is what you’re looking for, conversely the same is true for positivity. The future is unknown, however our attitude and resolve doesn’t have to be.

If you have short-term needs to prepare for, of course it’s beneficial to set aside money now. Connect with Generosity Wealth Management founder, Michael Brady today if you have a situation requiring specific assistance.

Transcript

Hi there. Mike Brady with Generosity Wealth Management, a comprehensive, financial services firm headquartered in Boulder, Colorado.

This is the last day, sadly for me up here at my cabin in Wyoming. This has been a magical summer once again. Many of you I’ve had Zoom meetings with and emails and phone calls, so there’s zero interruption in the business, but it certainly does enrich my life, the ability to spend a lot of time up here doing outdoorsy things. If you get me on the phone I’ll tell you all the things that I did this past summer to improve our place. But I also think that it’s great to get away, to get some perspective, to get outside of your bubble, to look at things in a new way. Some things will be different, some will be the same, but I think that it is important to proactively do that with your own thinking.

So, 2021. We’ve got three quarters down. I’m recording this on September 29, which is Wednesday. You’re probably getting this the first week of October, and by the time you get this you probably have your end-of-the-quarter statement if you’re my client.

What we’re going to see so far this year is that nice run-up for six months, and then the last three months has been about a breakeven. The unmanaged stock market indexes are positive, high single digits or low double digits depending on what index you want to look at. Bonds are positive as well in the low single digits. Cash whether that’s CDs or money market, et cetera, frankly almost zero. I was looking at some CD rates and some money market rates for a client a couple of weeks ago as he had an extremely short-term liquidity need, and it was very, very low – almost zero.

I think that it’s really important for us to keep the big picture in mind. You’ve heard this from me over the years. I’m like a broken record, but I believe that is one of the keys going forward, the duration. One of the things you might ask yourself is, are there any short-term needs that you have over the next year or two that you need to prepare for. Because, if so, then we should set that money aside because that’s a short duration need.

Now, if we go back to 1980, what you’re going to see is 31 out of those 41 years were positive for the unmanaged stock market index, the S&P 500. Three out of four years. When we actually go back – I’ve seen another study going back to 1929, same thing. Three out of four years, and in that case I think it was 73 percent were positive. So, this is a good thing. When you flip a coin, 50-50 is tails and 50-50 is heads. And when you do 1,000 of those flips, you should have 500 heads and 500 tails. Some of the distribution of it as you look at it though, they’ll be runs. They’ll be head, head, head, head, head, head, head or tails, tails, tails, tails, tails, tails. The stock market is very similar in that there will be some distributions where some years will be positive, positive, positive, negative, negative, negative. But as we look back 41 years, three out of four of those years are positive.

I’ve been doing this for 30 years since I graduated college in the early 90s, 1991. I was 22 years old, and I’m now 52 years old. During that time I have to tell you that every year inflation’s about to rear its ugly head. Every year the other political party is going to ruin this country. It flips, of course, depending on who’s in power. Every year there’s a reason for there to be pessimism if pessimism is what you’re looking for.

I hear pretty much every year from some people saying I’ve just got a feeling. I’ve got a feeling that we’re about to have a correction. I want to tell you that corrections are normal. Of course, like a broken clock, you’re right twice a day. Yes, there are always corrections. Double-digit declines are actually the normal within a year with some of the unmanaged stock market indexes. However, my experience has been that we forget the times that we thought there was going to be a correction and there wasn’t. The amount of money that would have been lost through the opportunity gain if you move to cash and then the market continues to go up is kind of an abstract loss. Whereas, just staying invested, keeping it for the long term, you can see in the short term that there’s an actual loss there. Hey, I used to have $100,000, now it’s worth $90,000 or $85,000. But over time that’s the reason why we keep the long-term vision in place is that it comes back, and it has historically. The future is always uncertain.

However, you know what. I think that’s the best for you, for your health, for your portfolio, for your peace of mind is not to try to decide exactly when and in and buys and sells and things of that nature. It is to be diversified because different areas of the market also do different things. Last year, 2020, value section of the market didn’t do so well. This year it’s near the top. And fixed income, same thing. So far this year, high yield has been the winner. Last year it was not. Last year it was TIPS, Treasury Inflation Protected Securities.

Even within the stock market, the bond market, different areas of it go in and out of favor year by year. That’s why we have a little bit of all of it because it’s difficult. Only in hindsight is it perfect. In the future, it’s always unknown and you can kill yourself, you can really cause yourself a lot of discomfort by always trying to guess what it is going forward.

I have no huge changes that I would recommend for my clients, for you if you’re not a client. Stay calm. Corrections are normal. We should always be looking at the duration of what our needs are for our cash, and the longer that we can keep it invested, the happier we will probably be. That was true 30 years ago, and it’s true today.

Mike Brady, Generosity Wealth Management, 303-747-6455. You have a wonderful day. Thanks. Bye-bye.